Gas Engines Market — Strategic Preview for 2026 Decision-Making

As companies plan capital allocation, product roadmaps, and market-entry strategies for 2026, the gas engines sector presents a mix of steady growth, technological pivot points, and regulatory inflection that demands disciplined, data-driven choices. PW Consulting’s upcoming Gas Engines Market study (base year 2025) synthesizes historical performance, near-term dynamics and scenario-based forecasts to give executives the strategic clarity they need — without overwhelming them with raw segment tables in a first pass. This introduction outlines the study’s strategic value and the type of operational intelligence decision-makers can expect when they access the full report.

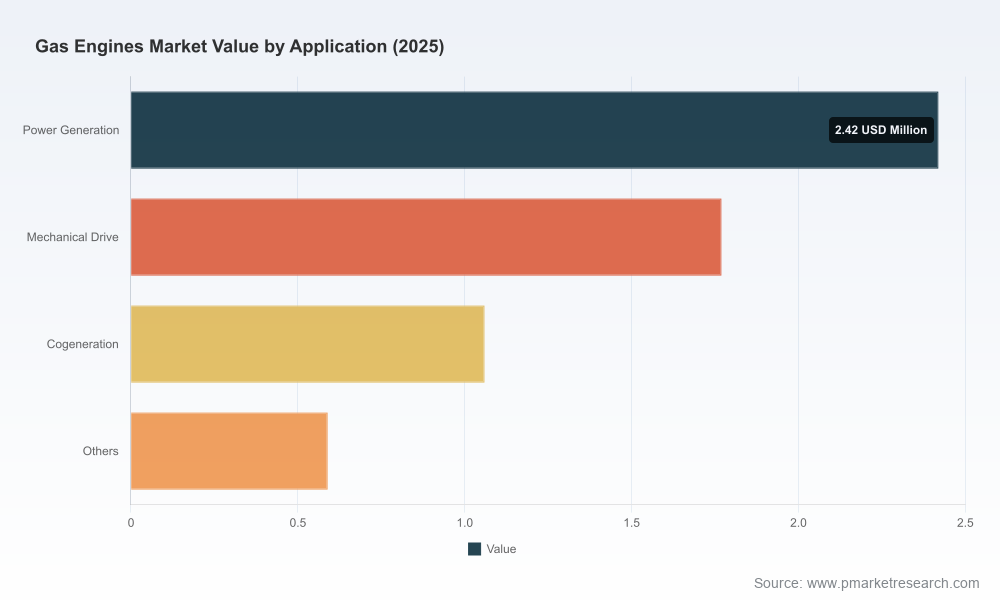

Gas Engines Market

Market trajectory at a glance

Between 2020 and 2025 the global gas engines market demonstrated resilient recovery and expansion. Measured in USD Million, the market moved from the mid-single digits in 2020 through sustained growth to a 2025 base around the mid-to-high single digit mark. Looking forward, our forecast (2026–2032) anticipates continued expansion at a compound annual growth rate (CAGR) of 5.6%, reaching a materially larger market size by the end of the forecast window.

Gas Engines Market

Why these headline dynamics matter for 2026 planning: a 5.6% CAGR implies that strategic investments made now — in product differentiation, supply chain resilience, or market-specific go-to-market models — will compound meaningfully over typical equipment lifecycles and project return horizons. The growth is sufficient to sustain incumbents’ share-protection strategies while creating room for focused entrants that can exploit niches created by decarbonization and fuel-blending transitions.

Gas Engines Market

Why this research matters for 2026 corporate strategies

- Allocate capital with horizon alignment: Equipment procurement, R&D roadmaps, and manufacturing ramp-ups must be aligned to a market that is growing steadily but experiencing structural shifts. Our study ties market-scale forecasts to practical investment milestones — indicating when scale advantages are likely to materialize in core and adjacent sub-markets.

- De-risk product and fuel strategy: With multiple fuel pathways emerging (including hydrogen readiness and special gas blends), firms must assess retrofitability, certification timelines, and cost-to-market tradeoffs. The report translates macro growth into TCO and retrofit break-even frameworks for common decision pathways.

- Prioritize routes to market: The growth profile supports differentiated strategies across service, rental, CHP integration and project EPC partnerships. We map where margin accrual will likely favour OEMs versus after-market service providers in the 2026–2028 window.

- Regulatory and standards readiness: New reporting deadlines and standards are reshaping compliance costs and procurement windows. Our analysis helps companies anticipate compliance-driven demand spikes and time product launches to regulatory cycles.

What the full report delivers — actionable, executable intelligence

PW Consulting’s study is designed as a working document for executives and strategy teams. The deliverables include:

- Market size history (2020–2025) and a granular 2026–2032 forecast model that supports scenario switches (fuel mix, regulatory stress, commodity price shocks).

- Decision-ready financial templates: project-level TCO calculators, lifecycle OPEX scenarios, and ROI sensitivities for retrofit vs. greenfield investments.

- Channel and product playbooks: go-to-market matrices for OEMs, integrators, and service specialists, including recommended partnership archetypes by strategic objective.

- Regulatory impact roadmaps and compliance cost estimates linked to key reporting and standardization milestones.

- Vendor benchmarking and capability matrices (technical fit, installed base, product readiness), plus M&A and JV screening frameworks for market consolidation and scale plays.

To preserve strategic advantage, this preview avoids publishing the full segment-level breakdowns and proprietary vendor scoring that appear in the paid report. Those elements are presented in interactive dashboards in the full deliverable to support board-level decision simulations.

Competitive landscape — strategic implications for 2026

The competitive field combines global OEMs with strong installed bases and specialized regional players. The market’s structure is neither a tight oligopoly nor wholly fragmented; the top-tier players hold meaningful scale but the cumulative combined share leaves space for focused challengers. Key strategic observations for each archetype are below.

- Legacy OEMs with deep installed bases (e.g., INNIO Jenbacher): These players convert installed capacity into recurring service and upgrade revenue. Their strategic priority is to monetize lifecycle services and position “hydrogen-ready” capabilities as a premium retrofit offering. For 2026, incumbents should prioritize modular upgrade paths and aftermarket digitization to protect margins as fuel mixes evolve.

- Heavy equipment conglomerates (e.g., Caterpillar, Cummins): These vendors leverage distribution networks and diverse product portfolios to cross-sell into fleet, industrial and power applications. Their advantage lies in scale and financing offerings. Strategic action for 2026: sharpen segmented value propositions — differentiate product lines for heavy-duty vs. distributed energy while accelerating near-zero emission product certification where it opens municipal and commercial contracts.

- Specialty engine manufacturers (e.g., MAN Energy Solutions, Rolls-Royce Power Systems/mtu, Wärtsilä): These companies compete on performance, emissions control and integration with grid services. They are well-positioned for power generation and cogeneration projects demanding high efficiency and grid-stability features. 2026 bets should prioritize fast-response controls, remote diagnostics, and contracts that embed long-term service agreements.

- Industrial and off-highway specialists (e.g., Perkins Engines, DEUTZ): Focused on robust engineering for harsh environments, these suppliers can exploit aftermarket and replacement demand in remote or heavy-industrial segments. Their strategic edge lies in ruggedization and local service networks; in 2026 they should expand certified partner programmes and parts logistics to shrink downtime for field operators.

Across these archetypes, a common commercial lever is the ability to offer integrated solutions — engine plus controls, fuel handling and digital monitoring — that transform commoditized units into higher-margin, recurring-revenue systems.

Regulatory and standards dynamics shaping near-term decisions

Regulatory timing and standards updates are material to 2026 planning. Recent and forthcoming requirements — including reporting schedules for engine emissions in certain jurisdictions and updated industry guidelines on gas quality effects — change procurement windows and certification timelines. Two dynamics matter most:

- Compliance-driven procurement waves: Reporting deadlines and emission thresholds can create concentrated demand for replacement or upgraded equipment. Companies can capture outsized share by synchronizing product availability and certification with jurisdictional reporting cycles.

- Technical standards influencing performance claims: Recent guideline updates on gas quality and engine response affect warranties, performance guarantees and aftermarket service designs. OEMs that move early to validate engine performance across broader gas quality envelopes reduce contract risk and open new fuel-mix use cases.

Our full analysis overlays these regulatory timelines onto procurement forecasts so legal, commercial and product teams can coordinate launches, approvals and partner agreements to capture market windows rather than chase them.

Scenarios and decision-support for 2026

The study offers three operational scenarios calibrated for near-term decision-making:

- Base case: Continued steady growth driven by distributed power and industrial demand, with gradual fuel diversification. This scenario emphasizes product reliability, service networks and financing flexibility.

- Accelerated transition: Faster policy-driven adoption of low-carbon fuels and stricter emissions norms. Here, first-mover advantage accrues to OEMs that have certified hydrogen-capable platforms and can offer retrofit pathways.

- Commodity shock: Price volatility in natural gas increases OPEX uncertainty; buyers delay new capex and prioritize efficiency and short-term rentals. Suppliers with lean manufacturing and rental fleets perform better.

Each scenario is accompanied by prioritized actions, a list of leading indicators to monitor in 2026, and decision thresholds that convert market movement into go/no-go investment triggers.

Recommended near-term actions for executives (2026 planning horizon)

- Run a rapid portfolio stress-test using our TCO templates to identify products with the best resilience to fuel-price swings and regulatory tightening.

- Accelerate service-digitalization pilots that shorten time-to-failure detection and create recurring revenue streams within 12–24 months.

- Align product certification timelines with identified regulatory milestones to capture compliance-driven retrofit and replacement demand.

- Pursue focused partnerships — e.g., with local integrators or fuel-supply specialists — rather than broadscale M&A unless the target closes a specific capability gap identified in the scenario analysis.

Conclusion — how PW Consulting’s study supports 2026 decisions

For executives who must commit capital and resources in 2026, this Gas Engines Market study turns a steady-growth market and shifting regulatory environment into a set of actionable decision levers. By combining a rigorous forecast (historical 2020–2025 baseline with a 2026–2032 outlook at a 5.6% CAGR), decision-ready financial tools, scenario playbooks and vendor benchmarking, the research helps you prioritize investments, time product and certification efforts, and structure commercial models that protect margin through transition.

This overview is a strategic preview: it highlights the study’s depth and practical utility without publishing the full segment-level tables and proprietary vendor scores that form the core of our paid analysis. For boards, strategy teams, and commercial leaders preparing 2026 plans, the full report and its interactive dashboards deliver the calibrations and templates required to act with confidence.

Access the full analysis to obtain the complete segmentation intelligence, vendor scorecards, and downloadable decision tools that will materially improve the quality and timing of your 2026 strategic choices.

For detailed analysis of this topic, please visit the official page:Gas Engines Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com