Transparent Barrier Films Market: Strategic Imperatives for 2026

Introduction — why this briefing matters now

As regulatory clocks, sustainability targets and consumer expectations accelerate, transparent barrier films are moving from a niche technical choice to a strategic lever across the packaging value chain. PW Consulting’s latest market study (base year 2025; forecast 2026–2032) synthesizes market sizing, technology trajectories and regulatory disruption into an actionable roadmap for corporate leaders making capital allocation, sourcing and product strategy decisions in 2026.

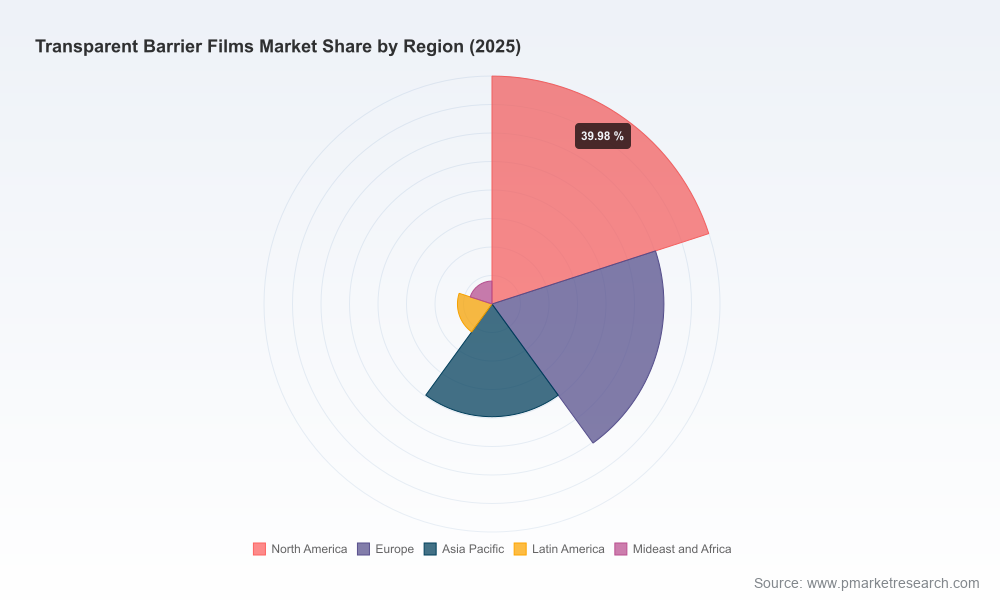

Transparent Barrier Films Market

At a macro level, the market has demonstrated steady expansion — growing from approximately USD 2,250 Million in 2020 to just over USD 3,037 Million in 2025 — and our modelling points to continued expansion through the forecast window, reaching roughly USD 4,682 Million by 2032 on a compound annual growth rate of 6.4%. These headline dynamics frame the strategic stakes: incremental growth is available, but value capture will depend on anticipating regulation, securing differentiated technology and managing input-cost volatility.

Transparent Barrier Films Market

What the full report delivers — practical, transaction-ready intelligence

- Executive synthesis of market drivers, inflection points and three commercial scenarios (base, accelerated adoption, and regulatory-driven substitution) calibrated to macro and micro inputs.

- Robust quantitative models: historic time series (2020–2025), bottom-up sizing logic for 2026–2032, and an integrated financial model for scenario testing (licensable Excel workbook).

- Competitive landscape and capability maps: technology trees (AlOx, ALOx PET, PVDC, EVOH co-extrusion, vapour-deposition coatings), manufacturing footprints, capacity dynamics and an M&A readiness checklist.

- Regulatory impact assessment and compliance playbooks, focused on actions required to meet near-term EU obligations and shifting Extended Producer Responsibility (EPR) mechanics.

- Supply-chain stress tests and procurement playbook: raw material sensitivity analysis, supplier concentration risk, alternative sourcing strategies and negotiation levers for long-term offtake.

- Go-to-market templates for film producers and converters: product positioning, piloting protocols with brand owners, recyclability claims substantiation, and commercial clauses for price-pass-through and sustainability warranties.

- Deal support assets: vendor due diligence checklists, integration scorecards, and value-creation pipelines for greenfield expansions or bolt-on acquisitions.

Market dynamics and inflection points that will shape 2026 decisions

Three systemic forces are converging and will determine who wins or loses in the next 24 months:

Transparent Barrier Films Market

- Regulatory acceleration toward recyclable, mono-material packaging. The EU Packaging and Packaging Waste Regulation (PPWR) entered into force in February 2025 and becomes binding in August 2026; it harmonizes EPR frameworks and brings concrete design-for-recycling obligations. It also formalizes minimum recycled content thresholds on specific formats, raising the bar for incumbent structures and accelerating demand for transparent barrier technologies that enable mono-material formats.

- Materials and cost volatility. Price movement in barrier polymers and specialty resins is a real operational lever. Reported EVOH price indices in Q1 2026 indicated a mid-to-high single-thousand USD per metric-ton range across geographies (in our analysis, typical market values clustered in the ~USD 7,000–7,800/MT band), implying that delta-costs for high-barrier solutions are meaningful and must be managed through procurement hedges, formulation optimization or long-term supply agreements.

- Consolidation and capability concentration. The film market shows notable concentration among leading technology providers. The top three players account for a substantial share of industry revenue, and the top five exhibit even higher combined concentration — an important consideration for buyers seeking scale, technical support and warranties for food- or pharma-grade solutions.

Competitive landscape — technology plays and strategic positioning

The competitive set is diverse in technology and go-to-market models. Key strategic archetypes we track include high-tech coating specialists, large-scale film extruders with coating capability, and nimble regional players focused on cost or recyclability claims. Representative players include firms such as TOPPAN, Dai Nippon Printing, Polyplex, BIO Packaging Films, CloudFilm, Momar Industries, Eurocast, Cosmo Films and Jindal Films. Each brings a different mix of proprietary coating (vapour-deposition, AlOx), co-extrusion (EVOH, PVDC) and commercial scale.

Recent corporate moves illustrate the strategic priorities manufacturers are pursuing:

- Product innovation to displace aluminum and multi-material laminates: leading suppliers have introduced mono-material retort-capable barrier films that deliver ambient shelf life while enabling aluminum-free pouch designs — a critical enabler for brand owners responding to recyclability mandates.

- Capacity investments oriented to recyclable mono-structures: producers have announced expansions of EVOH-based production capacity to serve the growing demand for co-extruded barrier layers compatible with mono-polymer recycling streams.

- Value-chain collaboration: suppliers are increasingly entering co-development and retrofit agreements with converters and brands to validate recycling streams and secure long-term offtakes.

Strategic implications for 2026 corporate decisions

For 2026 action plans, our report highlights five priority moves by player type:

- Brand owners and retailers: accelerate portfolio triage. Establish a cross-functional “recyclability fast track” that prioritizes SKUs for pilot substitution with transparent barrier films. Quantify cost-to-serve impacts and consumer-facing claims early so procurement can lock-in supply at favorable terms.

- Film producers and converters: invest selectively in mono-material barrier platforms and validation labs. Pursue modular capacity expansions and de-risk feedstock via dual-sourcing or polymer-supply partnerships.

- Investors and M&A teams: prioritize targets with demonstrable technology differentiation (coating IP or EVOH co-extrusion competence), validated commercial partnerships with FMCG brands, and flexible production footprints that can be repurposed to meet stricter recyclability standards.

- Procurement and operations: introduce material-cost hedging triggers and contract clauses for extreme volatility. Implement an input-cost monitoring dashboard tied to weekly polymer indices and supplier capacity-utilization metrics.

- Regulatory/compliance teams: create an EU PPWR readiness timeline through 2026, including product labelling updates, documentation requirements for EPR fees, and product re-design milestones tied to recycled content obligations.

How PW Consulting’s study informs the above decisions

Our report translates the market trajectory and regulatory milestones into commercial KPIs and go/no-go decision gates. Examples of deliverables that clients have found immediately useful include:

- Scenario P&L impact tables that quantify margin erosion or uplift under various substitution and recycled-content pathways.

- Supply continuity risk maps that rank suppliers by technological uniqueness, gigawatt-equivalent capacity and geographic exposure to regulatory risk.

- Negotiation playbooks for passing incremental barrier film costs through to customers while preserving shelf-life and consumer perception.

- Implementation blueprints for converter–brand pilots (design of experiment templates, acceptance criteria, and lab validation checklists) to compress commercialization timelines from months to weeks.

Limitations and where the full report fills the gaps

This introductory analysis highlights the structural drivers and strategic options; the full PW Consulting study contains the detailed, segment-level intelligence required for transactional execution: granular historic and forecast demand by type, application and region; supplier-by-supplier capacity maps; price-buildups; and downloadable financial models. These items are intentionally withheld in this preview to protect the value of proprietary modelling and to ensure clients can access validated, auditable data in full context.

Next steps — recommended immediate moves for 2026

- Initiate a 90-day cross-functional sprint to pilot mono-material barrier replacement on a controlled set of SKUs and to secure binding supply options for EVOH or Alox-coated films.

- Commission a targeted due diligence on at least two technology partners to assess IP defensibility and scaling risks over a 24-month horizon.

- Adopt a regulatory readiness calendar aligned to PPWR milestones and embed recyclability KPIs into supplier scorecards and EPR budgeting.

Conclusion — why now is a decisive window

Transparent barrier films are no longer a peripheral packaging choice; they are central to how brand owners, converters and film manufacturers meet the twin demands of sustainability and shelf-life performance. With the market already expanding and regulation setting firm timelines, 2026 is a decisive year to convert strategy into binding commercial moves. PW Consulting’s full study provides the granular models, benchmarked supplier intelligence and implementation playbooks to de-risk those decisions and accelerate value capture.

To access the complete dataset, downloadable models and step-by-step implementation guides, please visit our report page or contact PW Consulting’s Transparent Barrier Films practice for a confidential briefing.

For detailed analysis of this topic, please visit the official page:Transparent Barrier Films Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com