Calcium Carbonate Market 2026: Strategic Imperatives for Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a concise, decision-focused overview of our forthcoming Calcium Carbonate Market study. This preview synthesizes the report’s most consequential, data-driven insights for 2026 corporate planning while intentionally withholding the granular tables and segmented figures reserved for the full report. Think of this as the strategic trailer: enough to orient choices, not enough to substitute the primary intelligence set.

Calcium Carbonate Market

Market trajectory at a glance

The global calcium carbonate market is in a phase of steady, compounding growth. By our base year of 2025 the market approached approximately USD 56.8 billion in revenue and is projected to grow at a compound annual growth rate (CAGR) of roughly 5.21% over the 2026–2032 forecast window. Under base-case dynamics, the market moves from the 2026 opening year into a range that approaches the low eighties billion USD by 2032. This is not a boom-bust picture—the curve is characterized by persistent incremental demand, punctuated by capacity investments and regulatory inflections.

Calcium Carbonate Market

Why this matters for 2026 strategy

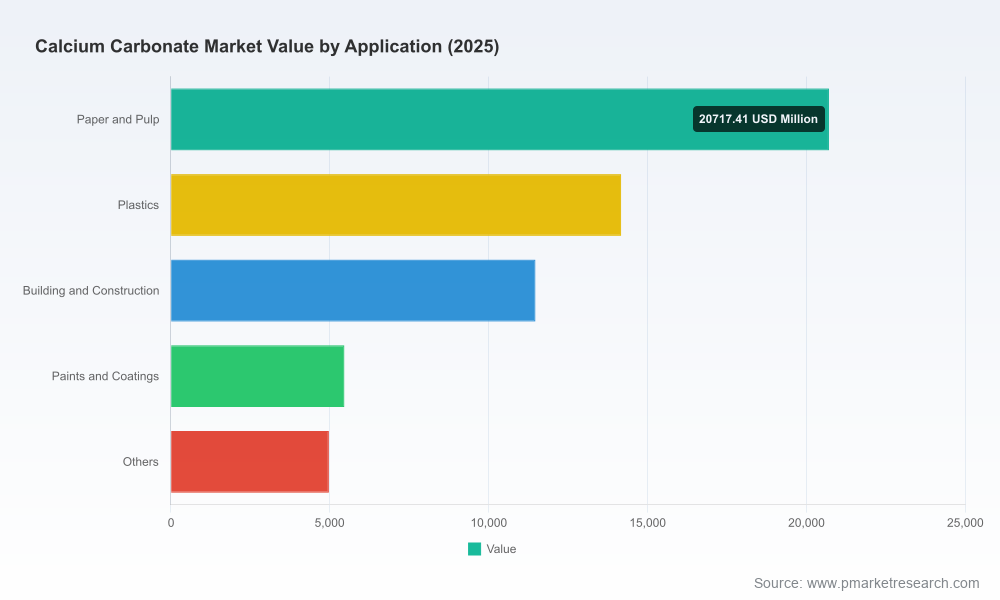

- Stable volume base, evolving mix: End-use demand remains diversified across paper & pulp, polymers and plastics, construction, paints & coatings, and specialty industrial uses. Stability in overall volumes creates room for selective investments in product differentiation rather than race-to-scale alone.

- Margin pressure from regulation and input costs: Carbon pricing in some regions and new tariffs have materially changed operating economics for calcination and cross-border trade. Expect regional operating-cost divergence to drive near-term reshoring and logistics optimization moves.

- Supply-side consolidation opportunities: The market concentration metrics show that the sector remains moderately fragmented at the global level. This drives natural M&A and bolt-on acquisition activity for players seeking to secure feedstock and distribution footprints.

- Product innovation as competitive currency: Suppliers are increasingly competing on engineered grades, sustainability credentials, and customer-specific on-site solutions. Differentiation is shifting value away from commodity pricing to performance and lifecycle cost.

Key 2026 strategic questions for stakeholders

- Supply security vs. cost optimization: Should procurement prioritize local, tariff-immune supply or global sourcing for spot savings? The answer hinges on your tolerance for supply disruption and the carbon-cost exposure of your plants.

- Decarbonization investment timing: With carbon pricing affecting calcination in jurisdictions like the EU and evolving carbon reporting globally, when and where does retrofitting or fuel-switching pay back?

- Downstream product positioning: Do you capture higher margins through engineered precipitated grades and specialty coatings, or by optimizing ground-calcium-carbonate (GCC) across commoditized applications?

- M&A and capacity planning: Where do bolt-on acquisitions create network effects—feedstock control, terminal reach, or specialty R&D—and what are realistic valuation benchmarks given current market concentration?

Supply-demand dynamics and price signals

Through 2025 and into early 2026 the market displayed relatively stable merchant price behavior for calcium carbonate, with transactional prices clustering in a narrow band. This stability masks heterogeneity at the plant and grade level: coated, engineered and precipitated grades show different margin profiles versus base GCC. Limestone remains the prevalent feedstock for the market, and regional mining and energy cost differentials are the principal sources of price dispersion.

Calcium Carbonate Market

Regulatory interventions materially reshape short-to-medium term dynamics. The U.S. tariff measures introduced in 2025 have already elevated landed procurement costs for select buyers and accelerated short-term investments in local capacity. In parallel, emissions pricing on calcination in key jurisdictions is re-ordering operating cost curves and shifting the calculus for older, high-emission assets.

Competitive landscape — what winners are doing

Global leadership is driven by a combination of integrated feedstock control, breadth of technical grades, and the ability to layer sustainability claims onto product performance. The full report contains deep-profiles on the sector’s principal players; below are strategic summaries of the companies that set the competitive tone.

- Imerys (Paris): A global leader in GCC production with an integrated mine-to-market model and recent North American capacity investments. Imerys leverages large-scale resource control and vertical integration to balance price volatility and service critical applications such as paints and construction.

- Omya (Oftringen): Focused on fillers, pigments and engineered solutions, Omya pairs sustainability-oriented product launches with on-site production models for large industrial customers. Recent innovations at industry exhibitions have fortified its position in polymer and biopolymer applications.

- Minerals Technologies (New York): A vertically integrated supplier emphasizing high-purity precipitated grades and specialty chemistries. The company’s expansion strategy targets markets where performance differentiation commands annuity-like margins.

- MLC – Mississippi Lime Company (St. Louis): A North American GCC incumbent that has used acquisition to broaden its mineral solutions portfolio and terminal footprint; recent transactions add operational capacity and market reach.

- Carmeuse & Lhoist (Brussels): Large European producers with deep exposure to construction and industrial applications. Their strategic focus balances regional production optimization with decarbonization roadmaps to mitigate EU operating cost pressures.

- Sibelco, Graymont, Calmit: Each brings distinct regional strengths—global filler coatings, chemical-grade supply chains, and European limestone expertise respectively—creating a competitive set that blends scale with localized service models.

Recent developments that matter for 2026 planning

- Early-2026 acquisition activity has intensified: a notable North American consolidation move closed in January, expanding a major producer’s capacity and mineral solutions portfolio—an example of the roll-up opportunities we expect to continue.

- Regional capacity additions are emerging outside traditional hubs: a new coated calcium carbonate plant began operations in East Africa in 2025, signaling diversification of supply and an opening for localized downstream development.

- Product innovation is accelerating: major suppliers used trade events in 2025 to launch sustainable, recycled-content and engineered filler solutions aimed at polymers and biopolymers—a clear signal that formulation and circularity are now primary battlegrounds.

What the full PW Consulting study delivers (practical contents)

The full market study is structured to support operational, commercial, and strategic decisions across the organization. Highlights include:

- Proprietary demand model with historic (2020–2025) and forecast (2026–2032) revenue curves by channel and application (note: detailed segment tables and regional breakdowns are available in the paid report).

- Price and margin matrices by grade, including scenario runs that incorporate carbon-pricing trajectories and tariff regimes.

- Supply-side atlas: plant-level capacity, recent expansions, and near-term project pipelines to assess local oversupply or scarcity risks.

- Company benchmarking: strategy maps, capability heatmaps, and M&A target scoring against four strategic plays—feedstock control, specialty engineering, geographic reach, and decarbonization capability.

- Commercial playbooks: procurement segmentation, supplier consolidation strategies, and go-to-market recommendations for launching engineered grades.

- Risk and regulatory matrices: impact assessment of food-safety recognition, emissions pricing, and trade measures on operating models and product eligibility.

- Executive dashboards and a prioritized implementation roadmap for 12–36 month decision horizons.

How to use this intelligence in 2026 (actionable guidance)

- Procurement leaders: Re-segment your supplier base by carbon and tariff exposure, then stress-test contracts using the report’s price-scenario module. Short-term hedging and longer-term supplier diversification are both valid responses depending on exposure.

- Operations and plant managers: Run asset-level economic sensitivity to carbon pricing and energy costs. The decision to retrofit, repower or retire older calcination assets should be driven by a three-year payback threshold tied to projected carbon costs.

- Commercial teams: Prioritize launch of engineered and certified low-carbon grades where customers are willing to trade price for lifecycle advantages. Use on-site or JIT production models selectively to lock-in strategic accounts.

- M&A teams: Target regional bolt-ons that secure feedstock or terminal access. The sector’s moderate fragmentation means well-priced acquisitions can materially lift CR and distribution economics.

Final note — what you don’t see here (and why)

This preview purposefully omits the detailed segmentation tables, regional/application percentage breakdowns and raw numerical matrices that underlie our recommendations. Those elements are the operational intelligence buyers use to model supplier contracts, site investments and acquisition valuations. If your 2026 planning depends on precise, auditable figures (price ladders by grade, plant-level capacities, or region-by-application demand curves), the full PW Consulting report and its supporting datasets are required.

To access the complete analysis, including downloadable datasets and interactive scenario tools tailored for procurement, operations and corporate strategy teams, please contact PW Consulting or visit our report page for subscription and licensing options.

For detailed analysis of this topic, please visit the official page:Calcium Carbonate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com