Car Mounted Ceiling Screen Market 2026 to Reach US$ 1.50 Billion by 2034 at 23.0% CAGR

Other |

2026-06-23 11:05:48

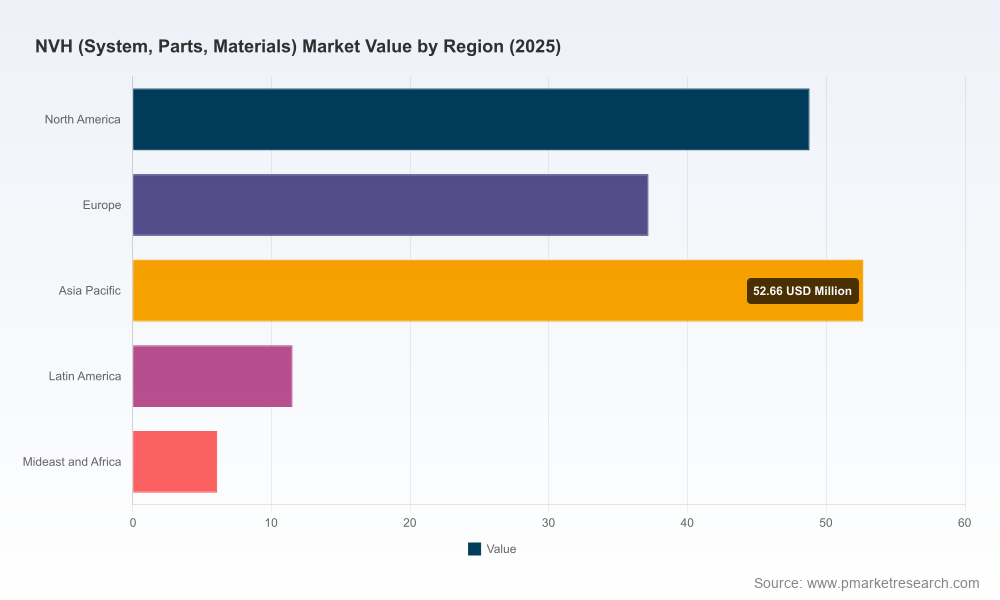

By the end of the 2020–2025 historical window, the global NVH market has demonstrably expanded, driven by rising regulatory thresholds, powertrain transitions, and customer expectations for refined cabin experiences. Using 2025 as our base year, PW Consulting’s latest analysis places the 2025 global NVH market at USD 156.2 Million (revenue unit: Million USD). Looking forward through a 2026–2032 forecast horizon, the market is projected to grow at a compound annual growth rate (CAGR) of 4.35%, reaching an anticipated market scale by 2032 consistent with mid‑single digit expansion driven by material upgrades, BEV platform adaptations, and continued regulatory tightening. The competitive landscape remains fragmented: the combined share of the leading three and five players is modest relative to total market breadth, underscoring consolidation and differentiation opportunities for 2026.

NVH (System, Parts, Materials) Market

Regulatory inflection points are operational imperatives. New and more stringent noise limits in major jurisdictions — including passenger car thresholds now enforced within EU/ECE frameworks — are forcing both OEM engineering and supplier material selection toward higher‑performance NVH solutions.

NVH (System, Parts, Materials) Market

Powertrain transition changes functional requirements. BEV architectures shift NVH priorities (e.g., battery pack and structural acoustics vs. traditional engine vibrational masking) and are already spawning new product categories such as specialized battery lids and multifunctional acoustic-thermal components.

NVH (System, Parts, Materials) Market

Raw material dynamics materially affect margins. For major NVH suppliers, polymers and synthetic rubbers represent the dominant share of cost of sales. Volatility in upstream petrochemical feedstocks therefore transmits directly to supplier margin profiles unless mitigated by material substitution, hedging, or process innovation.

Supply‑chain and labor dynamics remain local differentiators. Production expansions to capture BEV and aftermarket demand create hiring and localization pressures requiring careful plant footprint and automation planning.

Robust macro & scenario forecasts — a transparent base (2020–2025) and a scenario‑based view to 2032 (2026–2032), with sensitivity matrices that quantify exposure to key input variables such as petrochemical price swings, electrification adoption rates, and regulatory tightening.

Supplier playbooks — detailed strategic profiles and operational scorecards for leading Tier‑1 and specialist NVH players (capability maps, technology roadmaps, cost structure diagnostics, and go‑to‑customer posture). These enable benchmarking and quick identification of partners or targets.

Material and cost modelling — bottom‑up cost‑builds for major NVH components, unit economics for alternative material sets (including bio‑ and mineral‑filled polymers), and break‑even analyses under raw material price scenarios.

Regulatory impact matrix — actionable compliance timelines and technology levers to align product and validation plans with evolving noise and material standards in core markets.

Commercial and M&A playbooks — target screening criteria, valuation sensitivity to material constraints, and integration heat maps designed for acquirers and investors seeking consolidation or capability buys in a fragmented market.

Operational modules — plant footprint optimization, sourcing strategies, and CapEx prioritization templates tuned for a 24–36 month decision window.

Vibracoustic SE (Weinheim, Germany) — Recognized as a global NVH specialist, Vibracoustic’s product suite spans powertrain mounts, suspension and chassis mounts, isolators, and aftermarket solutions. Their near‑term strategic actions — including a global business transformation program with a major systems integrator to roll out SAP and digitize core processes — signal a priority on operational scale, margin recovery, and tighter supply chain control. For partners and competitors this means faster order‑to‑cash cycles, improved cost visibility, and an increased likelihood of data‑driven supplier consolidation.

Autoneum Holding Ltd. (Winterthur, Switzerland) — A leading actor in multifunctional acoustic and thermal management, Autoneum continues to push product innovation aligned to BEV needs. A recent product introduction targeted at battery enclosure acoustic performance highlights the pivot toward integrated NVH solutions for electrified platforms. OEMs and battery system suppliers should interpret such moves as an opportunity to co‑engineer early and to embed acoustic solutions into vehicle architecture rather than retrofitting them.

Applied Acoustics International (North America) — As a Tier‑1 specialist in noise and vibration engineering, Applied Acoustics is illustrative of high‑margin engineering plays that add product differentiation without necessarily commanding large manufacturing footprints. Strategic alliances between engineering‑heavy specialists and larger manufacturers will remain a common route to accelerate NVH innovation.

NVH Korea Inc. (Ulsan, South Korea) — A vertically integrated manufacturer covering interior, exterior and engine NVH systems, NVH Korea’s production expansion and job creation activities exemplify the labor and manufacturing dynamics in growth markets. Local capacity investments by regional suppliers can materially shorten lead times and provide OEMs with localization levers for cost and tariff management.

Regulation as a market driver — Tighter noise limits in major regulatory regimes are accelerating demand for higher‑performance materials and multifunctional components. Compliance timelines mean procurement and design teams must prioritize NVH early in the vehicle development cycle.

Material cost concentration — Major NVH suppliers report materials accounting for a very large share of cost of sales. This concentration makes material sourcing and alternative chemistries an essential element of margin management.

Feedstock volatility — Petroleum‑derivative price swings will continue to transmit to NVH product costs. Hedging policies, multi‑sourcing strategies, and R&D into low‑dependency materials are immediate risk mitigants.

Talent and capacity — Investments that increase capacity typically carry labor and ramp risks; scenario planning should incorporate time‑to‑ramp and automation choices tied to product complexity.

For OEMs: institutionalize NVH as an early architecture discipline. Design specifications and supplier selection must be locked into the concept phase to avoid costly rework and costly late‑stage acoustic fixes.

For Tier‑1 suppliers: prioritize modular multifunctional components that address both acoustic and thermal needs for BEV battery packs and e‑drive enclosures. Accelerate digitization of procurement and manufacturing planning to capture benefit from reduced working capital and improved scheduling accuracy.

For investors: screen targets against material risk exposure and IP strength in emerging BEV NVH products. Expect valuation premiums for companies that can demonstrate lower material intensity or validated alternative chemistries.

For procurement teams: run cost‑to‑serve and price‑pass through simulations under multiple petrochemical price scenarios. Implement rolling 12–24 month hedges where economically justified and negotiate clauses that balance risk between OEMs and strategic suppliers.

For R&D and product teams: invest in test capability for BEV‑specific NVH cases and build a rapid validation pipeline for new polymer blends and manufacturing techniques (e.g., foaming, hybrid laminates).

Deploy the report’s scenario dashboards to quantify upside and downside from shifts in BEV penetration, regulatory timelines, and petrochemical feedstock prices. Use these to stress test pricing, margin, and CapEx plans over an 18–36 month horizon.

Leverage supplier scorecards and capability maps to prioritize partnership pilots. Short‑list partners using a three‑axis rubric: technical fit, cost exposure, and geographic footprint resilience.

Apply the report’s cost models to build internal cost‑to‑deliver templates and commercial negotiation playbooks that can be updated quarterly as raw material data evolve.

This article has highlighted the structural drivers and strategic levers that make 2026 a critical year for NVH decision‑making. PW Consulting’s full NVH (System, Parts, Materials) Market Study contains the granular regional and application splits, segmented price curves, plant‑level cost models, supplier scorecards, and downloadable scenario templates that operational teams require to move from insight to execution. We have intentionally presented a high‑confidence strategic synopsis here while withholding the detailed segmentation and proprietary datasets that materially alter execution choices — access to the full dataset and executable toolkits will enable teams to prioritize investments, negotiate from strength, and lock in resilient sourcing strategies for the coming cycle.

For executives and functional leaders preparing 2026 budgets and 3‑year strategic plans, this research provides the required mix of market foresight and practical tools to convert NVH trends into competitive advantage.

For detailed analysis of this topic, please visit the official page:NVH (System, Parts, Materials) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com