Online Accounting Software Market — Strategic Primer for 2026 Decision-Makers

Market snapshot

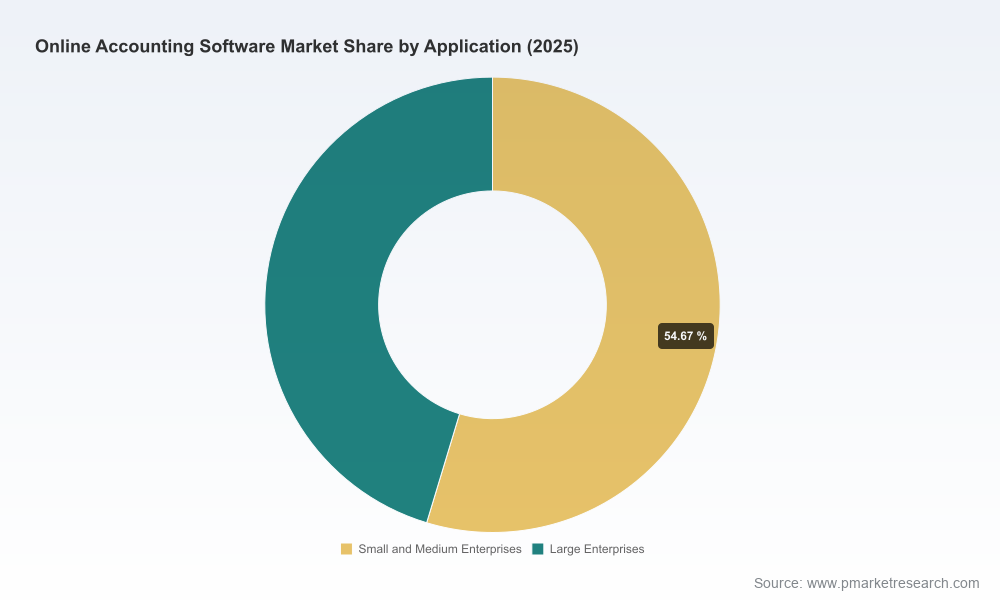

By the end of the base year (2025), the global online accounting software market crossed the threshold of roughly USD 14,000 million (≈ USD 14 billion). The sector is not mature but is moving into a phase of sustained scale: our forecast shows a compound annual growth rate (CAGR) of 9.6% across the 2026–2032 horizon, pushing the market toward the mid‑tens of billions by 2032. Market concentration sits at meaningful but not prohibitive levels (the top three and five vendors control a plurality, not a monopoly), creating space for both entrenched platforms and fast‑moving challengers.

Online Accounting Software Market

Why this research matters for 2026 strategy

- Timing and Spend Allocation — The market is large and accelerating. Boards and investment committees need to reconcile the growth trajectory for online accounting capabilities with multi‑year capital plans and cloud operating budgets.

- Product & Technology Roadmaps — Cloud accounting is becoming a vector for AI, bank integrations, and embedded financial services. Product leaders must prioritize which capabilities to build, buy, or partner for 18–36 month roadmaps.

- Go‑to‑Market and Channel Strategy — Sales motions are bifurcating: self‑serve, partner ecosystems, and embedded bank or ERP offers. Commercial leaders who align channel investment to these motions will capture disproportionate share.

- Regulatory & Infrastructure Risk Management — Cost and timing of cloud deployment are increasingly influenced by data‑center economics, permitting delays, and local sustainability requirements. Procurement and legal teams must update vendor selection criteria accordingly.

Dynamics shaping 2026 decisions

Several intersecting forces are creating both opportunities and constraints for organizations investing in online accounting solutions:

Online Accounting Software Market

- AI acceleration: Generative and task‑oriented AI have moved from experimental to operational. Vendors are shipping AI assistants and automated reconciliation engines that materially reduce routine bookkeeping effort — a structural productivity lever for small businesses and accounting firms alike.

- Embedded financial services: Increasingly, banks and fintechs are bundling payments, credit, and cash management with accounting workflows. Strategic partnerships and platform integrations will determine who captures wallet share beyond core software licensing.

- Infrastructure costs and permitting friction: Hyperscale cloud workloads — including AI training and inference — drive up data center electricity and capital intensity. Recent studies and industry reports show electricity demand for cloud/AI workloads could more than double by 2030, and a sizeable portion of infrastructure capital is delayed in permitting pipelines. These realities increase hosting and compliance costs for providers and can extend deployment lead times for large enterprise customers.

- Regulatory scrutiny and local policy: Municipal permitting, ROI recalibrations for data center incentives, and community pushback on development are reshaping how and where cloud providers expand capacity. This has knock‑on effects for service latency, sovereign data considerations, and sustainability reporting obligations for accounting platforms.

Competitive landscape — what to watch

The vendor field is a mix of category incumbents, focused specialists, and emergent AI‑first entrants. Each class presents different strategic considerations for buyers, partners, and investors.

Online Accounting Software Market

- Intuit (QuickBooks Online) — A leader in the small‑business cloud accounting category that has invested heavily in AI for bookkeeping, invoicing, and real‑time insights. Intuit’s scale, partner ecosystem, and developer footprint make it the default consideration for many SMB deployments; competitive responses should target differentiated integrations and verticalized workflows rather than feature parity.

- Xero — A cloud‑native platform focused on automation and real‑time bank sync, with a strong position among small and mid‑sized enterprises. Xero’s emphasis on open integrations and multi‑currency support makes it attractive for internationally oriented SMEs and accounting firms seeking extensible platforms.

- Sage Group — Positioned toward mid‑market and enterprise clients with advanced financial consolidation and subscription billing capabilities. Sage’s investments in regional scale (including new North American facilities) suggest a go‑deeper strategy in larger accounts and partner services.

- Wave Financial and FreshBooks — Specialists in the lower end of the market and service‑oriented businesses, differentiated by pricing models, simple UX, and features that address freelancers and small service firms. These vendors are acquisition targets for larger players seeking to expand addressable markets.

- Zoho Books — Part of a broader SaaS suite and attractive for startups and cost‑sensitive customers who value integration across CRM, HR, and finance. Zoho’s platform play is a reminder that accounting is often bought as a piece of a broader operational stack.

Recent product and corporate moves underscore the pace of innovation and competition: enterprise vendors have added generative assistants to accelerate report drafting; fintechs and banks are integrating accounting into commercial banking platforms; and AI‑native challengers are promising near‑perfect reconciliation accuracy. These developments compress time‑to‑value for buyers but increase churn risk for vendors that cannot operationalize AI safely and scalably.

Practical contents of the full PW Consulting report

This market brief is a gateway to a comprehensive toolkit designed for executives who must act in 2026. The full report includes:

- A validated market size and seven‑year forecast model with multiple scenarios (base, upside, downside) to stress‑test investment cases.

- Actionable segmentation and buyer personas that map procurement criteria to company size, vertical, and deployment model.

- Vendor scorecards and a competitive heat map that rate providers against functional modules, integration maturity, and operational risk.

- Detailed go‑to‑market playbooks for vendors and channel partners, including pricing frameworks, partner incentive structures, and ARR vs. one‑time revenue tradeoffs.

- M&A and investment screening criteria informed by technology debt, data residency posture, and AI readiness.

- Procurement checklists and SOW templates that accelerate vendor selection while mitigating compliance, security, and sustainability risks.

- Scenario planning tools that quantify the impact of infrastructure delays, rising energy costs, and regulatory changes on operating margins and TCO.

Strategic recommendations for stakeholders in 2026

Based on market size, growth trajectory, and structural dynamics, we recommend a stratified approach:

- For corporate buyers and CFOs: Prioritize platforms with clear AI governance, resilient hosting options, and a documented roadmap for data portability. Negotiate SLAs that reflect regional deployment constraints and energy‑related cost escalations.

- For technology product teams: Invest in modular, API‑first architectures and pragmatic AI features that demonstrably reduce manual effort. Consider verticalized templates for high‑value industries (professional services, e‑commerce, franchise models).

- For investors and M&A teams: Focus diligence on vendors with defensible integration networks, recurring revenue quality, and low customer concentration. Pay attention to providers that have realistic plans to mitigate rising infrastructure and compliance costs.

- For banks and financial services firms: Evaluate embedded accounting as a route to deeper commercial relationships. Integration can unlock upstream lending and payment revenue, but execution requires tight UX and reconciliations that map to underwriting workflows.

Risks and leading indicators to monitor

- Infrastructure availability and cost: Watch hyperscaler capacity announcements, regional permitting outcomes, and utility commitments for renewable power. These factors will materially affect vendor margins and deployment timelines.

- Regulatory fragmentation: Monitor state and national data‑sovereignty rules and permitting policies that could force multi‑jurisdiction hosting or segmented feature sets.

- AI operational risk: Track vendor disclosures on model accuracy, auditability, and the percentage of tasks automated. Operational failures in reconciliation or tax reporting can produce outsized liability.

- Consolidation waves: Given the CR3/CR5 dynamics, expect further M&A as incumbents buy scale and challengers sell to strategic acquirers; this will reshape channel options and integration costs.

How to use this research in 90‑, 180‑ and 360‑day plans

- 90 days: Run a vendor short‑list using our procurement checklist; pilot AI‑enabled reconciliation on a representative ledger; validate hosting and SLAs against your compliance matrix.

- 180 days: Finalize product integration priorities, sign partner agreements for payments or lending embedments, and begin a phased migration for prioritized business units.

- 360 days: Measure economic outcomes (cost of accounting per transaction, days to close), iterate on automation thresholds, and review strategic vendor consolidation or acquisition targets informed by the report’s scenario outputs.

Intentional omission — and why it matters

This introduction is designed as a strategic "trailer": it highlights the market direction, structural forces, and playbook‑level recommendations you need to make timely 2026 decisions. To preserve actionable differentiation for decision‑makers and advisory clients, we have intentionally withheld granular regional splits and fine‑grained segment metrics in this preview. Those data and the interactive models are available in the full PW Consulting report, where you can run bespoke scenario permutations relevant to your organization.

Next steps

If you are evaluating platform choices, allocating near‑term budget, or building an M&A pipeline, the full report and its model will materially shorten your decision cycle and reduce execution risk. Contact PW Consulting to access the comprehensive dataset, vendor scorecards, and tailored scenario runs that underpin the conclusions summarized here.

For detailed analysis of this topic, please visit the official page:Online Accounting Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com