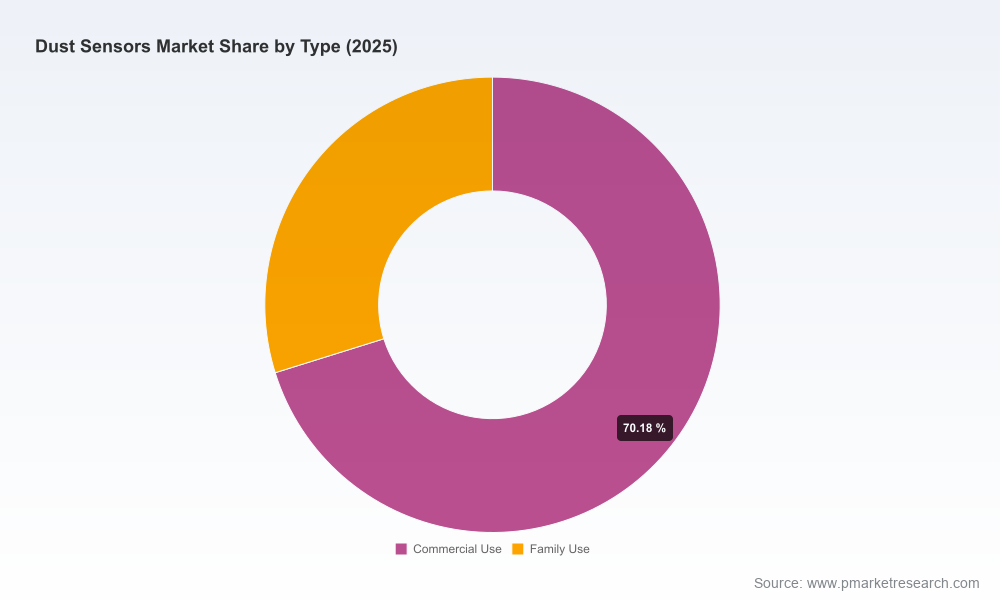

Dust Sensors Market 2026: Strategic Preview for Corporate Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused preview of our latest Dust Sensors Market study — a decision-grade, action-oriented briefing designed to inform capital allocation, product strategy, and regulatory engagement in 2026. This piece synthesizes the report’s most consequential insights without disclosing the granular segment-level intelligence reserved for subscribers. Consider it a strategic trailer: enough depth to shape near-term choices, while intentionally withholding the full model and segmentation tables to encourage retrieval of the full dossier for implementation.

Dust Sensors Market

Market snapshot: steady, predictable expansion

The global dust sensors market has moved from a niche solution set in the early 2020s toward a broadly adopted component in environmental monitoring, industrial automation, and consumer air-quality products. Our baseline (2025) places the market at USD 0.57 Billion, following steady growth through the 2020–2025 historical window. Under the report’s central forecast, the market expands at a compound annual growth rate (CAGR) of 5.4% across the 2026–2032 horizon, reaching approximately USD 0.82 Billion by 2032. This pace reflects an intersection of tightening ambient-air policies, municipal and industrial monitoring programs, and accelerating deployment of low-cost sensor networks for urban resilience.

Dust Sensors Market

Why 2026 is a pivotal year for corporate strategy

- Regulatory inflection points: New regulatory limits and monitoring directives in major jurisdictions are converting long-term policy signals into near-term procurement commitments. Organizations that align product roadmaps and sales channels to these changed compliance regimes will capture disproportionately early wins.

- Technology transition window: Improvements in optical and laser-based detection, paired with lower-cost electronics and edge analytics, create an affordable performance uplift. 2026 marks the moment to decide whether to upgrade legacy portfolios or buy-in through partnerships.

- Network economics and scale: As municipalities and industrial customers standardize on sensor classes for distributed monitoring, economies of scale in manufacturing and installation begin to favor players with integrated offerings (sensor + calibration + analytics).

- Supplier resilience and input risks: The supply chain for high-precision optical and laser components is sensitive to tooling and polymer molding capabilities; procurement strategy for these inputs will materially affect cost and lead-time through 2026–2028.

Market dynamics that will guide 2026 decisions

- Policy-driven demand: The tightened EU Ambient Air Quality Directive (Directive (EU) 2024/2881) has drastically raised the compliance bar for PM2.5 monitoring (European Commission, 2026). For vendors and systems integrators, this translates into accelerated replacement cycles for end-of-life monitors and fresh tenders from municipal and industrial buyers.

- Public-sector monitoring strategies: The U.S. EPA’s 2025–2026 priorities emphasize next-generation low-cost PM2.5 sensing in urban networks, creating procurement pathways for validated low-cost sensors (U.S. EPA, 2026). Market entrants must demonstrate traceability and calibration protocols to participate in these networks.

- Materials and manufacturing constraints: Laser-based dust sensors depend on advanced optical subcomponents and high-precision polymer injection molding. Suppliers that have secured tooling expertise and qualified polymer supply chains will enjoy lower unit costs and higher yields (Chengdu Pulse Optics-tech Co., Ltd., 2026).

- Installation and operational costs: Labor costs for installation, calibration, and network maintenance remain a significant portion of total cost of ownership for dense urban deployments. Device form factor, auto-calibration features, and robust remote diagnostics are differentiators that reduce lifecycle costs.

Competitive landscape — who matters and why

The market is characterized by a mix of specialist industrial players, sensor module manufacturers, and legacy instrumentation firms. Overall concentration is moderate: the top three players account for a meaningful but not dominant portion of the market, and the top five still leave substantial share for smaller, niche competitors. This fragmentation creates opportunities for targeted consolidation and for technology-focused entrants to capture vertical niches.

Dust Sensors Market

- ENVEA (France) — ENVEA’s ProSens and Dusty product lines position the company strongly in real-time industrial emissions monitoring and filter-leak detection. Their April 2025 launch of a next-generation Optical Aerosol Spectrometer underscores an investment strategy centered on high-accuracy, compliance-grade instrumentation and premium service contracts (ENVEA, April 2025).

- Chengdu Pulse Optics-tech Co., Ltd. (China) — A supplier focused on laser and infrared dust-sensing modules, Pulse Optics brings manufacturing depth in optical subsystems. Their emphasis on laser-based detectors aligns with applications that require high sensitivity and low detection limits, and their manufacturing notes highlight the importance of polymer tooling in sensor production.

- Cubic Sensor and Instrument Co., Ltd. (China) — Cubic’s strength lies in industrial dust sensing for powder and bulk solids leak detection. Their product set and channel relationships in heavy industries make them a go-to for process-control applications.

- Zhengzhou Winsen Electronics Technology Co., Ltd (China) — Winsen’s laser and infrared offerings target air-quality monitoring at competitive cost points. Their portfolio strategy is tailored for integrators building large sensor networks.

- Amphenol Advanced Sensors (USA) — Through brands like Telaire, Amphenol offers SMART Dust Sensor and DSF series products that target automotive and consumer air-quality segments, leveraging established distribution in vehicle and HVAC markets.

- Sensirion AG (Switzerland) — Sensirion’s SPS30 and related particulate sensors are optimized for HVAC and building-air-quality applications, combining commercial-scale manufacturability with strong calibration datasets for integration into building-management systems.

- Shinyei Corporation (Japan) — Shinyei’s PPD optical series represents a lower-power optical approach that is attractive to battery-operated and compact consumer devices, with decades-long pedigree in optical sensing.

For 2026 strategy, the competitive implications are clear: industrial-grade accuracy and certification will command premium pricing in compliance-driven tenders, while low-cost, validated modules will dominate large-scale urban sensor rollouts. Firms that bridge both—delivering modular, upgradeable platforms with certified calibration—will outcompete one-trick vendors.

Practical, operational content included in the full report

Our full study is organized to convert strategic insight into executable plans. Highlights of the deliverables include:

- Market sizing and forecast model (2020–2032) built at the device, application, and buyer-type levels — with scenario sensitivity for regulatory tightening and sensor-cost deflation.

- Buyer decision matrices that map procurement criteria (accuracy, cost, service, calibration burden) to typical tender specifications across municipalities, industrial buyers, and original equipment manufacturers (OEMs).

- Unit-cost and supply-chain heatmaps emphasizing optical-subcomponent risks, tooling requirements, and lead-time sensitivities for laser-based versus low-cost optical sensors.

- Deployment playbooks that quantify installation and lifecycle expenditures for dense urban networks, including maintenance schedules and remote calibration pathways that reduce total cost of ownership.

- Go-to-market frameworks for sensor manufacturers — channel options, value-added partnerships (analytics and managed services), and pricing archetypes.

- Competitive profiles and strategic scorecards for the key vendors mentioned earlier, plus a shortlist of potential M&A targets and partnership candidates, ranked by capability fit and acquisition complexity.

- Regulatory impact maps for major jurisdictions and compliance timelines to align product certification and sales outreach with procurement cycles.

Note: This preview intentionally omits the full segment-level breakdowns and downloadable Excel models. Those proprietary data and the full forecast engine are available only with the comprehensive report license.

Actionable recommendations for C-suite teams in 2026

- Align product certification roadmaps to regulatory timetables: Prioritize compliance-grade sensor development and third-party validations for markets where PM2.5 limits were tightened in 2024–2025. Missing certification windows will delay access to high-value tenders.

- Lock down optical-component supply: Secure long-lead tooling agreements for critical laser and lens components, or qualify alternate suppliers with equivalent polymer-molding capabilities to mitigate lead-time and cost risk.

- Adopt modular business models: Offer sensor modules with upgrade paths (firmware, calibration kits, analytics subscriptions). This enables initial low-cost deployments while preserving a pathway to higher-margin managed services.

- Invest in calibration and network O&M: Differentiate through lower lifecycle operating costs—auto-calibration, remote diagnostics, and bundled maintenance contracts beat one-off device sales in municipal and industrial procurements.

- Consider targeted M&A or partnerships: If your incumbent strength is manufacturing, consider acquiring analytics or certification capabilities; if you are an analytics firm, secure hardware partnerships to control data quality.

Conclusion — what to do next

The dust sensors market in 2026 is a market of converging vectors: regulatory mandates, technological maturation, and the economics of distributed sensing. For companies making investment and market-entry decisions in 2026, the key is to act with calibrated speed: secure your supply chain, validate devices against emerging regulatory standards, and design commercial models that capture recurring service value.

PW Consulting’s full Dust Sensors Market report provides the proprietary models, jurisdiction-level regulatory maps, supplier due-diligence templates, and scenario simulations that underpin these recommendations. Use this preview to shape board-level debate now; procure the full report to translate directional strategy into procurement specifications, product roadmaps, and M&A targets with the precision required for competitive advantage in 2026.

For detailed analysis of this topic, please visit the official page:Dust Sensors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com