Radiosurgery Systems (Neurology Devices) Market Size, Share, Diagnostics Trends, and Forecast by 2032

Other |

2026-06-29 11:03:26

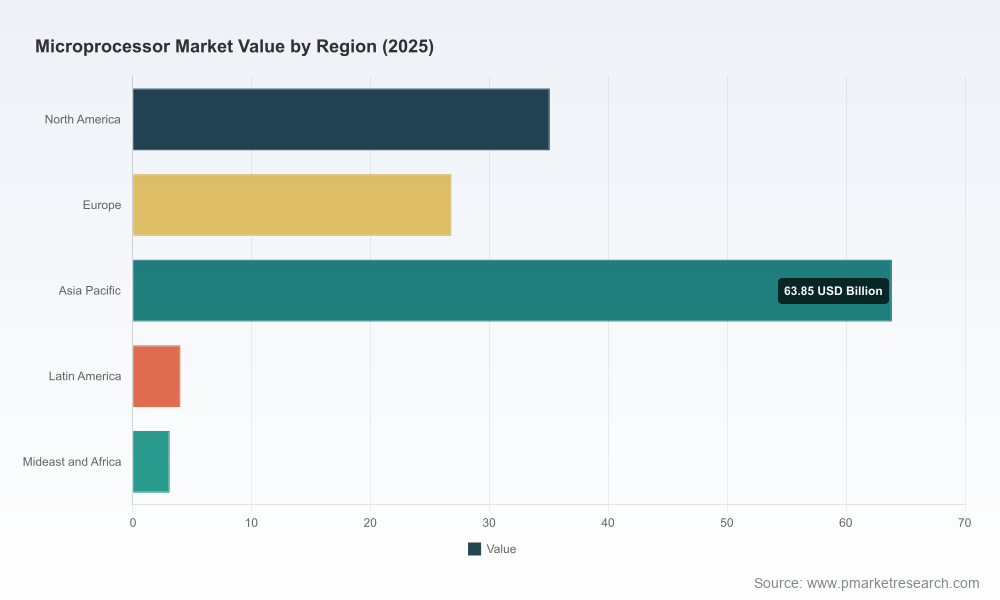

PW Consulting’s latest Microprocessor Market study (base year 2025; historical window 2020–2025; forecast 2026–2032) reframes how executive teams should approach product, supply chain and M&A decisions in 2026. At a macro level the market has expanded from roughly USD 108 billion in 2020 to about USD 133 billion in 2025, and is forecast to reach nearly USD 195 billion by 2032 at a compound annual growth rate of 5.56%. These headline figures reflect a market that is large, steadily growing, and increasingly shaped by a concentrated set of technology, supply and geopolitical vectors that will determine winners and losers in the coming 18–36 months.

Microprocessor Market

Immediate prioritization: 2026 is the first full strategic planning year after several disruptive policy and supply events (export controls, tariffs, and memory-price shocks). The report translates those shocks into prioritized actions for procurement, inventory, capacity and R&D spend.

Microprocessor Market

De-risking investment: Capital allocation decisions — from fabs to design teams to software ecosystems — require probabilistic scenario planning. Our models convert macro forecasts into scenario-specific ROI ranges and break-even timelines so CFOs can choose among competing investments with quantifiable trade-offs.

Microprocessor Market

Competitive positioning: With significant market concentration among the top OEMs and platform providers, the research shows where horizontal partnerships, vertical integration and differentiated IP deliver the most durable advantage.

Regulatory readiness: New controls and tariff regimes introduced in late 2025 and early 2026 materially alter addressable markets and channel economics. The report maps policy levers to commercial outcomes and prescribes mitigation measures for exporters, integrators and end-device manufacturers.

Transparent market-sizing and forecasting methodology tied to publicly verifiable inputs and PW Consulting’s proprietary demand drivers model (CPU cycles per device, AI-acceleration attach rates, automotive compute per vehicle, etc.).

Scenario suites (three base-case/three stress-case) that embed geopolitical shocks, supply shortages and accelerated AI adoption; each scenario includes P&L, cash-flow and working-capital implications for typical microprocessor-centric business models.

Go-to-market playbooks by buyer persona: hyperscalers, OEMs (mobile, PC, automotive), Tier-1 integrators and industrial customers. Each playbook translates technical differentiation into procurement, pricing and partnerships tactics.

Supply-chain heatmaps and supplier-dependence indices that combine material, fab, substrate and logistics risk into a single actionable score per supplier cluster.

M&A and alliance decision frameworks with valuation corridors for tuck-ins, capability acquisitions and joint ventures — calibrated to current market multiples and projected synergy capture.

Commercial templates: procurement RFx checklists, strategic supplier-scorecard templates, and go‑to‑market KPIs that can be operationalized in 90–120 days.

AI and accelerator-led demand: The ongoing proliferation of AI workloads — in data centers and increasingly at the edge — drives higher performance and heterogeneous compute requirements. This lifts demand not only for CPUs but for integrated SoCs and accelerator pairings.

Memory and component inflation: Memory price volatility observed in late 2025 created immediate cost pressure across system builders and has materially shortened procurement planning horizons. Organizations must now model multi-quarter price shock scenarios into BOM and margin planning.

Geopolitical and trade constraints: New export controls and tariff measures enacted in early 2026, and earlier export restrictions announced in 2025, have changed supply assurances and market access. These policy shifts produce uneven regional demand reinterpretations and higher costs of compliance.

Concentration and platform effects: A small group of firms account for the majority of industry revenue and ecosystem influence. This concentration amplifies platform lock-in risks but also creates clear targets for strategic partnerships or competitive disruption.

Intel Corporation: Continues to lead in x86 desktop and laptop microprocessors and is investing to maintain process-node and architecture advantages. Recognition in early 2026 underscores ongoing capability leadership, but Intel’s strategic bets focus on extending relevance across cloud and AI workloads.

Advanced Micro Devices (AMD): Competes aggressively on performance-per-watt and server designs, leveraging integrated CPU/GPU approaches. AMD remains a critical alternative for buyers seeking x86 performance with differentiated power characteristics.

NVIDIA: While primarily a GPU and accelerator vendor, NVIDIA’s ecosystem is reshaping compute stacks. Their accelerators are frequently paired with microprocessors in data center and edge AI applications — creating a new layer of dependency and co-innovation opportunity for CPU vendors.

Qualcomm: Strong in mobile and expanding into automotive and edge compute via Snapdragon SoCs and custom AI processors. Its integrator relationships with OEMs make it a strategic partner for brands moving compute toward the device.

Broadcom: Plays a critical role in networking and custom acceleration for data center systems. Its offerings are influential in how server and communications platforms are architected.

Apple and Samsung: Both drive differentiated, vertically integrated silicon for consumer ecosystems. Their designs push the boundaries of power and system-level optimization and force rivals to respond across hardware and software stacks.

NXP, STMicroelectronics, TI, Analog Devices, Microchip: These firms anchor the embedded, automotive and industrial sides of the market. Recent product launches and roadmaps emphasize cost-sensitive, secure edge compute and real-time processing for industrial and mobility applications.

Two recent developments are emblematic of competitive dynamics in 2026: a major microprocessor family launch targeted at cost‑sensitive edge applications (early 2026), and renewed external recognition of incumbents’ technological leadership (spring 2026). Both underscore the dual market pressure to push performance while controlling bill-of-materials and certification timelines for regulated industries.

Export controls and tariffs: New rules and tariffs introduced in early 2026 have immediate implications for channel economics and where certain classes of chips can be shipped without authorization. Companies must build a compliance-first commercial posture that integrates license risk into revenue planning.

Materials and component availability: Export restrictions on certain materials and a pronounced spike in memory pricing during late 2025 require firms to rethink sourcing strategies. The prudent course is a blended approach: strategic stock, qualified second sources and pricing clauses that share risk with customers.

Long-term scarcity scenarios: For specific component families, shortages could persist for multiple years. The report offers threshold-based trigger points for capacity expansion and contractual protections to mitigate extended shortages.

Supplier de‑risking playbook: A step-by-step sequence to map single-source exposures, qualify alternate suppliers, and implement dual-sourcing contracts with staged volume commitments.

Product roadmap triage: A matrix to rank product features and variants by margin contribution, customer retention impact and regulatory cost — enabling product managers to defer non‑strategic features and prioritize high-value compute integrations.

Pricing and procurement hedges: Short-term financial instruments and procurement clauses that tie pricing to transparent indices, coupled with operational levers (software-enabled efficiency) to protect gross margins.

M&A readiness checklist: Financial and technical due diligence templates tailored for microprocessor and accelerator targets, including IP quality, supply-chain integration risk and customer overlap analysis.

To preserve the commercial integrity of our primary research and to encourage informed engagement, this introduction omits the full granular breakdowns by region, processor-type and application verticals. The full report contains detailed regional and application splits, unit economics, pricing curves and supplier-level revenue shares — all essential for transaction diligence and tactical planning. If you require the specific segment-level tables, forecast matrices and the proprietary demand model used in our scenarios, they are available in the complete PW Consulting Microprocessor Market report.

2026 will be the year organizations convert short-term disruption into durable advantage. Our study equips leaders with the macro perspective (large, mid-single-digit CAGR growth at the market level), granular scenario tools, and executable playbooks to make decisions with confidence: where to invest, what partnerships to form, which supply risks to hedge, and which product bets to accelerate. The market’s size and growth matter — but the distribution of that growth across platforms, geographies and applications will determine returns. PW Consulting’s analysis shortens your decision cycle and increases the probability that 2026 investments compound into sustained competitive advantage.

Access the full report to obtain the proprietary segment tables, supplier-level assessments and scenario models required for detailed planning and deal execution.

For detailed analysis of this topic, please visit the official page:Microprocessor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com