Unlocking Innovation: Top Cell Culture Media Market Trends Shaping the Future of Biopharma

Dance |

2026-03-30 17:03:31

As PW Consulting’s lead industry analyst, I present a focused primer on the Paint Remover Market to frame the strategic choices firms must make in 2026. This preview distills the report’s most consequential takeaways — the macro trajectory, regulatory inflection points, supplier dynamics, and actionable playbooks — while deliberately withholding the granular breakouts and proprietary spreadsheets that underpin commercial decisions. Think of this as the trailer: enough insight to inform strategy, but not the raw data that powers tactical execution. For the full dataset, interactive models, and confidential company benchmarks, please consult the full report.

Paint Remover Market

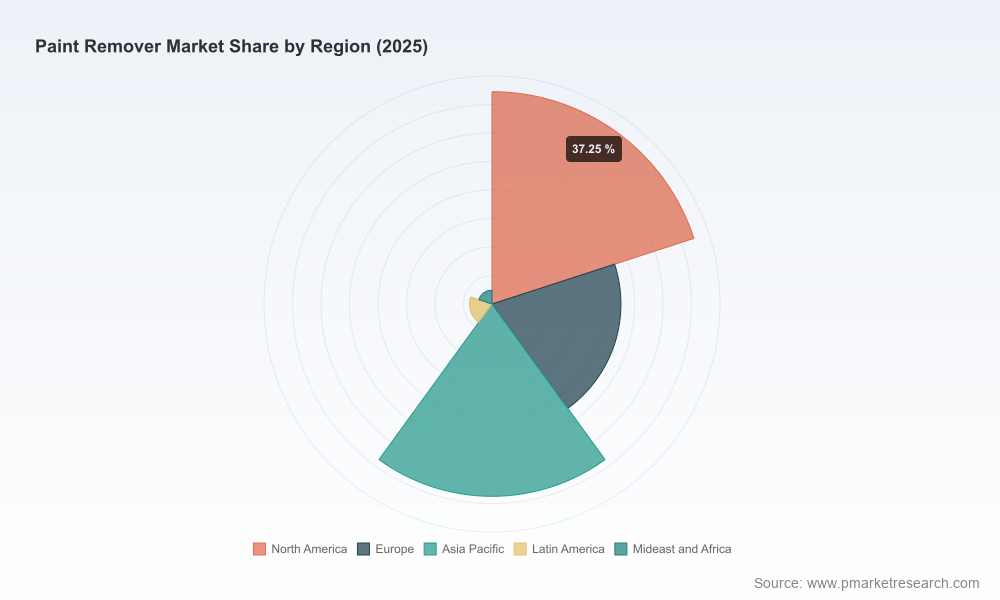

The paint remover market is on a sustained growth path. Using 2025 as the report’s base year, the global market is valued in the low‑to‑mid‑thousand million USD range and is forecast to expand at a steady compound annual growth rate of 5.6% through the 2026–2032 horizon. By the end of the forecast window the market is expected to be materially larger than today, reflecting both replacement demand driven by maintenance cycles and an expanding set of applications that favor reformulated, lower‑toxicity chemistries.

Paint Remover Market

That pace of growth is neither hyper‑expansionary nor stagnant — it is characteristic of a mature chemical-adjacent sector undergoing structural transformation. Companies that misread the rate of change risk either underinvesting in reformulation and supply‑chain resilience, or overcommitting to obsolete chemistries that face regulatory squeeze and shrinking commercial acceptance.

Paint Remover Market

Regulatory tectonics: Regulatory action is the single most consequential near‑term variable. Recent and ongoing restrictions on legacy solvents (notably methylene chloride and certain nitro solvents) have already elevated compliance costs and narrowed formulatory options for both consumer and industrial channels. Jurisdictional variance — from U.S. federal bans and state “priority product” rules to EU REACH limitations — multiplies market complexity for global suppliers and distributors.

Reformulation premium: The shift toward acetone, dimethyl carbonate, and water or bio‑based systems typically carries a per‑unit premium. Our sector analysis shows these alternatives can cost materially more on a per‑gallon basis versus legacy solvents, necessitating margin reengineering across private‑label and branded offerings.

Sustainability as a procurement filter: Rising consumer and institutional demand for biobased and low‑toxicity chemistries is creating a transparent quality signal. Products with high biobased content and credible third‑party claims are increasingly preferred in home‑improvement and certain industrial segments, altering procurement conversations and channel merchandising.

Moderate market concentration: Market concentration metrics indicate a mid‑range oligopolistic structure: a handful of suppliers hold meaningful share, but there remains room for challengers with differentiated technologies or distribution strategies. This configuration favors both focused incumbents and nimble specialists targeting underserved niches.

Cost and supply‑chain volatility: Feedstock and logistics pressures — compounded by the cost differentials of greener chemistries — demand that firms redesign procurement contracts, hedging strategies, and packaging efficiencies to protect margins while meeting regulatory and customer expectations.

The competitive picture is a mix of technology push and channel push. Established industrial chemical companies and paint manufacturers are retooling portfolios to meet regulatory and buyer expectations, while specialized formulators and private brands are capturing share through focused product claims and channel intimacy.

Product innovation: Market leaders are introducing advanced formulations that remove the most hazardous solvents, prioritize biodegradability, or leverage high percentages of biobased content. Some launches explicitly target low‑odor profiles and improved worker safety, responding to both regulation and installer sentiment.

Channel and use‑case differentiation: Brands are bifurcating offerings for verticals — from consumer home‑improvement gels tailored to DIY applications, to higher‑performance industrial strips optimized for metal and infrastructure maintenance. This segmentation of go‑to‑market approaches will be a decisive battleground in 2026.

R&D footprint expansion: Investments in European and North American R&D centers signal an acceleration in sustainable stripping technologies aligned to regional chemical safety directives. Firms expanding R&D capacity are positioning for lead‑market advantage as regulation tightens.

Recent product introductions across the competitive set underscore these trends: new eco‑formulations with high biobased percentages, gel products suited to vertical surfaces and detailed renovation work, and next‑generation solvent systems emphasizing lower odor, improved biodegradability, and reduced worker exposure. These moves are tacit admissions that legacy chemistries are being phased out of mainstream commercial channels.

For corporate leaders planning capital allocation, portfolio strategy, or M&A in 2026, the market presents both defensive and offensive opportunities. The following strategic imperatives should frame boardroom conversations:

Accelerate safer‑chemistry migration: Prioritize R&D and pilot manufacturing for formulations that remove or replace regulated solvents. Time‑to‑market will determine who captures reformulation premiums and secures preferred supplier status with large distributors and institutional purchasers.

Reprice and reframe value: Where reformulation increases per‑unit cost, shift from commodity pricing to value‑based propositions emphasizing total cost of ownership (TCO), reduced regulatory risk, and lower operational controls. Bundled safety services and application guidance unlock margin beyond unit economics.

Harden supply chains: Diversify feedstock sources for alternative solvents and fortify logistics for higher‑cost chemistries. Negotiate long‑term offtakes where possible and model multi‑stress scenarios to quantify margin exposure under supply disruptions.

Channel segmentation and sales plays: Develop distinct offers for DIY retail, professional refinishers, and industrial maintenance. Invest in point‑of‑sale education, technical application guides, and contractor loyalty programs to reduce friction during conversion to new products.

M&A and partnerships: Target niche formulators, bio‑chem specialists, or regional distributors to accelerate capability build without the full cycle of in‑house development. Acquisitions should be evaluated not only for revenue accretion but for regulatory moat and IP that simplifies compliance across jurisdictions.

Regulatory foresight as a product feature: Make compliance an explicit selling point. Certifications, third‑party biobased verification, and clear exposure mitigation claims reduce buyer hesitation and can justify price premiums.

This research product is designed as an operational playbook for executives and strategy teams. Highlights include:

Granular market forecasts (2026–2032) with downloadable time‑series for scenario modelling and sensitivity testing.

Segment‑level analyses by product type, application, and region, linked to margin profiles and buyer economics (note: these segment datapoints are available only in the full report).

Competitive benchmarking: R&D pipelines, recent launches, strengths/weaknesses, and strategic intent for market participants across the value chain.

Regulatory risk matrix that maps jurisdictional controls to product portfolios and flags near‑term compliance cliffs.

Supply‑chain heat maps and a supplier scoring tool to prioritize dual‑sourcing and resilience investments.

Commercial playbooks for pricing, channel segmentation, and marketing claims that convert technical benefits into purchasing decisions.

M&A screening templates and valuation multiples adjusted for regulatory uncertainty and reformulation capex.

Primary research summaries: interviews with formulators, industrial buyers, and retail category managers that validate adoption assumptions and friction points.

Executives should fold the macro view and the strategic imperatives into three practical planning horizons:

Immediate (0–12 months): Lock in compliant supply arrangements, pilot reformulated SKUs with controlled channel partners, and implement updated safety and labeling protocols to avoid regulatory disruption.

Near term (12–24 months): Scale successful reformulations, codify value‑based pricing, and negotiate distribution agreements where sustainability credentials are preferentially rewarded.

Medium term (24–48 months): Consider acquisitive moves to secure IP, expand into adjacent maintenance chemistries, or vertically integrate supply of alternative solvents where it enhances margin resilience.

2026 is a turning point for the paint remover market: the interplay of regulation, rising demand for safer alternatives, and a manageable growth rate creates a window where smart, timely moves deliver disproportionate returns. Whether you are a manufacturer reengineering product lines, a distributor rationalizing SKUs, or an investor sizing M&A targets, the choices you make this year will determine competitive positioning for the remainder of the decade.

This article has highlighted the strategic contour and 실무 guidance embedded in PW Consulting’s full market study. To access the full suite — including the segment‑level forecasts, company model sheets, supplier scorecards, and customizable scenario tools — please consult the full report and our advisory team for a tailored executive briefing and interactive workshop.

For detailed analysis of this topic, please visit the official page:Paint Remover Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com