Electric Control Cabinet Market — Strategic Outlook for 2026 Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a forward-looking primer to orient executives, M&A teams, procurement leaders, and product strategists preparing decisions in 2026. This brief synthesizes the report’s macro findings and the high-confidence implications you will need to act on immediately — while preserving the full data tables and proprietary segment breakouts for subscribers. Consider this a trailer: deep enough to validate our methods and conclusions, intentionally curated to prompt a direct visit to the source for the detailed intelligence that will materially change your plans.

Electric Control Cabinet Market

Market snapshot: trajectory and structural facts

The electric control cabinet market has moved from a mature industrial component to a dynamic battleground for modularization, digital services and regulatory compliance. Using 2025 as the report base year, PW Consulting’s topline estimate for the market was USD 1,050 Million. Under our central scenario the market is projected to grow at a 6.5% CAGR through the 2026–2032 forecast window, reaching approximately USD 1,650 Million by 2032. Historical context (2020–2025) shows steady recovery and structural re-investment in automation and energy infrastructure, setting the stage for sustained mid-single-digit growth.

Electric Control Cabinet Market

Market concentration is modest by heavy-industrial standards: the three‑firm and five‑firm concentration ratios are low‑to‑moderate (CR3 ≈ 25.8%, CR5 ≈ 28.5%), indicating meaningful room for both global leaders and regional specialists to expand share through product differentiation, service offerings and selective consolidation.

Electric Control Cabinet Market

Why 2026 is a strategic inflection point

- Capital allocation window: Maintenance capex and modernization programmes postponed during the pandemic are converging with new investments in EV charging, smart buildings and distributed energy resources — creating a near-term spike in tender activity.

- Regulatory re‑readiness: Standards and certification pathways (notably the UL 508A program and NFPA 79 compliance regimes) are now key procurement filters; firms that can demonstrate program participation and certified production will unlock higher-volume customers more quickly.

- Technology leverage: Advances in modular enclosures, digital interlocks, and AI-assisted design and testing change cost curves — early adopters will shorten time-to-deploy and command premium margins.

Primary demand drivers and headwinds

- Automation re-platforming: Renewed adoption of factory automation and retrofits in process industries continues to be the single largest demand engine. Purchasing decisions are increasingly shaped by integration readiness (PLCs, fieldbus, ethernet/IP, digital I/O).

- Infrastructure and energy transitions: Rollouts of EV charging infrastructure, microgrids and distributed renewables create sustained demand for stainless steel, aluminum and polycarbonate enclosures suited to outdoor and corrosive environments.

- Regulatory and certification costs: Compliance with UL 508A and NFPA 79, plus mandatory staff training for program adherence, raise the bar for new entrants and increase the value of certified panel-builders.

- Raw material volatility: Fluctuations in steel and aluminum prices compress margins and drive localized sourcing strategies and hedging tactics. Firms that optimize material substitution and standardized bill-of-materials gain resilience.

Technology, product and delivery trends

- Modularization and pre‑assembly: Demand for delivery-ready, modular cabinet systems accelerates installation timelines and reduces site labor risk — a competitive lever for global suppliers.

- Embedded intelligence and digital twins: Manufacturers are piloting AI-generated cabinet designs and virtual validation workflows, reducing engineering cycle times and lowering field start-up failures — highlighted by recent public demonstrations in industry expos.

- Service commercialization: Warranty extension, remote diagnostics, spare-parts-as-a-service and subscription-based monitoring are emerging as meaningful revenue streams beyond the initial sale.

Competitive landscape — what the leaders and specialists are doing

The market features a mix of global platform players, regional enclosure specialists and custom panel builders. Below are high-level strategic positions of core participants evaluated in the report.

- Rittal GmbH & Co. KG (Germany): Strong in modular cabinet platforms and global systems integration. Competitive advantage: systems engineering, modularity and channels into machine-building OEMs.

- Schneider Electric SE (France): Broad automation ecosystem; leverages software and services to position control cabinets as part of end‑to‑end electrification solutions.

- Siemens AG (Germany): Integrated control solutions with depth in process control and factory automation; differentiates on system integration and lifecycle services.

- ABB Ltd (Switzerland): Focused on motor control and power distribution; strong OEM relationships and project execution in energy-intensive sectors.

- nVent Electric plc (USA): Known for NEMA/UL-rated enclosures and harsh-environment solutions; plays to reliability and regulatory compliance demands.

- Phoenix Contact (Germany): Component and cabinet-level solutions with fast integration into control systems; notable for R&D partnerships and early demonstrations of AI-generated cabinets.

- Regional/custom specialists (PanelTEK, Saginaw Control, ESL Power, Keltour, Excelpro, The Industrial Controls Company, SE‑MAR, KDM Steel): These firms compete on UL 508A certification capabilities, customization speed, local presence, and price elasticity for mid-market OEMs and contractors.

Recent industry activity underscores two dynamics: (1) product innovation and demonstration (product launches and AI-assisted exhibits at trade shows), and (2) recognition of specialist manufacturers for certification and niche execution. These signals validate our view that winning requires both product breadth and executional rigor at the factory level.

Strategic implications and recommended actions for 2026

- For global platform players: Prioritize modular, pre-certified product lines and bundled services (installation, digital monitoring) to capture lifecycle margins. Accelerate partnerships with systems integrators to shorten sales cycles in EV and building automation segments.

- For regional specialists: Invest selectively in UL 508A program participation and staff training to become preferred bidders for repeat OEM contracts. Use digital quoting and BOM standardization to improve margins and win-volume throughput.

- For procurement and OEMs: Build a supplier scorecard that weights certification readiness, delivery lead times, and aftermarket service — not just unit price. Consider dual-sourcing strategies for critical enclosure materials to manage raw-material volatility.

- M&A and corporate development teams: Target bolt-ons that provide certified production capacity, regional footprints, or specialized materials capability (stainless, polycarbonate). Small additive acquisitions can move the CR3 and CR5 dynamics materially in regional markets.

- R&D and product teams: Pilot AI-assisted design-for-manufacture workflows and invest in digital twin validation for high-volume cabinet designs to compress time-to-order and reduce first-time‑right failures.

What PW Consulting’s full report delivers (practical tools and deliverables)

The full Electric Control Cabinet Market report is structured around actionable outputs designed to be used directly by commercial teams, product managers and corporate strategy groups. Highlights include:

- Executive summary and 2026 decision playbook with prioritized actions by company type.

- Topline market forecasts (2026–2032) including scenario analysis and sensitivity to raw‑material and regulation shocks.

- Competitive benchmarking with capability heat maps and supplier maturity scores (commercial, operational, certification).

- Procurement toolkit: supplier scorecards, RFQ templates, and a TCO model calibrated to enclosure materials and certification pathways.

- Go‑to‑market and product roadmaps for modular cabinets, digital services and aftermarket monetization.

- M&A target shortlists and valuation heuristics for tuck‑ins that accelerate certification, regional expansion or vertical integration.

- Case studies and factory-level diagnostics showing benchmarked cycle times, cost drivers, and improvement levers.

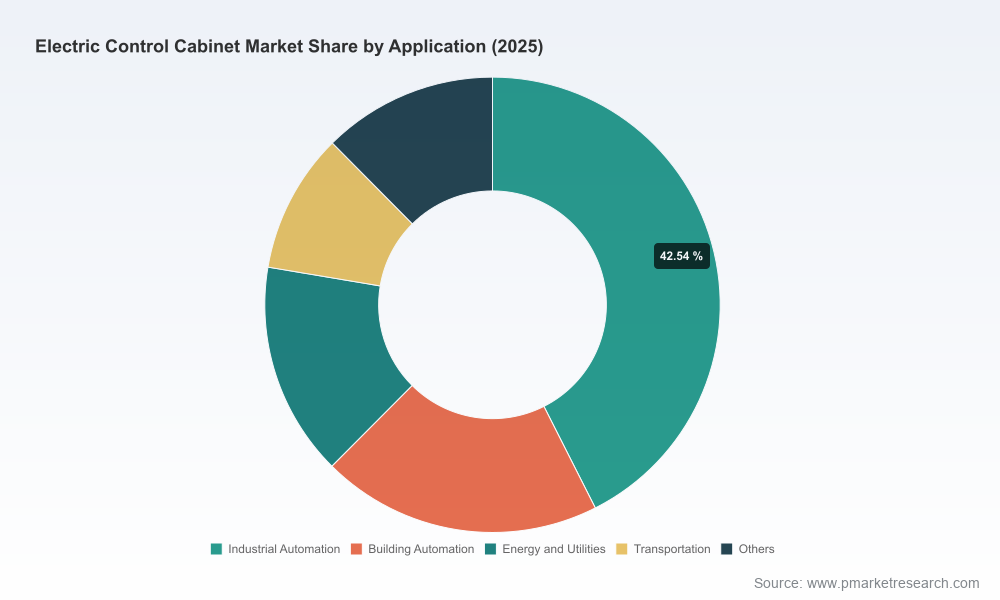

Note: To preserve the research’s commercial integrity, this preview intentionally excludes the detailed segmentation tables and regional/application split metrics contained in the subscriber dataset. Those granular slices — which drive bespoke procurement and M&A scenarios — are available in the full report package and accompanying Excel model.

Risk register — what keeps operators awake

- Material price shocks: steel and aluminum price swings can erode margins quickly unless hedged or managed via material substitution strategies.

- Certification bottlenecks: delays in UL program enrollment or skilled-staff availability can create delivery backlogs for high-volume tenders.

- Competition from integrated suppliers: firms that bundle software, controls and enclosures can disintermediate traditional cabinet suppliers unless they evolve into solutions providers.

- Macro slowdowns: an industrial capex pullback would compress growth below the central 6.5% CAGR scenario — contingency plans should be ready by mid‑2026.

Next steps — how to use this insight

If your 2026 strategic plan includes any of the following — re‑sourcing of control cabinets, investment in a certified panel-building capability, launching modular product lines, or evaluating M&A to secure regional capacity — the full PW Consulting study provides the granular data and decision support tools you will need to set budgets, negotiate contracts, and prioritize pilots. For direct access to the full dataset (including regional and application splits, detailed supplier profiles, and our Excel modeling toolkit), please visit the PW Consulting report page or contact our commercial team to schedule a briefing and model walkthrough.

In complex industrial markets, timing matters. The next 12–24 months will separate those who merely survive from those who expand margins and capture the systemic upside of electrification and automation. Our study is built to convert market visibility into executable advantage.

For detailed analysis of this topic, please visit the official page:Electric Control Cabinet Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com