Grab Bars for Elderly and Senior Bathroom Safety: A Complete Guide to Safer Living Spaces

Other |

2026-06-18 19:10:54

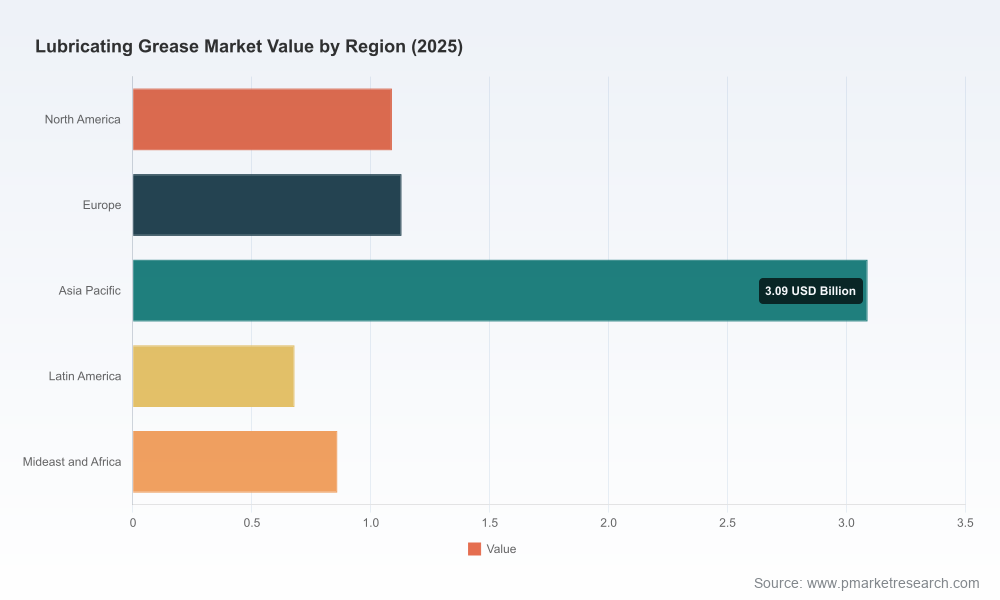

As companies rebase strategy for 2026, the lubricating grease market presents a classic case of steady growth intersecting with accelerating regulatory and technology-driven disruption. PW Consulting’s latest market study—anchored on a 2025 base year and a seven-year forecast horizon—shows a market that expanded from approximately USD 5.5 Billion in 2020 to roughly USD 6.85 Billion in 2025 and is projected to approach the USD 9.4 Billion mark by 2032, tracking a 4.6% compound annual growth rate over the 2026–2032 forecast period. For senior executives and business unit leaders, that combination of reliable topline growth and concentrated structural change demands a sharpened set of strategic responses in 2026.

Lubricating Grease Market

Planning horizon alignment: The report aligns near-term operational choices with mid-term portfolio outcomes—helping CFOs and portfolio managers reconcile 2026 capex and supply commitments with expected market dynamics through 2032.

Lubricating Grease Market

Regulatory risk mapping: It converts diffuse global regulatory signals into prioritized actions for product reformulation, inventory provisioning, and market access—critical for firms exposed to food-contact, industrial, and export-oriented channels.

Lubricating Grease Market

Competitive prioritization: With industry concentration skewed toward a few global majors (top-three firms account for just over half the market; top-five approach two-thirds), the study frames realistic competitive responses from mid-sized players and makes M&A and partnership opportunities actionable.

The market’s steady expansion through 2020–2025 demonstrates persistent demand across industrial maintenance, construction equipment, transportation and other applications. Forecasts to 2032 incorporate both the continuation of traditional demand drivers and incremental upside from fleet electrification tailwinds, improved industrial uptime economics, and higher-specification products for heavy-duty use. The 4.6% CAGR over the forecast period signals an environment in which volume growth can be meaningfully accretive to margins if firms manage product mix, raw-material exposure, and regulatory compliance efficiently.

Raw-material and feedstock context: Spot market indicators show lithium hydroxide price stabilization through 2024 after previous volatility. Stabilized base inputs reduce one element of margin uncertainty but do not eliminate cost exposure from other additives and specialty thickeners—companies must keep scenario-tested procurement strategies in place.

Regulatory acceleration on PFAS: Multiple jurisdictions moved decisively in 2024–2026. Notable regulatory signals include regulatory de-listings in food-contact matrices, REACH-level proposals tightening PFAS coverage in Europe, additions to toxic schedules under national chemical acts, and country-specific bans effective January 2026. The cumulative effect is to compress reformulation timetables and create differentiated market access pathways for PFAS-free offerings.

Technology and product innovation: The market is seeing parallel innovation vectors—high-performance synthetic chemistries for extreme environments, bio-based greases targeting sustainability mandates, and PFAS-free formulations for regulated markets. Early movers that validate performance parity at scale will capture premium share.

Consolidation and capacity moves: Recent capacity expansions by global majors and regional producers indicate targeted growth plays in food-grade, high-temperature, and heavy-industry segments. These moves alter supply risk and bargaining dynamics for buyers and create competitive urgency for specialty producers.

The competitive landscape is dominated by large integrated energy and specialty chemical firms alongside a set of high-performance lubricant specialists. Market concentration metrics indicate a market where the leading three firms collectively hold the majority share and the top five exert substantial influence over pricing norms, technology diffusion, and distribution reach.

Shell PLC (London): Offers an established family of lithium-based greases for bearings, open gears and multipurpose industrial uses. Their recent investment to expand food-grade high-temperature grease capacity underscores a strategy to secure compliance-sensitive customers and European food-supply chains.

ExxonMobil Corporation (Irving, Texas): Mobilgrease products anchor their portfolio, emphasizing high-temperature stability and water resistance—attributes that preserve OEM relationships and aftermarket lock-in in transport and heavy industry.

BP p.l.c. (London): Through Castrol-branded greases, BP balances automotive and industrial channels with an emphasis on widely specified OEM approvals and channel penetration.

FUCHS SE (Mannheim): A specialist player doubling down on high-performance lithium complex greases and introducing PFAS-free, bio-based formulations for REACH-compliant customers—an exemplar of differentiated product strategy aligned to regulatory trends.

Chevron Corporation (San Ramon): Focused on premium industrial and marine greases, leveraging integrated supply chains and global service contracts.

Klüber Lubrication (Munich): High-performance, extreme-condition greases that serve niche heavy-duty applications—positioned for technical differentiation and aftermarket support contracts.

Sinopec (Beijing): Regional scale plus recent capacity additions for high-temperature lithium greases targeted at steel and cement—illustrating the role of local supply scale in price-sensitive segments.

D-A Lubricant Company (Rockford): A specialized U.S. player with branded niche offerings for industrial and automotive use, representing an archetype of regional brand-strength leveraged into distributor networks.

Recent corporate actions—capacity expansions and targeted product launches—demonstrate two concurrent strategies: incumbents protecting margins and access through scale; and specialty players racing to establish PFAS-free and bio-based credentials. For market entrants and incumbents alike, the competitive playbook in 2026 will revolve around where to invest in formulation science, which channels to prioritize, and how to structure supply contracts that hedge regulatory risk.

PW Consulting’s study goes beyond high-level forecasting to deliver pragmatic, transaction- and implementation-focused assets tailored for 2026 execution:

Decision matrices for reformulation: Stepwise templates that translate PFAS scenarios into product-class actions, with cost-to-compliance estimates and performance validation checkpoints.

Supply-chain stress tests: Scenario models for raw-material shocks, alternative-thickener adoption curves, and contract-duration optimization to reduce working-capital strain.

Channel and margin playbooks: Profitability ladders by application class and go-to-market options (direct OEM supply, distributor-led aftermarket, segmented retail), enabling trade-off analysis between share and margin targets.

M&A and partnership screeners: A prioritized shortlist methodology for bolt-on acquisitions and joint ventures, calibrated to technology, capacity and geographic footprint objectives.

Capex prioritization model: Facility-level investment calculators that align expected incremental revenue, payback timings and regulatory compliance costs to de-risk 2026 capital decisions.

Immediate: Institute a PFAS risk-review across all product lines and markets. Where exposure is material, accelerate validation of PFAS-free substitutes or secure inventory and contractual buffers for transitional periods.

Medium term: Create a two-track product roadmap—optimize incumbent mineral-oil platforms for cost and reliability while piloting bio-based and PFAS-free formulations in regulated and premium channels.

Commercial: Revisit distributor contracts and OEM approvals to capture higher conversion value in specialty segments; consider multi-year supply agreements for critical additive inputs to stabilize procurement costs.

Portfolio: Use targeted M&A or JV to obtain local scale in high-growth industrial applications or to acquire formulation IP that accelerates time-to-market for compliant greases.

Use the research as both a diagnostic and an execution tool. The diagnostic layer benchmarks your current exposure—product, feedstock, regulatory and channel—while the execution layer provides prioritized projects and templates for immediate deployment by R&D, procurement, commercial and corporate development teams. Importantly, the study is constructed to translate strategic intent into 90-, 180- and 360-day workplans that align with 2026 fiscal calendars and board-level approval cycles.

This article previews the study’s strategic insights while intentionally withholding detailed segmentation tables, plant-level capacity maps, and the full set of financial-model worksheets—these are consolidated in the full PW Consulting report and accompanying data appendix. For procurement teams, R&D leaders and corporate development officers seeking the granular segmentation, application-level revenue models, and the full list of supplier contract templates, please consult the full report on our website.

In an industry where modest annual growth masks rapid regulatory and technological change, 2026 is the year to convert insight into protective and value-creating action. PW Consulting’s lubricating grease study is designed to be the playbook that makes those choices credible, measurable and executable.

For detailed analysis of this topic, please visit the official page:Lubricating Grease Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com