Ready-to-Fill Pastry Market Forecast Signals Rising Investment in Ready-to-Bake Solutions

Food |

2026-06-27 13:43:44

As companies plan capital allocation, supply-chain strategies, and product roadmaps for 2026 and beyond, the aluminium welding wires market presents a mix of structural growth, concentrated supply, and acute commodity-driven risk. This preview distils the strategic implications from PW Consulting’s latest market research to help executives move from high-level interest to concrete decisions — while preserving the granular datasets and proprietary models for subscribers who access the full report.

Aluminium Welding Wires Market

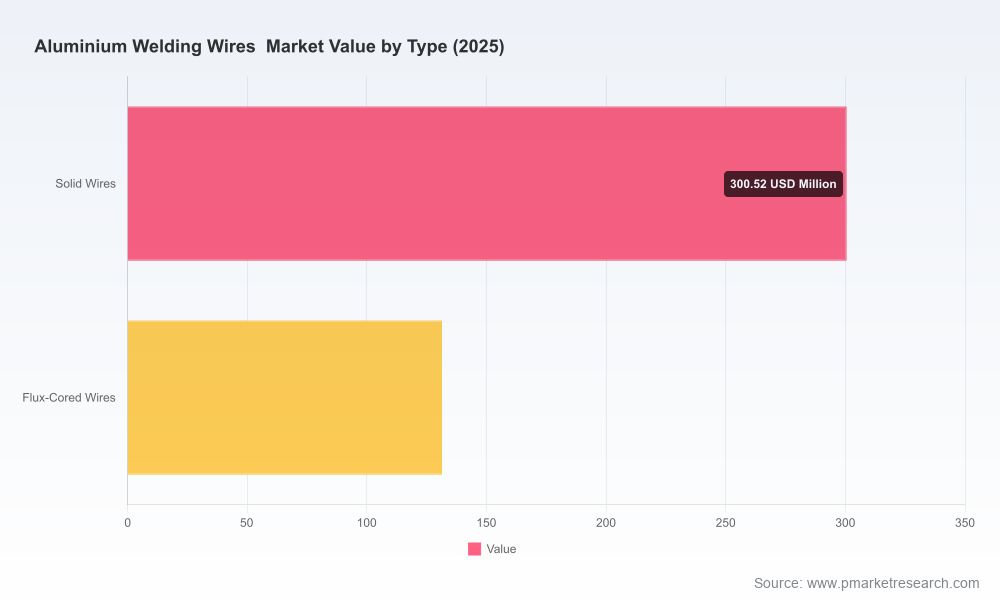

Our base-year analytics (2025) and historical series (2020–2025) show the aluminium welding wires market has expanded consistently, driven by adoption in mobility, marine, and light-structure construction segments. The market reached a material inflection point in the early 2020s and is expected to continue growing through the forecast period (2026–2032) at a compound annual growth rate (CAGR) of approximately 5.5%. PW Consulting’s topline projection places the total market in the mid‑2020s at a level that underpins near‑term capacity investments and supports resilient supplier economics through 2032.

Aluminium Welding Wires Market

For decision-makers, two implications follow immediately: first, the market is large and growing enough to justify targeted investment in specialty alloys, automation-friendly packaging, and quality assurance programs; second, the growth is predictable enough to underpin multi‑year contracts, but not so rapid as to eliminate the need for active competitive differentiation.

Aluminium Welding Wires Market

Commodity volatility and its operational impact — Aluminium price volatility has escalated into a defining dynamic. Sharp year‑over‑year increases in primary aluminium spot prices are translating into working‑capital stress and margin pressure across the value chain. Procurement teams must treat aluminium as a strategic raw material: implement multi‑scenario hedging, renegotiate cost‑pass‑through clauses, and evaluate tolling or consignment models with integrated suppliers.

Product innovation driving productivity — Recent launches and product updates demonstrate a market bias toward weldability and on‑line productivity. Examples include high‑feedability alloys tuned for robotic MIG/TIG lines and larger spool formats that materially extend run‑time between changeovers. These innovations reduce per‑part labor and increase throughput for customers deploying automation.

Traceability, standards and certifications — Buyers increasingly require traceable lots and compliance with welding standards. Certification and lot traceability have become de‑facto purchase criteria in aerospace, shipbuilding and regulated industrial applications. Suppliers that can document metallurgical provenance and offer certification-ready materials gain premium access to critical tenders.

Digital tools for defect prevention — New digital tooling that predicts weld risk and prevents defects is emerging. Early adopters of such tools report lower rework, improved first‑pass yield, and enhanced warranty economics. Integrating these tools with consumables and process parameters is rapidly evolving from boutique capability to mainstream supplier differentiation.

Supply concentration and strategic implications — The market exhibits moderate concentration among a small group of global and regional incumbents. This concentration creates both opportunities for scale players to tighten margins and openings for specialized players to capture niche, high‑value segments by offering alloy expertise, faster supply, or regulatory compliance assurance.

End‑market transport dynamics — Demand for lightweight vessels and vehicles continues to rise, with notable percentage increases in aluminium‑intensive designs aimed at fuel efficiency. For welding wire suppliers, this underpins sustained demand for higher‑performance alloys and weld procedures tailored to thin‑gauge, high‑strength applications.

The supply side is a mix of global conglomerates and specialized manufacturers. Several players have signalled strategies that reveal the direction of competitive differentiation:

Nexal Aluminum (Canada) — Nexal has positioned itself as a premium, integrated North American manufacturer. Its recent catalog and product updates emphasize alloys engineered for robotic and high‑volume MIG/TIG applications, with a continued focus on feedability and porosity minimization. Nexal’s elimination of added beryllium in product formulations is a notable safety and compliance differentiator that reduces risk for customers in regulated industries.

Berkenhoff GmbH / Bedra (Germany) — Known for a broad alloy portfolio and corrosion‑resistant formulations, Bedra is also moving into digital risk mitigation with tools designed to preempt welding defects. Their product‑plus‑software approach targets shipbuilding and chemical‑plant applications where both alloy performance and process control are critical.

Lincoln Electric (United States) — A vertically integrated incumbent, Lincoln continues to leverage full‑facility control to offer secure supply to shipbuilders and heavy fabrication customers. Their value proposition blends consumable supply with deep technical support for complex welds.

ESAB (United States) — ESAB’s recent introduction of larger spool formats addresses a clear productivity gap on automated and semi‑automated lines. Coupled with lot traceability and certification compliance, ESAB targets high‑uptime manufacturing environments seeking lower changeover costs and audit‑ready supply documentation.

NS ARC (United States) — As a specialty‑brand supplier, NS ARC focuses on high‑strength, crack‑resistant alloys for demanding fabrication contexts. Its niche positioning appeals to fabricators and OEMs that prioritize metallurgical performance over commodity pricing.

Sumitomo Electric Industries (Japan) — Sumitomo’s continuous casting capabilities highlight a process‑technology advantage for consistent feedstock quality in large‑scale shipbuilding and automotive assembly applications.

Collectively, these vendors illustrate two parallel competitive paths: scale and integration (security, cost leadership, certification) versus specialization and innovation (advanced alloys, digital tools, productivity‑enhancing formats). For buyers and investors, the choice between these routes informs partner selection and M&A appetite.

The full report is structured to be immediately actionable for procurement, manufacturing, product, and corporate strategy teams. Key deliverables include:

These components are supported by proprietary datasets, supplier interviews, and process‑level benchmarks that allow teams to move from strategic intent to procurement and operations implementation within a single planning cycle.

Embed raw‑material scenario planning into capital decisions — Given current commodity price trends, require a minimum of three aluminium‑price scenarios in any CAPEX evaluation and stress‑test payback timelines under sustained elevated cost assumptions.

Prioritise automation‑friendly form factors — Larger spools and feeds designed for robotic lines reduce labor dependence and downtime. Incentivise suppliers that offer productivity metrics tied to spool life and feeder compatibility.

Insist on traceability and certification as purchase qualifiers — For aerospace, marine, and regulated construction applications, certification and lot traceability should be non‑negotiable. This reduces audit risk and TCO related to rework and liability.

Evaluate blended sourcing and localised buffer stocks — Combine strategic contracts with regional buffer inventories to mitigate transport and tariff disruptions without overcapitalising working capital.

Pursue supplier co‑development for alloy and digital bundles — Firms that co‑develop weld procedures, digital defect‑prevention tools, and alloy tweaks secure preferential pricing and faster time‑to‑market for new products.

Monitor M&A and partnership signals — The market’s moderate concentration suggests M&A will remain a lever for scale and capability acquisition. Use supplier scorecards to prioritise targets that add alloy expertise, traceability, or automated‑format manufacturing.

This article is intended as a strategic “trailer” that highlights the essential market forces and competitive moves that will matter to executives in 2026. The full PW Consulting report contains the granular regional and application splits, per‑company capacity sheets, and downloadable financial models that enable implementation. If your team needs a tailored brief — for procurement renegotiations, CAPEX boards, or M&A screening — the report also supports custom deep‑dives and scenario workshops.

For organizations that must move from planning to action in 2026, success will depend on three linked capabilities: disciplined commodity risk management, selective investment in productivity‑preserving formats and digital controls, and supplier strategies that balance security with specialised performance. The aluminium welding wires market offers predictable growth and tangible levers to improve manufacturing economics; the full PW Consulting analysis supplies the datasets and playbooks required to convert that potential into measurable commercial outcomes.

To access the full dataset, company profiles, and executable playbooks — including the region‑ and application‑level intelligence intentionally withheld from this preview — visit our report page or contact PW Consulting to request the full Aluminium Welding Wires Market report and a tailored executive workshop.

For detailed analysis of this topic, please visit the official page:Aluminium Welding Wires Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com