LED Glass Market 2026: Strategic Preview for Executive Decision‑Making

As PW Consulting’s Senior Strategy Advisor and Lead Industry Analyst, I present a focused, executive‑level preview of our 2026 LED Glass Market study. This introduction synthesizes the macro drivers, near‑term inflection points and strategic implications that matter for boardrooms, corporate strategy teams and transaction advisers preparing for decisions in 2026. The aim is to establish the study’s strategic value while reserving the granular segment tables and proprietary forecasts for the full report—this “trailer” is intended to demonstrate analytical rigor and practical orientation, not to substitute for the primary deliverable.

LED Glass Market

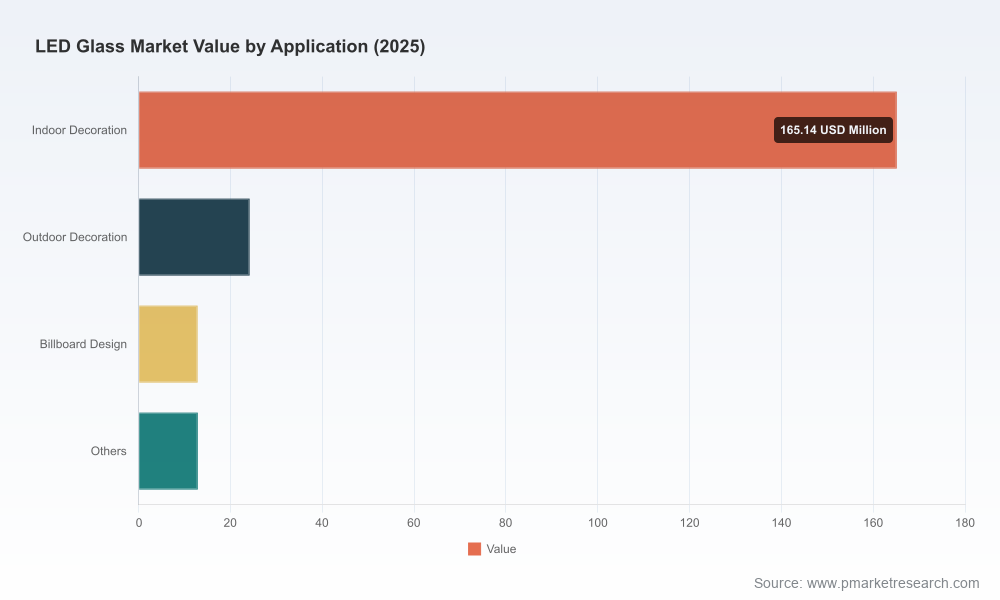

Market at a Glance: What the headline numbers tell us

LED glass—where active LED elements are integrated with architectural glass substrates—has transitioned from a novel spectacle to a considered component in retail, commercial and specialized sports and entertainment applications. Our market model, base year 2025, shows the industry growing from a mid‑double‑digit USD million base in 2020 to a materially larger market by 2025, and projecting to expand through the forecast window 2026–2032 at a compound annual growth rate of 9.58% (USD Million basis). By 2032 the market reaches a substantially higher level compared with 2025, reflecting both increased adoption and higher‑value configurations entering projects.

LED Glass Market

These headline dynamics are important for 2026 planning: the underlying CAGR signals market resilience beyond one‑off installation cycles, while the historical growth trend evidences accelerating enterprise adoption that is now intersecting with shifts in standards, raw‑material cycles and high‑visibility use cases that will shape supplier economics and go‑to‑market choices over the next 18–36 months.

LED Glass Market

Why 2026 is a Strategic Inflection Year

- Standards and certification convergence: 2025–2026 has seen important momentum toward harmonized standards for smart and thin‑film glass technologies. Global alignment around smart glass standards and recent updates that address thin‑film performance are lowering a key barrier to specification in international projects. For firms planning product roadmaps or certification budgets in 2026, the timing is critical—early compliance yields specification advantage, late compliance can lock suppliers out of high‑value contracts.

- Raw‑material and input cost dynamics: Feedstock volatility—particularly soda ash dynamics—has moved from a headline risk to a tactical procurement lever. After a 2025 decline in soda ash prices driven by oversupply and weak industrial demand, prices traded at depressed levels into mid‑2026. That temporary easing creates an acquisition and inventory planning window for manufacturers that can convert spot relief into sustainable cost advantage through procurement restructuring and supply‑contract renegotiation.

- Commercial validation through marquee deployments: High‑visibility deployments—including the use of LED glass floors in major sporting events announced in 2026—are accelerating buyer confidence across facility owners, venue operators and flagship retail formats. These proof points materially shorten the sales cycle for premium configurations and increase the willingness of integrators to propose LED glass in mainline projects.

Strategic Implications for Corporate Decision‑Makers

Decisions that must be made in 2026 fall into three practical categories: go‑to‑market (GTM), product and supply chain. Below are the prioritized strategic implications we identify for each.

- GTM and channel strategy: As LED glass moves from showcase to specification, winning becomes about ecosystem positioning. OEMs and integrators that invest in architect/specifier outreach, packaged compliance documentation and a limited set of high‑impact reference projects will capture the premium segment. Partnerships with venue owners and sport/event organizers—already visible in recent announcements—are effective accelerants for market credibility.

- Product roadmap and certification investments: Thin, laminated and transparent LED solutions face distinct safety glazing and building‑code hurdles in some jurisdictions. Certification pathways such as ANSI Z97.1 (and local equivalents) remain gating factors for adoption in retrofit and occupied space projects. Firms must budget for testing and design iteration early in 2026 to avoid specification delays later in procurement cycles.

- Supply chain resilience and cost management: With soda ash and other glass inputs experiencing cyclical softness, 2026 is the right time to redesign supplier contracts—shifting toward blended sourcing, indexed pricing collars and strategic buffer inventory where capital allows. Manufacturers that convert short‑term raw‑material relief into longer‑term cost efficiency will enjoy margin leverage as demand resumes full acceleration.

Competitive Landscape — Who Matters and Why

The LED glass value chain today remains fragmented, with a small number of specialized innovators and numerous regional fabricators competing on execution and integration services. Market concentration metrics indicate a relatively open market—top supplier groups represent a modest share of the total market—so there is room for both focused incumbents and well‑backed challengers to scale.

- Clear Motion Glass (York, PA, USA): Specializes in cvLED transparent LED glass with laminated, surface‑applied and ceiling‑hung configurations designed for high‑resolution architectural displays. Their positioning—integrating safety‑grade architectural glass with embedded LEDs—targets premium specifications where resolution, optical clarity and safety compliance are mandatory. For companies evaluating partnerships or acquisition targets, Clear Motion’s integration depth and product modularity are strategic assets.

- Glasstronn (Bangalore, India): Focuses on transparent glass LED systems for retail and commercial facades, emphasizing ultra‑transparent aesthetics and local manufacturing agility. Glasstronn’s thought leadership—publishing practitioner‑oriented pieces on switchable glass and transparent LED trends in 2026—demonstrates an effective content strategy to influence architects and façade consultants in growth markets.

These firms illustrate two scalable plays in the market: technology‑driven premium solutions for high‑spec clients, and agile, regionally focused players leveraging local relationships and competitive pricing. Investors and corporate strategy teams should evaluate targets against five dimensions: product IP and modularity, certification status, integration capability, distribution and reference projects, and procurement resilience.

Regulation, Standards and Raw Materials — The Underappreciated Constraints

- Certification as a gating variable: Safety glazing certification remains a practical hurdle for thin glass adoption in some key markets, with ANSI Z97.1 testing and analogous local approvals required for building‑code compliance. Firms that delay certification investments will materially impair their ability to compete on retrofit and occupied‑space projects.

- Standards harmonization as an adoption accelerator: The recent movement toward global harmonization—reflected in updates to smart glass standards and the new thin‑film guidance—will reduce project friction for multinational deployments. Early adopters who design to these converged standards will shorten sales cycles with multinational clients and reduce re‑engineering costs across markets.

- Input cycle opportunity: Soda ash, a key feedstock for glass manufacture, softened through 2025 as oversupply pressured prices. By June 2026, soda ash trade reported lower levels relative to prior year benchmarks, creating a procurement window. Manufacturers should model both short‑term price relief and potential rebound scenarios when negotiating supplier agreements and hedges.

What the Full Report Delivers — Practical, Transaction‑Ready Assets

Our full LED Glass Market study is organized to support immediate 2026 decision workflows. Key deliverables include:

- Actionable market sizing and a validated forecast model (2026–2032) with scenario runs for adoption velocity and pricing evolution.

- Regional and application segmentation (detailed), with demand drivers and adoption timelines mapped to procurement cycles—note: this introduction intentionally omits granular split tables to preserve the report’s commercial value.

- Supplier scorecards and a competitive matrix covering technology differentiation, certification status, reference projects and channel reach.

- Regulatory and standards compliance playbook, including test‑plan templates for safety glazing certification and a timeline for anticipated harmonization impacts.

- Supply‑chain playbook and cost sensitivity analysis that models raw‑material scenarios (including soda ash price pathways) and recommended contracting strategies.

- M&A and partnership playbook: target prioritization, integration risk checklist and illustrative valuation sensitivities tuned to the market’s current concentration dynamics.

- Implementation roadmaps for three typical buyer archetypes: infrastructure owners (venues and large retailers), premium façade integrators and technology OEMs seeking to enter the space.

How to Use the Insights in 2026 — Three Immediate Actions

- Front‑load certification and compliance: Allocate budget and technical resources to secure necessary glazing and product certifications in target markets. This prevents specification bottlenecks and allows firms to price for certainty rather than risk.

- Lock in advantageous procurement terms: Use the temporary softness in glass feedstocks to renegotiate supplier contracts with multi‑year collars or to secure strategic inventory positions that smooth input price volatility into 2027–2028.

- Prioritize reference projects and strategic partnerships: Invest in a small portfolio of high‑visibility installations that demonstrate longevity and serviceability. Partnerships with event owners and integrators—evident in recent 2026 announcements—accelerate acceptance among conservative buyers.

Final Note — Why Read the Full Report

This introduction has summarized the macro trajectory, critical inflection points and the operational levers that will determine winners in the LED glass market in 2026. For boards and executive teams preparing capital allocation, product investment or M&A moves this year, our full report provides the missing elements required to act: the segment‑level demand matrices, supplier market‑share detail, region‑by‑region adoption timelines and downloadable templates for procurement and certification projects. We deliberately withhold the granular split tables and company‑level market shares here to preserve the report’s strategic utility—those datasets and the interactive forecast model are available on the report landing page.

PW Consulting’s LED Glass Market study is designed to convert macro insight into executable programs: from a six‑month certification sprint to a 24‑month GTM rollout or an acquisition due diligence package. If your 2026 plans include product launches, vertical expansion, or acquisition activity in LED glass, the full study is the decision‑grade input you should build around.

For detailed analysis of this topic, please visit the official page:LED Glass Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com