How Long-Term Metabolism Adapts During Mounjaro in Islamabad

Health |

2026-06-29 04:53:59

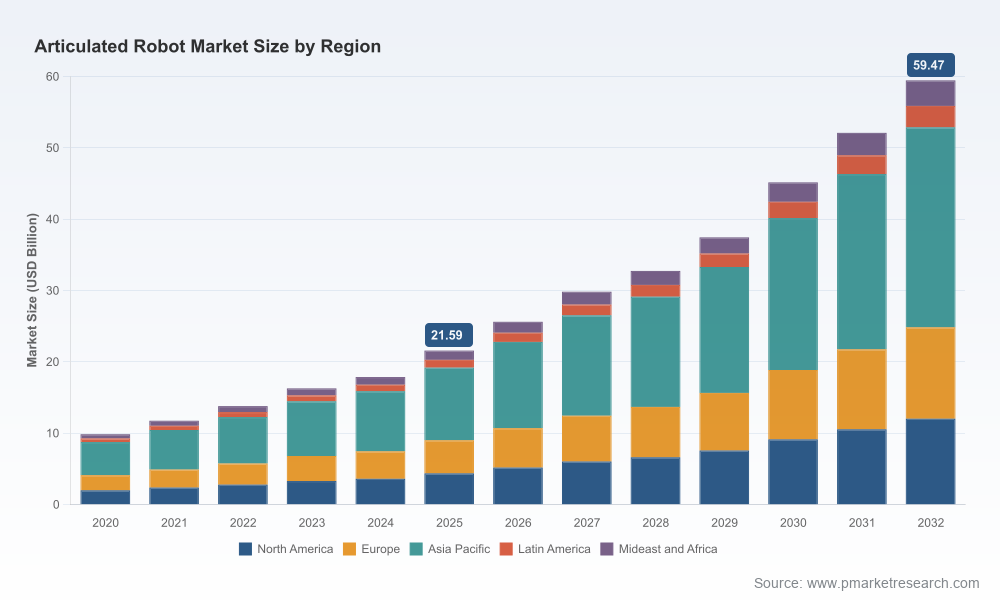

As corporations map capital allocation and operational shifts for 2026, the articulated robot market stands out as a high-conviction opportunity and a complex strategic terrain. PW Consulting’s forthcoming Articulated Robot Market study (base year 2025; historical span 2020–2025; forecast 2026–2032) quantifies a market that has more than doubled since 2020 and is projected to continue expanding at a compound annual growth rate of 15.58% through 2032. From an estimated market size in 2025 to a multi-decade expansion culminating in the late 2020s and early 2030s, the trajectory demands that executives assess manufacturing footprint, partner ecosystems, and product roadmaps with greater granularity than traditional CAPEX planning cycles have required.

Articulated Robot Market

Speed of adoption vs. deployment complexity: Robotics adoption has accelerated across industries, but the commercial value of articulated solutions depends on execution—systems integration, safety certification, and workforce enablement. Our study separates hype from investable opportunities so leaders can prioritize initiatives that materially improve throughput, quality, or unit economics.

Articulated Robot Market

Market momentum with concentrated leadership: The market shows clear scale dynamics: the top three vendors account for a majority share and the top five for a clear supermajority, indicating that competitive positioning, channel access, and IP advantages remain decisive. For buyers and OEMs, supplier selection is therefore a strategic choice that affects total cost of ownership, long-term serviceability, and upgrade paths.

Articulated Robot Market

Regulatory and geopolitical tailwinds and headwinds: New safety standards and continuing geopolitical frictions are reshaping procurement risk and time-to-deployment. Companies that proactively integrate regulatory timelines and trade-risk mitigation into procurement strategies will avoid costly project delays in 2026.

To orient executive decision-making: the articulated robot market has exhibited robust growth over the last half-decade and is forecast to continue at an elevated pace. Our modeling shows the market expanding from a sub-$10 billion industry in 2020 to a materially larger base in 2025, and on to a substantially larger market by 2032 under a 15.58% CAGR. The global installed base dynamics reported by independent industry trackers corroborate this acceleration—industrial robot installations numbered in the hundreds of thousands, with concentrated deployment activity across Asia and select advanced manufacturing clusters. These macro dynamics create a window for both aggressive growth plays and disciplined defensive moves in 2026.

Transparent market-sizing methodology: reproducible top-down and bottom-up models, sensitivity analyses, and clearly stated assumptions that allow corporate finance teams to stress-test scenarios against their internal forecasts.

Technology and deployment playbooks: implementation timelines, integration cost buckets (hardware, controls, safety engineering, software, systems integration), and best-practice checklists for ROI validation at pilot and scale phases.

Risk-adjusted go-to-market templates: supplier shortlists by application archetype, contracting constructs to protect service continuity, and recommended warranty and spare-parts strategies to minimize lifecycle cost.

Vendor evaluation matrices: a concise, comparative framework that scores vendors on product breadth, ecosystem openness, software and AI capability, service footprint, and roadmap clarity—enabling procurement committees to prioritize incumbent consolidation or strategic diversification.

M&A and partnership playbook: actionable criteria for bolt-on acquisitions, equity partnerships, and co-development agreements designed to accelerate time-to-market for differentiated automation solutions.

Executive dashboards and downloadable datasets: curated charts and raw data that finance and strategy teams can ingest directly into valuation models and operating plans. (Note: this preview intentionally omits core segment-level tables; full datasets are available in the paid report.)

The articulated robot market is populated by established global OEMs and rapidly maturing newcomers. Several firms set the technology and commercial bar; understanding their strategic posture helps corporations evaluate partner fit and competitive risk.

FANUC Corporation (Yamanashi, Japan) — A long-standing leader known for robust 6-axis articulated platforms optimized for welding, painting, assembly and precision machining. FANUC’s enduring strength is its field-proven reliability and extensive global service network. For firms prioritizing uptime and scale, FANUC remains a core consideration.

ABB Ltd. (Zurich, Switzerland) — ABB offers a wide articulated product portfolio across handling, welding, cutting and grinding applications. Recent heavy-payload specification updates from ABB indicate an emphasis on industrial-scale throughput and mission-critical deployments, attractive to manufacturers seeking high-duty-cycle automation.

Yaskawa Electric Corporation (Kitakyushu, Japan) — Known for high-performance robotics optimized for heavy-duty tasks. Yaskawa’s engineering focus tends to deliver compelling life-cycle economics for continuous-duty industrial applications.

KUKA AG (Augsburg, Germany) — Specializes in heavy-payload systems and increasingly differentiates via AI-enabled software and digital services. KUKA’s strategy is appealing to firms that view robotics as part of a broader digital transformation and data-driven production optimization effort.

Kawasaki Heavy Industries (Tokyo, Japan) — A diversified supplier with an emphasis on general-purpose manufacturing needs, with recent product introductions targeted at small-to-medium manufacturing segments in high-growth markets.

Universal Robots A/S (Odense, Denmark) — Pioneer of collaborative (cobot) articulated arms; a preferred option for small-batch, flexible production where human-robot collaboration and ease of deployment reduce barriers to automation.

Mitsubishi Electric Corporation (Tokyo, Japan) — Offers a range of vertical and horizontal articulated robots for high-volume assembly and precision tasks. Its product catalog updates reflect a continued push to serve tightly integrated assembly lines and electronics manufacturing.

Market concentration metrics demonstrate that incumbent leaders capture a majority of market value—underscoring that enterprise partner selection is not merely a procurement decision but a strategic alignment with long-term ecosystem trajectories.

Installation momentum and regional dynamics: independent monitoring of global installations in 2024 showed a sizable installed base with dominant deployment activity concentrated in Asian manufacturing hubs. For executives, this underscores where supply-chain resilience and regional service capacity matter most.

Product refresh cycles: several OEMs updated product lines and technical specifications in late 2025 and early 2026, including heavy-payload expansions and cobot portfolio refreshes. These refreshes influence replacement vs. retrofit decisions for existing automation assets.

Standards and safety: new safety parameters for collaborative robots and ongoing standards development at the ISO level require manufacturers and integrators to re-evaluate safety engineering approaches to avoid project rework.

Geopolitics and trade risk: supply-chain disruptions and trade friction observed in 2025 have measurable impacts on procurement lead times and cost of imported robotics systems—factors that should be built into 2026 sourcing strategies.

Reassess supplier concentration: With a handful of vendors controlling a majority of market share, firms should model the impact of single-supplier dependence on uptime, spare-part lead times and upgrade cost. Consider dual-sourcing critical lines and negotiating stronger service-level commitments.

Prioritize pilot-to-scale paths: Accept that many automation pilots fail to scale due to integration gaps. Focus investments on modular integration frameworks, middleware adoption, and clear success metrics that link automation to throughput and quality KPIs.

Factor regulatory timelines into deployment schedules: New safety limits and ongoing standard updates can materially affect certification and commissioning; integrate compliance milestones into project Gantt charts to avoid schedule slippage.

Design for flexibility: Where possible, choose articulated solutions and controllers that support open architectures and software upgrades, enabling future functionality (vision, force control, AI) without complete hardware replacement.

Consider M&A or strategic partnerships to close capability gaps: Whether to accelerate software competency, edge-compute capability, or service reach, inorganic options can be faster and more certain than internal development in a high-velocity market.

This overview is a strategic preview intended to inform planning cycles and executive discussions. PW Consulting’s full Articulated Robot Market study contains the underlying datasets, segment-level models, vendor scorecards, and downloadable dashboards necessary for mid-year planning and long-term capital allocation. In line with our “trailer” approach, we provide significant directional analysis here while reserving the detailed segment tables and proprietary modeling outputs for the full report—designed so subscribers can immediately operationalize findings in finance, operations, and procurement processes.

2026 is shaping up to be a decisive year for firms placing big bets on automation. With the market poised for substantial growth and ongoing shifts in standards, supply chains, and vendor strategies, executives need actionable, data-grounded insights to translate ambition into outcomes. PW Consulting’s Articulated Robot Market report combines rigorous market sizing, practical deployment playbooks, and competitive intelligence to de-risk those decisions. For the datasets, vendor evaluations, and implementation templates that make this research operational, access the full report on our website or contact PW Consulting’s strategic advisory team to schedule a briefing.

For detailed analysis of this topic, please visit the official page:Articulated Robot Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com