Experts Predict Geothermal Power Infrastructure Market to Thrive Amid Rising Demand

Other |

2026-05-08 10:28:18

PW Consulting presents a concise strategic brief that frames our full Fiber Cement Board Market study for executive teams preparing decisions in 2026. The industry is beyond niche: after growing from roughly USD 105 million in 2020 to about USD 133.1 million in 2025, the market is forecast to continue its steady expansion at a compound annual growth rate of 4.88% through our 2026–2032 horizon, approaching the high‑one‑hundreds by 2032. This brief highlights the decision‑critical implications embedded in our analysis while deliberately withholding granular segment tables and regional splits to encourage direct engagement with the underlying dataset and models.

Fiber Cement Board Market

Capital allocation and capacity planning: With leading manufacturers announcing capacity investments to secure near‑term demand, companies must reconcile short‑term throughput expansion against medium‑term demand scenarios. Our study converts the headline CAGR into scenario‑level production planning and capex timing to minimize idle assets and maximize first‑mover advantage.

Fiber Cement Board Market

Portfolio prioritization: The fiber cement market is transitioning in raw material composition and product positioning. Firms must decide whether to push premium architectural cladding, resilient exterior systems, or commoditized backer boards—each has materially different margin and working‑capital characteristics. Our report maps product economics to revenue and margin scenarios for 2026 tactical plans.

Fiber Cement Board Market

Regulatory and procurement alignment: Several product and certification dynamics (fire, hurricane, Buy America) are already influencing procurement flows for infrastructure and residential programs. Procurement and compliance teams will use our regulatory matrix to align sourcing, qualify factories, and accelerate spec approvals.

M&A and partnership playbook: As market concentration remains meaningful and selective capacity investments are underway, the most effective M&A playbooks are those that combine near‑term demand capture with long‑term technology and raw‑material access. The study provides a prioritized list of targets and partner archetypes tied to ROI windows relevant to 2026 boardroom decisions.

Bottom‑line market sizing and forecasts (2020–2032) with scenario variants calibrated to input shocks (raw material prices, construction activity swings, and trade policy shifts).

Go‑to‑market playbooks for suppliers and distributors: product positioning, pricing ladders, channel segmentation, and sample marketing narratives differentiated by durability and sustainability claims.

Supply chain and procurement risk register: single‑source exposures, logistics bottlenecks, lead‑time sensitivities, and mitigations including nearshoring and multi‑sourcing strategies.

Raw material cost and substitution analysis: sensitivity models that quantify margin erosion or enhancement under different cellulose/carbon‑based mix assumptions and transport cost regimes.

Regulatory compliance matrix and certification pathways across key markets—practical checklists for product testing, labeling, and approvals that shorten time‑to‑specification for large construction programs.

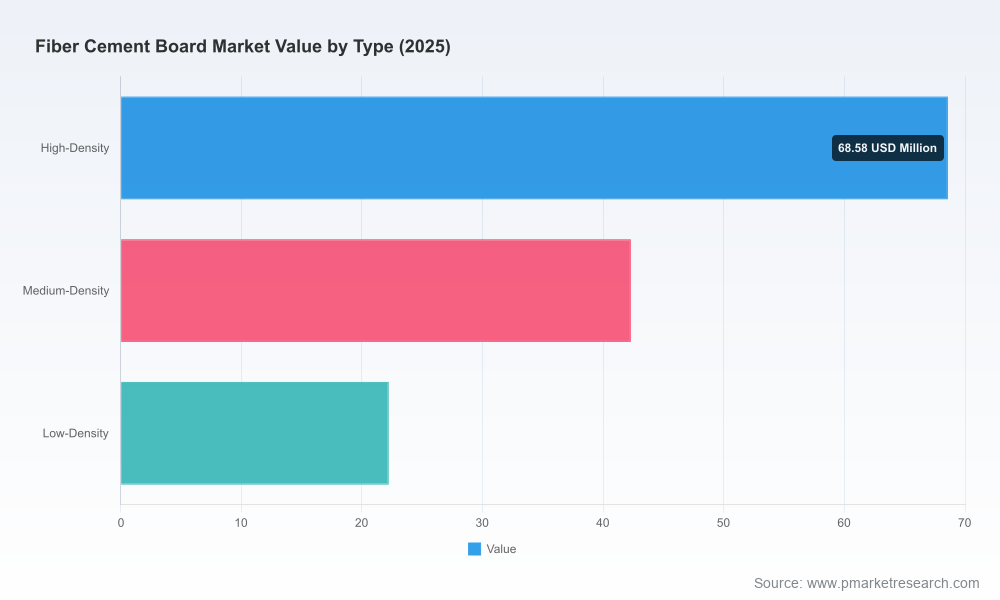

Competitive benchmarking and capability maps featuring plant footprints, primary product families, and technology differentiators (e.g., high‑density vs. medium/low‑density manufacturing platforms).

M&A and JV decision frameworks including valuation priors, integration scorecards, and synergies templates aligned with 18–36 month payback expectations.

Resilience and safety are premium decision criteria. Building codes and client specifications increasingly prioritize non‑combustible materials and systems that withstand severe weather. Several market participants already hold approvals for high‑velocity hurricane zones and wildland‑urban interface (WUI) certifications; these approvals are translating into bounded demand corridors in codes‑driven projects.

Sustainability is reframing raw material choices. Cellulose fiber has emerged as the fastest‑growing raw input, expanding at a double‑digit rate through 2026, driven by client sustainability preferences and regulatory pressure to reduce embodied carbon. The adoption curve for cellulose‑heavy mixes creates supply‑side winners and losers depending on upstream relationships with fiber suppliers.

Supply chain and procurement nationalism matter. Domestic production certifications and Buy America approvals have become commercial differentiators in several procurement categories. Manufacturers with local manufacturing and certification advantages are winning projects that would otherwise flow to imports or global suppliers.

Product durability and lifecycle performance are monetizable. Non‑combustible ratings, color stability under high UV exposure, and engineered resilience to moisture and freeze‑thaw cycles are frequently written into specifications. Producers who can demonstrate longer warranty‑adjusted lifecycles command premium pricing and lower effective total cost of ownership for buyers.

The market exhibits a mix of global platform players and strong regional specialists. Below we summarize the strategic posture of the principal players tracked in our study and highlight the operational moves to monitor through 2026.

James Hardie (Australia) — A global leader with broad exposure in siding and backer boards. The company has publicly announced multi‑million dollar capacity investments to support growth, signaling an intent to defend share and capture replacement and new‑build demand. Strategic focus: scale, channel penetration, and product consistency under harsh UV and fire performance claims.

Nichiha Corporation (Japan) — Known for high‑performance architectural siding and panels, Nichiha emphasizes resilient exterior cladding with certifications for hurricane and WUI performance. Their Buy America and domestic manufacturing moves enhance their competitiveness in code‑driven public and private projects. Strategic focus: certification‑led differentiation and resilient product suites.

Etex Group / EQUITONE (Belgium) — A European leader in high‑density cladding and aesthetic architectural panels, leveraging international production networks. Strategic focus: design‑led premium segments and specification channels (architects and façade consultants).

Swisspearl Group (Switzerland) — Specializes in architecturally oriented high‑density panels and cladding. The company competes on premium finish, longevity, and specification support in design‑heavy projects. Strategic focus: architectural niches and long‑tail façade opportunities.

Everest Industries (India) — A resilient regional producer offering asbestos‑free boards for interiors and exteriors; positioned for home‑builder and modular construction partnerships in fast‑growing markets. Strategic focus: cost competitiveness and rapid distribution reach.

American Fiber Cement Corporation (USA) — North America–focused manufacturer and distributor of compressed high‑density panels; benefits from proximity to demand centers and local code familiarity. Strategic focus: channel depth in North American retrofit and commercial markets.

SCG Building Materials (Thailand) — A broad‑based supplier with global distribution for wall, ceiling, and flooring applications; competes across value tiers and geographic markets. Strategic focus: regional scale and product diversification.

Nichiha showcased Made‑in‑USA resilient exterior cladding at a major architecture conference, directly targeting specification channels for hurricane‑resistant and fire‑rated panels. Expect follow‑through in local project awards and specification wins as architects and owners prioritize certified resilience.

James Hardie’s announced capacity expansion program (notable multi‑million dollar commitment for fiscal 2026) signals a push to secure incremental market share and to meet anticipated replacement and new‑build demand. Competitors and suppliers must anticipate increased competitive pressure on prices and raw‑material volumes.

On raw materials, the acceleration of cellulose fiber usage creates upstream concentration risk for firms that have not secured long‑term supplier agreements. The shift to bio‑derived fibers is also a potential avenue for marketing sustainability credentials—if verified by lifecycle assessments.

Immediate diagnostics (0–30 days): run the report’s procurement checklist to validate supplier qualifications against code and Buy America requirements; validate inventories against scenarios for 2026 demand acceleration.

Operational levers (30–90 days): adjust short‑term production schedules, negotiate conditional offtake with cellulose suppliers, and pilot altered product mixes for high‑margin architectural channels.

Strategic moves (90–180 days): accelerate certification programs where incremental revenue justifies the cost; evaluate bolt‑on acquisitions and capacity partnerships that shorten time‑to‑market for resilient cladding systems.

This brief intentionally surfaces the direction, drivers, and decision levers central to 2026 planning while omitting the detailed regional, type, and application splits that operational teams need for budgeting and site‑level planning. The full PW Consulting report contains the granular segment tables, downloadable models, supplier scorecards, and regulatory checklists you will need to operationalize the strategic options outlined here. For teams preparing board presentations or capex approvals this year, those attachments convert the study’s scenarios into executable financials and integration plans.

PW Consulting stands ready to run a compact, client‑specific workshop to translate the study’s scenarios into a prioritized implementation roadmap tailored to your footprint, product mix, and risk tolerance. Engage with our industry practice to obtain the full dataset and a customized 90‑day action plan that aligns with your 2026 objectives.

For detailed analysis of this topic, please visit the official page:Fiber Cement Board Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com