Hyperkalemia Treatment Market Evolution: Advancements in Chronic and Acute Hyperkalemia Treatment Approaches

Health |

2026-05-28 11:30:13

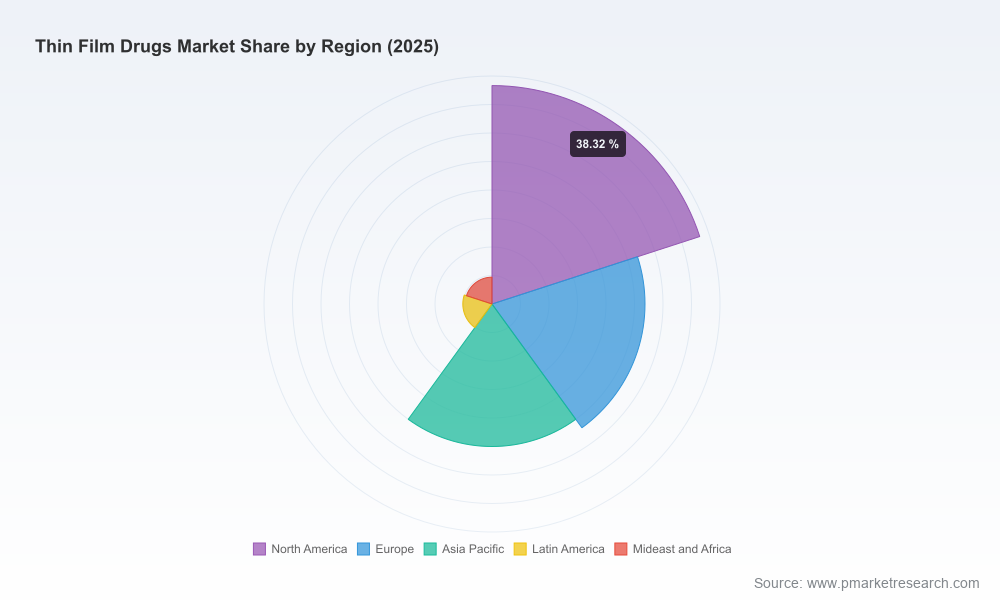

The thin film drugs market has moved from a promising niche to a strategically relevant therapeutic and delivery modality. Our analysis shows the market expanding from an estimated USD 3.15 billion in 2020 to USD 4.88 billion in 2025, and projecting to approximately USD 9.14 billion by 2032 — reflecting a compound annual growth rate of roughly 9.5% across the forecast period. That trajectory creates both enlarged addressable opportunities and heightened competitive pressure: incumbents and new entrants must convert technical advantages into scalable commercial outcomes, while payers and regulators update frameworks for these patient-centric modalities.

Thin Film Drugs Market

Base-year alignment: With 2025 established as the analytical base year, 2026 marks the first full operational year for strategies informed by the newest regulatory decisions, clinical readouts, and manufacturing investments. Many product roadmaps and license windows converge in this timeframe.

Thin Film Drugs Market

Commercial readiness: Advances in formulation platforms, CDMO capacity expansion, and the first wave of thin film approvals have matured supply-side capabilities to a point where scale-up risk is often the binding constraint — not clinical plausibility.

Thin Film Drugs Market

Competitive consolidation: Market concentration indicates that leading firms command a substantial share of market value. This dynamic increases the value of targeted partnerships, differentiation through IP or service models, and first-mover advantages in priority therapeutic areas.

Our report is built for executives making real 2026 decisions. Rather than a descriptive summary, it delivers tools, templates and decision-ready outputs you can apply immediately:

Proprietary market-sizing model (2020–2032) with transparent assumptions and scenario toggles — enabling bespoke “what-if” forecasts for product launches, geography prioritization, and pricing strategies.

Investment decision frameworks that translate technical readouts (bioavailability, manufacturability, stability) into go/no-go thresholds for R&D and capital allocation.

Go-to-market playbooks for thin film products: channel strategies, payer engagement templates, and product launch milestones tailored to both branded and generic strategies.

Manufacturing and CMC scorecards for vendor selection and in-house vs. outsourcing decisions, including capacity ramp timelines and quality risk matrices.

Regulatory pathway comparisons and a dossier-preparation checklist that anticipates typical questions regulator agencies raise for thin film formulations.

M&A and licensing target filters: a prioritized list of capability archetypes and negotiation playbooks designed to accelerate capability acquisition while managing valuation risk.

Company profiles and competitive heatmaps that highlight capabilities (platform technologies, FDA approvals, CDMO competencies) and identify tactical partnership fits.

Implementation timelines and 90/180/365-day action plans aligned to board-level decision cycles.

The competitive topology combines technology-specialists, specialty pharma, large multinationals and specialized CDMOs. Three-to-five firm concentration metrics indicate a market where a limited set of players owns meaningful share — making strategic positioning, alliances and IP management determinative.

IntelGenx Technologies Corp. (Saint-Laurent, Quebec) — purpose-built platform player. Their proprietary VersaFilm® technology and developer-manufacturer model make them an attractive partner for pharma companies seeking to externalize formulation innovation.

Indivior PLC (North Chesterfield, VA) — clinician-focused specialty pharma. Known for oral thin film products in dependency treatment, Indivior illustrates how therapeutic focus plus commercial expertise can secure strong payer and provider acceptance.

Pfizer Inc. (New York City) — scale and portfolio breadth. As a large-cap incumbent, Pfizer brings integration advantages across development, global regulatory reach and established commercialization channels — a reminder that platform utility must be reconcilable with large pharma requirements.

ZIM Laboratories Limited (Nagpur) — manufacturing-led innovator. Their emphasis on bilayer and innovative oral thin film platforms underscores the strategic value of upstream formulation know-how paired with cost-competitive production.

Novartis AG (Basel) and Sumitomo Pharma Co., Ltd. (Osaka) — diversified R&D and regional strengths. These firms demonstrate how thin film formats can be nested within broader therapeutic franchises to extend product lifecycle and improve patient adherence.

LTS Lohmann Therapie-Systeme AG and Vektor Pharma TF GmbH — CDMO and specialty manufacturers. They illustrate two paths to profitability: (1) capture of outsourced development and manufacturing demand; (2) co-development partnerships that reduce sponsor capital needs.

Aquestive Therapeutics, Inc. (Warren, NJ) — regulatory leadership in buccal films. Specialist approvals provide commercial proof points and help define acceptable clinical endpoints for regulators and payers alike.

Collectively, these profiles explain why strategic choices are as much about partner selection and IP negotiation as they are about the underlying science.

Patient-centric demand: Adherence and ease-of-use considerations continue to drive payer and prescriber interest, especially for chronic and acute-onset indications.

Manufacturing scale-up challenges: While lab-stage formulations are tractable, consistent quality at scale — including uniform drug loading and stability — remains a commercial gating item.

Regulatory evolution: Health authorities are refining expectations for bioequivalence and inhalation/sublingual safety, which affects trial design and data packages.

Value-based contracting: Payers increasingly request evidence of real-world adherence and economic benefit; product claims must be backed by datasets and go-to-payer strategies.

Consolidation pressure: With meaningful concentration at the top, strategic players will watch for bolt-on acquisitions and long-term supplier agreements that can reallocate margin pools.

Portfolio triage: Use our technical-commercial scorecard to prioritize candidates that balance clinical differentiation, manufacturing feasibility, and payer value proposition.

Manufacturing decisions: For companies without in-house capacity, commit to a two-track approach — secure short-term contract manufacturing capacity while advancing a mid-term-capex plan if unit economics warrant.

Partnerships and licensing: Identify platform partners with proven regulatory pathways and case studies for the target therapeutic area. Structure deals with milestone split tied to regulatory approvals and sales tranches.

Regulatory and payer pathing: Begin parallel planning now: engage regulators early on bioequivalence expectations and map payer evidence requirements to clinical endpoints.

M&A playbook: Target assets that fill immediate commercialization or CMC gaps; avoid speculative platform buys without validated manufacturing reproducibility.

Commercial readiness: Invest in clinician education and adherence measurement tools — these are high-ROI activities that support premium pricing and faster formulary uptake.

0–90 days: Rapid audit of pipeline candidates against our thin film scorecard; shortlist partners; initiate regulatory pre-submission meetings for priority candidates.

90–180 days: Execute development agreements or LOIs with CDMOs; begin pilot-scale runs; finalize payer evidence generation plans (including real-world evidence blueprints).

180–365 days: Finalize commercialization partnerships, secure manufacturing slots or commence facility upgrades, and lock-in launch pricing and contracting strategies aligned to payer evidence milestones.

We present three strategic trajectories in the full report (conservative, base, aggressive) that translate market growth parameters into tangible metrics for portfolio sizing, capex requirements, and time-to-revenue. Each scenario uses the same baseline growth dynamics but applies different adoption curves, reimbursement outcomes and partner availability assumptions. These scenarios are designed to help boards stress-test capital allocation decisions in 2026 under plausible market outcomes.

Thin film drugs represent a convergent opportunity: therapeutic differentiation, patient-centered benefit and novel commercial pathways. However, realizing that opportunity requires discipline in technical validation, manufacturing execution and commercial evidence generation. With the market expanding at a near double-digit growth rate into the next decade, 2026 is the year to convert exploratory programs into executable commercial strategies.

Our full PW Consulting report provides the market models, vendor scorecards, regulatory playbooks and M&A filters that enable rigorous 2026 decision-making. For access to the detailed segment models, downloadable templates, and full company profiles — and to schedule a strategy workshop tailored to your portfolio — please visit our report landing page or contact the PW Consulting industry team.

For detailed analysis of this topic, please visit the official page:Thin Film Drugs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com