Europe Footwear Sole Materials market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-20 11:41:35

As the automotive industry accelerates toward lighter, more efficient, and increasingly electrified vehicles, carbon fiber has moved from niche high-performance applications into the crosshairs of mainstream engineering and procurement strategies. This PW Consulting briefing synthesizes proprietary modelling and primary research from our Automotive Carbon Fiber Materials Market study (base year 2025, forecast 2026–2032) to surface the strategic imperatives that corporate leaders must act on in 2026. We intentionally present high-level, actionable intelligence here while withholding granular regional and application-level breakdowns to preserve the full analytic value of the complete study.

Automotive Carbon Fiber Materials Market

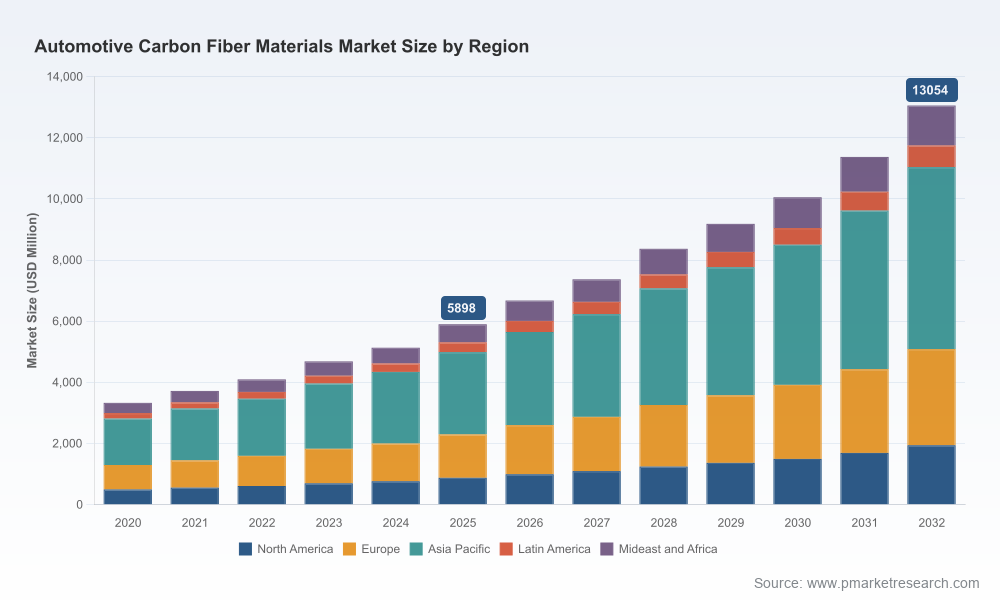

By our base year (2025) the global automotive carbon fiber materials market has reached roughly USD 5.9 billion in revenue. Looking ahead through our 2026–2032 forecast window, the market is projected to expand at a compound annual growth rate of approximately 12.1%, driving it to a multi‑billion dollar opportunity by 2032. This growth profile reflects a convergence of structural drivers — electrification-driven mass optimization, regulatory pressure on fleet efficiency, broader OEM acceptance of composite solutions, and accelerating product innovations that compress cost and cycle-time barriers.

Automotive Carbon Fiber Materials Market

The full PW Consulting study is built for corporate decision-makers. It combines quantitative forecasting with prescriptive playbooks and includes (summary):

Automotive Carbon Fiber Materials Market

Note: to preserve the decision advantage we provide in this public briefing, detailed regional splits, application revenue shares and unit-cost tables are reserved for the full report.

Manufacturers are actively reconfiguring capacity footprints to be closer to automotive OEM clusters. Announcements and phased expansions in 2025–2026 indicate capital is being deployed where lead-time reduction and local content capture matter most. For buyers, 2026 is the year to lock in long‑lead supply agreements or to co-invest in plant projects to secure preferential allocation as utilization tightens with demand.

Leading producers are bringing circular-process demonstrators into trade shows and pilot programs. Recycled-carbon backing plies integrated with virgin surfaces, and product lines with digital product passports, are active themes. The commercial implication is twofold: circular solutions will materially alter the cost curve for mid-volume applications, and sustainability-certified supply will become a procurement differentiator for OEMs with net‑zero pledges.

Recent product introductions target improved stiffness-to-weight and Class A surface finishes that meet consumer expectations for premium aesthetics without excessive secondary processing. This expands the addressable portfolio beyond performance cars and invites new design-for-manufacturing approaches at scale.

Raw-material volatility and discontinuation of non‑profitable product lines among some suppliers underscore a market pruning that will influence availability and price. Buyers must model margin exposure across alternative resin systems and recycled feedstocks and design procurement hedges accordingly.

Market leadership is a mix: global carbon-fiber producers, chemical groups, regional specialists, and precision-component integrators each bring distinct propositions — from high-performance fiber brands to vertically integrated composite systems. This uneven competitive map creates opportunities for niche consolidation and strategic partnerships.

This briefing outlines the strategic context and the actionable levers available to firms entering 2026. The full report provides the quantitative backbone — scenario tables, supplier scorecards, plant-level capacity maps, and executable commercial templates — necessary to convert strategy into contracts and investments. For executives planning capital allocation, supplier negotiation, or product architecture choices in 2026, the full dataset and playbooks are essential tools.

We have intentionally preserved the proprietary granularity that drives competitive advantage. To access the complete market segmentation, regional demand maps, and the detailed supplier benchmarking that underpins these recommendations, please visit the PW Consulting report page.

For detailed analysis of this topic, please visit the official page:Automotive Carbon Fiber Materials Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com