Fractional RF Microneedling in Dubai for Large Pores

Other |

2026-04-13 10:16:21

As transit agencies, system integrators, and investors recalibrate for a post‑pandemic mobility landscape, the Automatic Fare Collection (AFC) systems market is entering a phase of rapid commercialisation and technological consolidation. PW Consulting’s new AFC market study — anchored on a 2025 base year and a 2026–2032 forecast horizon — provides the forward-looking, decision‑grade intelligence leaders need to convert market momentum into defensible strategy in 2026.

Automatic Fare Collection (AFC) Systems Market

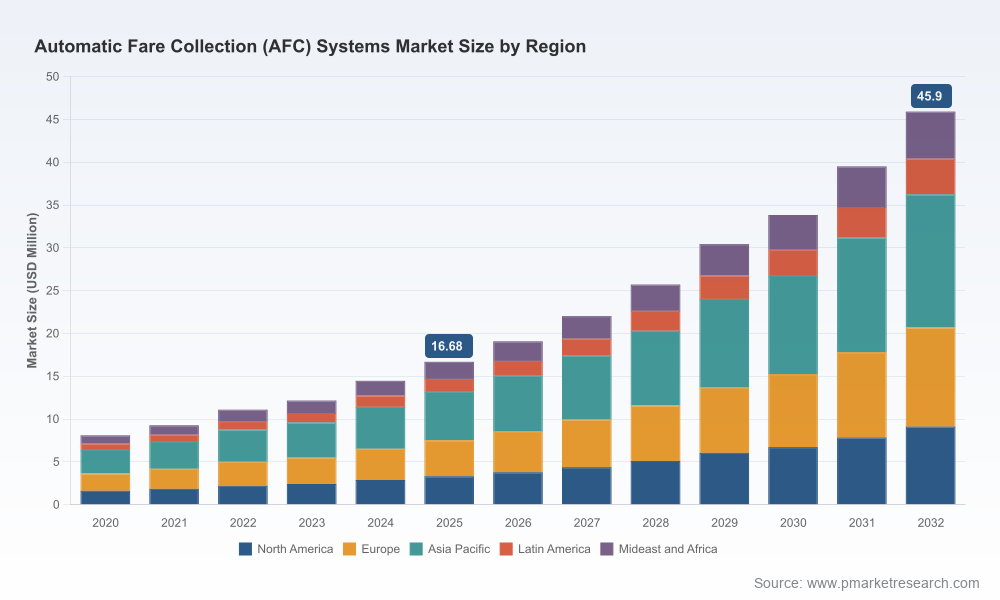

The AFC market has recorded sustained growth through the first half of the decade, expanding from a modest industry base in 2020 to a materially larger market by 2025. Our topline projection shows continued acceleration into the forecast period: the market is expected to grow at a compound annual growth rate (CAGR) of 15.56% across 2026–2032, reaching a materially larger market size by 2032 compared with 2025. Year‑on‑year projections for the immediate term reflect persistent investment into fare modernization, contactless payments and account‑based ticketing initiatives.

Automatic Fare Collection (AFC) Systems Market

These aggregate figures are deliberately included here to frame the opportunity scale for executives planning procurement, product investment, or M&A activity in 2026. The full report contains the granular time‑series tables and scenario runs underpinning these topline projections.

Automatic Fare Collection (AFC) Systems Market

Procurement readiness: Public authorities preparing RFPs or contract renewals need evidence‑based benchmarks for pricing, implementation timelines and risk allocation; our study translates topline growth into practical procurement guardrails.

Vendor strategy: Vendors should prioritize where to invest R&D, identify partnership targets, and size go‑to‑market opportunities. The report maps competitive positioning against expected market demand and regulatory constraints.

Investor and M&A plays: With the market showing concentrated vendor power at the top, our analysis identifies consolidation vectors and the financially attractive niches where bolt‑on acquisitions can accelerate product roadmaps.

Operational transition planning: Transit operators can use our implementation playbooks to stage migrations to account‑based, contactless, or mobile fare modalities while preserving service continuity.

Market architecture and demand scenarios: layered demand modelling that distinguishes short‑term tender pipelines from multi‑year adoption curves and stress‑tested forecasts under alternate economic and policy scenarios.

Vendor benchmarking and capability matrices: comparable scorecards across technical scope (validators, back‑office, account‑based platforms), commercial models (CAPEX vs. OPEX, SaaS, Fare Payments‑as‑a‑Service) and operational performance metrics.

Procurement playbooks and contract templates: modular scopes of work, performance acceptance criteria, staged payment structures, and hold‑back/penalty mechanics tuned to preserve service continuity during cutover.

Implementation checklists and risk registers: vetted test plans (including mass transit certification requirements), migration sequencing, pilot design, and contingency plans to keep systems operational during rollouts.

Regulatory and compliance toolkit: prescriptive guidance on FTA‑type certification pathways, Buy America considerations, and documentation templates that accelerate pre‑award compliance reviews.

Supply‑chain and materials analysis: component‑level sourcing risk for specialized electronics (logic boards, sensors, magnetic readers/encoders, contactless validators), options for dual sourcing, and lead‑time mitigation strategies.

Commercial models and TCO scenarios: side‑by‑side CAPEX/OPEX and TCO dashboards that capture hardware refresh cycles, software-as-a-service fees, revenue-management uplift, and lifecycle maintenance costs.

The AFC vendor landscape is characterised by a mix of established systems integrators, global defence and transportation technology players, and specialist software providers offering cloud‑native fare payments. Market concentration metrics indicate that the top three vendors command a majority of market share while the top five account for a very large portion of market capacity — a structure that favours strategic scale, distribution capability and public‑sector procurement track record.

Cubic Transportation Systems (United States) — a market incumbent with strengths in account‑based and open payment implementations and large transit program experience (notably modern, city‑scale rollouts). Recent contract activity underscores Cubic’s continued role in major urban programs and systems upgrades.

Thales Group (France) — leverages its broader transport and security portfolio to offer integrated mobile ticketing and gate solutions, with a particular emphasis on contactless ecosystem integration.

Scheidt & Bachmann (Germany) — established in fare collection hardware and validators, with an increasing focus on account‑based platforms and modernization projects for legacy fleets.

INIT and Conduent — both bring strong revenue‑management and back‑office capabilities; INIT focuses on ITS and contactless ticketing integration, while Conduent couples systems integration scale with public‑sector program delivery experience.

Masabi and other software‑first challengers — introduce fast‑to‑market Fare Payments‑as‑a‑Service models and mobile‑centric offerings that are changing procurement conversations around managed services and recurring revenue contracts.

Regional and systems specialists (Aurionpro, SC Soft, Vix Technology, Prodata Mobility) — often win on local presence, turnkey delivery and integration with existing ITS stacks; their role in regional rollouts is strategically important for partners and contractors.

Recent program activity is illustrative: early‑2026 contract awards and late‑2025 project progress events indicate ongoing modernization investments in major U.S. metros and regional systems — reinforcing vendor momentum but also amplifying procurement scrutiny over compliance and integration risk.

Regulatory certification and testing: some public funders now require final test reports conforming to formal test standards; programmes must plan for certification time and test‑report dependencies when sequencing rollout milestones.

Buy America and localisation requirements: many FTA‑funded projects mandate documentation around domestic content and final assembly. Pre‑award certification strategies and supplier mapping are critical to avoid disqualification or late compliance costs.

Operational continuity: procurement specifications increasingly demand that AFC implementations remain operational during installation to avoid service disruption — this raises the bar for parallel‑run strategies, data migration and fallbacks.

Hardware component dependencies: AFC hardware relies on specialised electronics and sensor modules that have constrained supplier pools; you should treat component sourcing as a strategic risk area and plan for obsolescence management.

Supply‑chain risk — mitigate with supplier‑diversification clauses, long‑lead procurement windows, and inventory buffering for critical electronic components.

Integration complexity — require interface standards and open APIs in contracts; insist on interoperability testing and vendor cooperation clauses for third‑party subsystems.

Regulatory non‑compliance — embed pre‑award compliance milestones and independent verification into procurement timelines to avoid late remediations.

Vendor lock‑in — prefer modular, service‑oriented contracts that allow phased vendor substitution and include data portability obligations.

Operational disruption — fund and design pilots that validate cutover procedures and data reconciliation under real service loads.

Prioritise pilots for account‑based and open payment models with measurable KPIs for ridership, payment success rates and revenue assurance.

Require Buy America and certification mapping as part of vendor pre‑qualification to avoid downstream surprises.

Negotiate modular contracts that separate hardware, software and operations to enable upgrade paths and commercial flexibility.

Insist on service continuity guarantees and detailed cutover plans for any live deployment to maintain ridership confidence.

Build TCO scenarios into vendor evaluations to assess long‑term cost of managed services versus capital purchases.

Track consolidation and partner ecosystems; consider strategic partnerships or acquisitions to acquire missing capabilities (e.g., account‑based back offices, mobile wallets, systems‑integration scale).

For executives finalising budgets, drafting RFPs, or evaluating investment theses in 2026, the AFC market presents both clear growth and concrete implementation risk. PW Consulting’s AFC market study synthesises quantitative growth forecasts, vendor‑level benchmarking, procurement playbooks and compliance toolkits into an operational roadmap for decision‑makers. This article provides a high‑level orientation; the full report contains the granular segment breakdowns, vendor scorecards, contract comparators and downloadable procurement templates that teams will need to execute with confidence.

To access the full dataset, including regional and application segment tables, vendor scorecards and scenario modelling assets, please consult the PW Consulting report landing page where the complete research package and implementation toolkits are available.

For detailed analysis of this topic, please visit the official page:Automatic Fare Collection (AFC) Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com