Wireline Services Market 2026: Strategic Imperatives from PW Consulting’s Market Preview

As oil and gas operators and service providers plan budgets, partnerships and technology roadmaps for 2026, the wireline services market is emerging from a multi-year recovery into a structurally different competitive landscape. Our latest PW Consulting Wireline Services Market preview synthesizes market sizing, competitive dynamics, supply-chain constraints and operational levers to help executives make targeted, risk-aware decisions. This article outlines the strategic value of that research for 2026 planning—demonstrating the depth of our analysis while reserving detailed segment-level tables and proprietary scenario outputs for the full report.

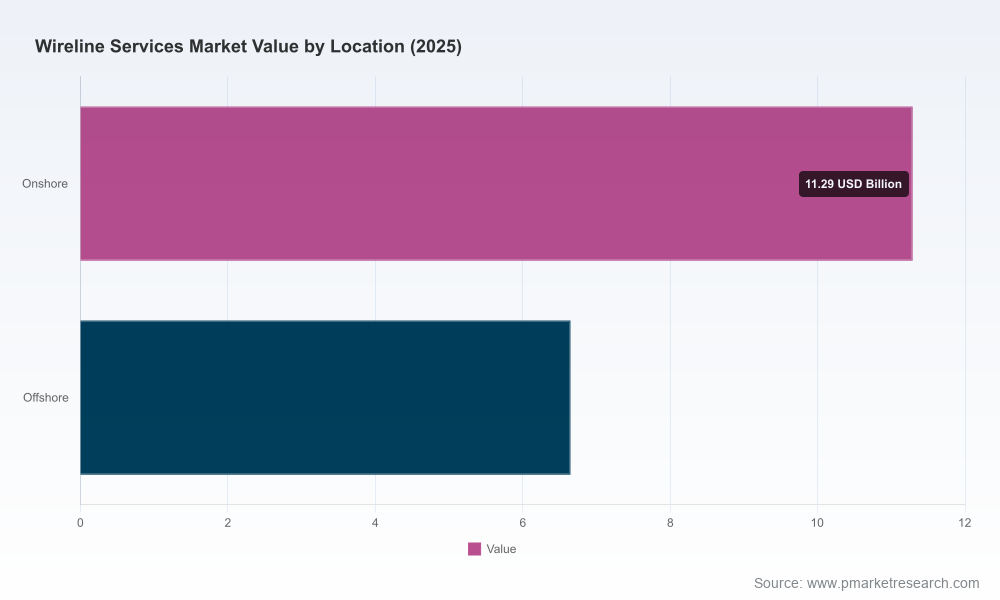

Wireline Services Market

Macro picture: growth, scale and concentration

At a macro level, the wireline services market has moved from recovery to measured expansion. Global market revenue increased from approximately USD 10.8 Billion in 2020 to USD 17.9 Billion in 2025, and our baseline forecast projects a continuation of that trajectory to roughly USD 28.8 Billion by 2032. That profile corresponds to a compound annual growth rate (CAGR) of about 7.0% over the forecast window. Two structural features matter for 2026 decision-making:

Wireline Services Market

- Market scale is sufficient to support large integrated service providers and specialized niche players simultaneously; investment decisions must therefore balance scale advantages against opportunities unlocked by specialization and faster technology adoption.

- Market concentration is material: the top three global players control a majority share, and the top five capture an even larger portion. This concentration shapes commercial dynamics—pricing, bundled offers, and contract design—and creates both entry barriers and acquisition targets for scale-seeking challengers.

Why this market intelligence changes 2026 decisions

Executives face five practical choices where precise wireline market intelligence materially alters outcomes in 2026:

Wireline Services Market

- Contracting strategy: whether to pursue integrated, long-term contracts with a global major or adopt a modular supplier strategy with specialized players affects cost trajectories, risk allocation and operational flexibility.

- CapEx vs OpEx trade-offs: equipment ownership, platform upgrades and digitalization investments demand a long-horizon cash-flow view; accurate market growth and utilization assumptions change the NPV of buy-versus-rent decisions.

- Technology adoption pacing: the pace at which operators and service companies adopt advanced downhole sensors, real-time telemetry and predictive maintenance tools determines differentiation—and the size of the addressable market for higher-margin services.

- M&A and partnership plays: a concentrated market produces strategic M&A opportunities for both buyers and sellers; precise sizing and scenario outputs are essential to value targets and integration plans.

- Talent and supply-chain resilience: skilled wireline technicians command premium compensation in mature fields, and specialized cable and tool supply is vulnerable to raw-material swings—both require proactive workforce and procurement strategies.

What the PW Consulting report delivers for 2026 planning

The full PW Consulting Wireline Services Market report is structured to move decision-makers from hypothesis to executable actions. Its operational focus is designed for commercial, technical and corporate development leaders who need both macro context and transaction-ready detail. Key deliverables include:

- Market sizing and scenario forecasts to 2032, with base, upside and downside cases that reflect commodity-linked capex cycles, offshore development timelines and technology adoption curves.

- Service-level economics—standardized unit costs, utilization benchmarks and margin sensitivities—enabling comparisons of own-vs-contracted service delivery models.

- Practical procurement playbooks for structuring integrated versus modular contracts, including risk allocation templates, indexation clauses and performance KPIs designed for wireline operations.

- Supplier benchmarking and capability matrices that map technical competencies (e.g., cased-hole vs open-hole logging, electric line vs slickline interventions) to commercial models and fleet readiness.

- Supply-chain stress tests focused on specialized components (electrical downhole cables, telemetry modules) and labor scenarios to quantify delivery risk and cost volatility under different market shocks.

- M&A and partnership decision frameworks—valuation priors, integration checklists and synergy playbooks—tailored for both regional consolidators and global majors pursuing capability fills.

Competitive dynamics: what the market leaders are doing

The competitive map in 2026 reflects a blend of contract-driven expansion, capability bundling and technology-led differentiation. The major global service providers continue to leverage broad portfolios and integrated project capabilities, while regional and specialized players focus on operational agility and niche technical services.

- Baker Hughes (Houston, Texas) remains a front-line competitor, leveraging integrated well-construction contracts and expanding wireline scope across complex offshore basins. Recent contract extensions with Petrobras and Equinor underscore a strategy that couples wireline capabilities with broader drilling and intervention packages—an approach that increases contract stickiness and average revenue per well.

- SLB (Houston, Texas) continues to pursue multi-asset, multi-region offers that bundle wireline, completions and drilling services. Recent awards for deepwater gas developments illustrate how participation in upstream project workstreams can secure multi-year wireline demand ahead of first gas milestones.

- Halliburton (Houston, Texas) positions wireline interventions within its completions and plugging suites, focusing on integrated offshore execution and lifecycle well integrity services—areas where combined expertise creates margin uplift.

- Weatherford International (Houston, Texas) and other specialist players emphasize operational efficiency and targeted product innovations (slickline/e-line toolsets), competing on speed-to-deploy and cost-per-intervention metrics.

- Regional specialists such as Expro (Aberdeen) and China Oilfield Services Limited (Beijing) balance global standards with local execution advantages, particularly in offshore and onshore basins with distinct regulatory or logistics profiles.

- Smaller entrants and niche providers (e.g., Archer Limited, Superior Energy Services) continue to capture pockets of demand where responsiveness and bespoke technical capabilities trump scale.

These competitive moves are amplified by recent contract flows in early 2026—multi-year awards and extensions that lock-in wireline scopes as part of larger well-construction and intervention packages. The practical implication for executives: contracting windows are active and those who can demonstrate integrated capability or disciplined procurement timing will secure preferential access and pricing.

Operational levers and risk factors to watch in 2026

Several operational and market risks will determine which players and strategies outperform in 2026:

- Commodity-linked capex: upstream investment cadence continues to set the volume and timing of wireline demand. Our scenario outputs quantify how a modest shift in upstream capex can ripple through utilization and day-rate dynamics.

- Raw-material and supply-chain volatility: specialized electrical cables and downhole tool components are exposed to commodity-price cycles. Procurement strategies should incorporate hedges, dual-sourcing and safety-stock policies tailored to high-value components.

- Labor and skills: the premium for experienced wireline engineers in mature and complex fields is a structural cost driver. Workforce programs—training, retention incentives and remote-operations augmentation—are essential for consistent uptime and safety performance.

- Regulatory and contractual complexity: region-specific contracting norms and evolving safety and emissions rules influence scope definition and risk allocation. Contract templates in the report reflect clauses to mitigate these jurisdictional uncertainties.

- Technology adoption and data monetization: operators that demand telemetry, real-time analytics and integrated logging/completion datasets will shift service mix toward higher-margin, data-enabled services. This creates new value-capture opportunities for suppliers who can package tools with analytics and outcome-based guarantees.

Actionable recommendations for 2026

Based on the interplay of growth forecasts, competitive concentration and operational risks, senior leaders should prioritize three actions in 2026 planning cycles:

- Define a contracting posture aligned to portfolio risk: for core, high-complexity assets pursue integrated multi-year partnerships with performance-based milestones; for brownfield or episodic needs, maintain a modular supplier set to capture agility and cost competition.

- Accelerate investments in digital-enabled services where ROI can be demonstrated within two-to-three years—predictive maintenance for downhole tools, real-time logging analytics and remote intervention orchestration are high-impact areas.

- Harden supply-chain resiliency: build inventory strategies for critical cable/tool components, qualify secondary suppliers, and invest in workforce pipelines to mitigate wage inflation and skill shortages.

Why PW Consulting’s full report is the right next step

This article previews the strategic contours that will shape wireline decisions in 2026. Our full report augments these insights with the granular data and decision frameworks that procurement directors, asset teams and corporate development leaders require: segmented demand models, supplier scorecards, contract language playbooks, and deal valuation templates. We intentionally withhold proprietary segment-level tables and the detailed regional/application breakouts here to preserve the actionable advantage contained in the full deliverable.

For teams preparing 2026 budgets, negotiating framework agreements or sizing acquisition targets, the combination of our top-line forecasts (historical and projected market size through 2032), concentration metrics and operational playbooks converts sector-level conviction into executable programs. To access the complete dataset, modeling workbooks and procurement templates, please refer to PW Consulting’s Wireline Services Market report on our website or contact our industry desk for an executive briefing.

In a market where a handful of major players steer contract flows and where technology and supply-chain constraints create asymmetric advantages, timely, structured intelligence is the difference between reactive procurement and strategic value capture. PW Consulting’s analysis equips you to choose—confidently—where to defend, where to disrupt, and where to partner in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Wireline Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com