Indonesia Thermal Coal Market Outlook: Forecasting the Next Decade of Strategic Energy Supply

Other |

2026-03-28 11:00:18

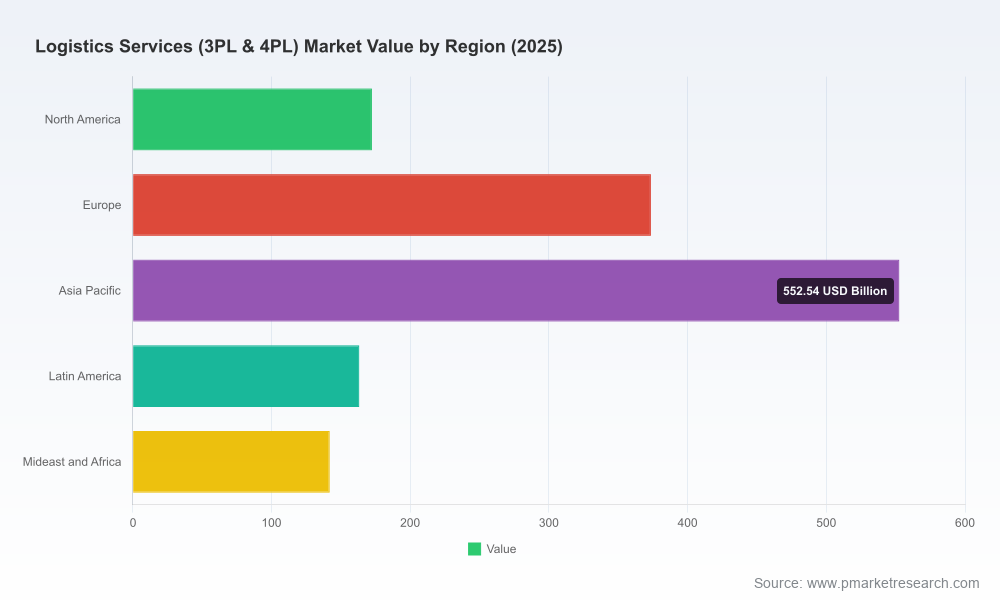

As global supply chains enter a renewed phase of transformation, third- and fourth-party logistics providers (3PLs and 4PLs) are shifting from cost-takers to strategic partners. Our PW Consulting market study — anchored on 2025 as the base year and covering historical dynamics from 2020–2025 with forward projections through 2032 — quantifies and contextualizes that shift. The global Logistics Services market is sizable and accelerating: from roughly USD 1.4 trillion in 2025 it is projected to approach USD 2.6 trillion by 2032, expanding at a compound annual growth rate (CAGR) of approximately 9.25%. For senior leaders planning investments, partnerships, or capability buildouts in 2026, this study provides the empirical foundation and implementation playbook to act with confidence.

Logistics Services (3PL & 4PL) Market

Timing: 2026 is the inflection year in our model where technology-enabled orchestration and reshoring/nearshoring trends intersect with a maturing 4PL value proposition. Decisions taken now — on automation, partner selection, and operating models — will determine cost-to-serve and resiliency positions for the next business cycle.

Logistics Services (3PL & 4PL) Market

Signal-to-noise clarity: The market is noisy: trade-show announcements, vendor hype, and fragmented regional dynamics can obscure durable strategic differentiators. This report synthesizes quantitative trajectories and qualitative drivers so C-suite and supply chain leaders can separate tactical fixes from structural investments.

Logistics Services (3PL & 4PL) Market

Risk-calibrated growth: With an established multi-year growth trajectory, leaders must balance capacity investments against volatility (labor, regulatory shifts, modal capacity). Our scenario analyses and stress-tests provide a calibrated view of upside and downside outcomes under plausible macro and industry shocks.

Three macro forces underpin the projected near-doubling of market value by 2032: continued digitization and orchestration (favoring 4PL frameworks), elevated omnichannel complexity (sustaining demand for specialized 3PL execution), and structural shifts in trade and manufacturing footprints (reshoring, nearshoring, and network rebalancing). Technology is not an add-on; it is the multiplier. Providers who combine automation, advanced planning, and data-driven orchestration create an asymmetric value proposition—reducing working capital, improving throughput, and delivering predictable service levels across modes.

Operationally, labor constraints and the scarcity of qualified supply chain talent remain persistent themes identified in authoritative industry studies. These constraints amplify the value of automation, flexible labor models, and partnerships that can quickly scale capacity. In parallel, volatility in transportation capacity continues to pressure lead times and costs, making dynamic spot- and contract-mix strategies essential for shippers and providers alike.

Executive dashboards: consolidated market sizing, trend decomposition, and scenario projections (base case, conservative, upside), enabling board-level discussions supported by empiric growth paths.

Capability scorecards: a playbook-style assessment framework for evaluating 3PL/4PL partners across technology, operations, geographic reach, and commercial constructs—designed for rapid vendor shortlisting and RFP design.

Implementation roadmaps: stepwise blueprints for transitioning from multiple tactical 3PL contracts to an orchestrated 4PL model (when appropriate), including governance, KPIs, and staged tech integration plans.

Commercial and TCO models: decision-ready templates to compare build vs. buy scenarios, measure total landed cost impacts of modal shifts, and quantify payback horizons for automation investments.

Scenario stress-tests: sensitivity analyses that model the impact of key shocks — labor scarcity, sudden modal capacity contraction, tariff shifts — on network cost and service metrics.

Appendices with primary research: interviews, proprietary survey data, and vendor capability matrices to support due diligence and shortlisting.

The competitive field combines global integrators, regional specialists, and technology-forward disruptors. The market remains moderately concentrated: the largest global integrators collectively account for roughly a quarter of market volume, leaving extensive room for regional champions and niche specialists. Our competitive analysis profiles the leading operators and distills strategic implications for prospective buyers and investors.

C.H. Robinson — a broad-based logistics integrator that has doubled down on AI and cross-modal orchestration. Their recent introduction of autonomous 4PL management capabilities signals an aggressive push to move beyond traditional brokerage into full-stack orchestration.

GXO Logistics — focused on contract logistics and automation-heavy warehousing. GXO’s play is to convert scale automation and reverse logistics capabilities into differentiated service offerings for retail and consumer-facing clients.

Expeditors — retains strengths in freight forwarding and customs proficiency, positioning itself as a resilient partner for complex cross-border flows where regulatory navigation and customs expertise are high-value.

Kuehne + Nagel, DHL Supply Chain, and DSV — the traditional global integrators continue to compete on global network depth, multimodal control towers, and industry-specific vertical services. Their advantages lie in scale, modal coverage, and the ability to invest in platform-level orchestration.

XPO Logistics and J.B. Hunt — strong in North American execution, with differentiated asset-or-light hybrid models that appeal to shippers seeking flexibility in transportation and warehousing.

Geodis and CEVA Logistics — European-focused operators leveraging freight forwarding heritage to expand contract logistics and 4PL orchestration capabilities, particularly for manufacturing and industrial customers.

For buyers and investors, the practical takeaway is to map provider strengths to the node-specific needs of your network: who can deliver automation at scale in your fulfillment nodes; who brings best-in-class customs and cross-border visibility; and which integrator can orchestrate an end-to-end outcome without creating single points of failure.

Product innovation: The market is moving from incremental automation to systems that claim autonomous orchestration across modes. Early commercial launches underscore the need to pilot, validate KPIs, and insist on transparent measurement frameworks before scaling.

Industry forums: Large industry conferences in 2026 continue to reinforce the convergence of supply chain resilience and digital transformation priorities. These forums are valuable for benchmarking capability maturity and sourcing partner references.

Operational headwinds: Industry reporting highlights persistent labor constraints and modal volatility. These dynamics make flexible network designs and variable-cost operating levers more attractive for shippers than large fixed-capex investments in certain geographies.

C-suite: Use the executive scenarios to validate capital allocation decisions and to prioritize initiatives (automation, 4PL pilots, supplier consolidation) with expected ROI windows aligned to the 2026–2028 inflection.

Supply chain leaders: Leverage the vendor scorecards and implementation roadmaps to run vendor selection processes that are outcomes-focused (e.g., service consistency, inventory turns) rather than compliance-focused.

Investors and private equity: Apply the market sizing and concentration insights to identify acquisition targets where scale, technology, or niche specialization can unlock multiple expansion levers.

Regional operators: Use the scenario stress-tests to prioritize resilience investments where labor and capacity shocks are most likely to cascade across your network.

This article is designed as a high-fidelity preview: it provides strategic context, methodological orientation, and practical outputs without disclosing the full granularity of the report. The full report contains the detailed regional and application segmentation, vendor-level benchmarking, and downloadable financial models that underpin the headline projections. We intentionally withhold some segment-level figures in this preview to preserve the action-oriented value of the primary publication and to direct practitioners to the full dataset for decision execution.

For teams preparing to invest in 2026, we recommend three immediate actions informed by our study:

Run a 90-day partner audit: map current provider capabilities, overlay critical gaps against near-term demand drivers, and identify 1–2 pilot initiatives (automation, 4PL orchestration, or network densification).

Model three finance-backed scenarios: base, conservative, and upside — using the report’s templates — to test capital allocation and commercial structures under different levels of demand volatility.

Pilot a data “integration sprint”: focus on visibility (end-to-end), exception management, and a single source of truth for carrier performance; these are the enablers for any 4PL transition.

The Logistics Services market is entering a strategic phase where orchestration, digital maturity, and flexible cost structures will determine which organizations capture disproportionate value. The projected growth path through 2032 underscores both opportunity and urgency. Our full PW Consulting study equips leaders with the numbers, narratives, and execution tools needed to move from intent to impact in 2026. For practitioners ready to convert insight into action, the comprehensive datasets, vendor matrices, and implementation templates in the full report are purpose-built to accelerate that journey.

To access the full dataset, vendor scorecards, and downloadable models, visit the report landing page — the detailed evidence base is there to support procurement, investment, and operational decisions in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Logistics Services (3PL & 4PL) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com