Dissolving Pulp Market — Strategic Briefing for 2026 Decision‑Makers

This insight note, prepared by PW Consulting’s strategy practice, frames the strategic imperatives derived from our full Dissolving Pulp Market study (base year 2025, historical period 2020–2025, forecast 2026–2032). It is written for C‑suite leaders, corporate development teams, procurement heads and institutional investors who must make binding choices in 2026 — from capacity allocation and sourcing strategy to M&A and regulatory contingency planning. The objective is to demonstrate the analytical depth and actionable orientation of our research while reserving the full, transaction‑grade detail for the complete report and data annexes.

Dissolving Pulp Market

Market snapshot: what the numbers tell us

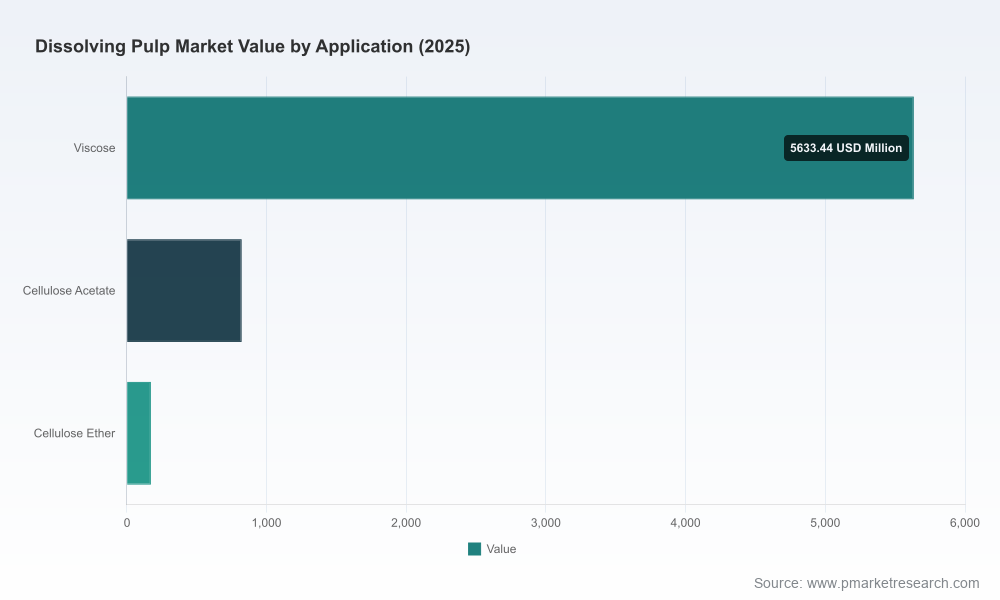

Our market model shows dissolving pulp as a stable, slowly expanding market, with a compound annual growth rate (CAGR) of 3.05% across the 2026–2032 forecast window. After gradual recovery through the early 2020s, the industry reached a base market size of USD 6,628.9 Million in 2025 and is projected to continue expanding under existing demand drivers and structural supply changes. Growth is driven by balanced demand between regenerated textile fibres, acetate and ether derivatives, while supply dynamics are increasingly shaped by feedstock availability, mill reconfigurations and regulatory shifts.

Dissolving Pulp Market

Why this matters for 2026 strategic choices

- Capacity decisions are no longer binary. Small changes in line reallocation or mothballing at a single large producer can shift regional supply balances and price differentials. As some producers prioritize specialty grades and others optimize for cost, 2026 will be a year where incremental capacity moves translate into outsized commercial opportunities for nimble offtakers and processors.

- Sourcing and feedstock risk require a forward posture. Raw material shocks — such as the 2023 global spike in eucalyptus wood chip prices following adverse weather in key producing regions — illustrate that feedstock volatility can compress margins rapidly. Contract design, supplier diversification and upstream partnerships must be central to procurement playbooks.

- Regulatory noise is a strategic risk. Trade and anti‑dumping/commercial investigations introduce execution risk for cross‑border supply chains. The initiation of trade remedial proceedings in late 2025 is already changing negotiation dynamics and should be factored into 2026 tender timelines and insurance pricing.

- Concentration matters for negotiation and consolidation strategy. The top three and top five producers together account for a material share of global capacity, producing a marketplace where a few corporations can influence spot availability and lead times. This creates both leverage for large buyers and acquisition rationale for private equity and industrial players seeking to secure feedstock and downstream integration.

Key thematic drivers identified in the report

- Product mix evolution: Demand for higher‑purity grades for pharmaceutical, cellulose acetate and specialty chemical applications is growing faster than commodity viscose requirements. That shift favors mills with investments in quality control, bleaching and pulping technologies.

- Feedstock supply chains: Plantation management, chip logistics and pulp‑grade wood availability now determine long‑run cost curves. Weather patterns, transportation bottlenecks and port congestion are recurring stress points in our scenarios.

- Sustainability and certification: Buyers increasingly price chain‑of‑custody and lifecycle metrics into procurement decisions. Certification programs — and the ability to demonstrate traceability — are material to winning long‑term contracts with textile and pharma customers.

- Trade and policy risk: Tariffs, investigations and non‑tariff measures can materially rewire trade flows within months. Producers and buyers must maintain contingency routing and alternative supplier options.

- Vertical integration and conversion economics: The cost and availability of converting dissolving pulp into regenerated fibres, acetate and ethers determine the margin capture potential for integrated players versus merchant suppliers.

What the full report contains (operational and strategic tools)

The complete PW Consulting study is designed as a practical decision toolkit. Highlights include:

Dissolving Pulp Market

- Proprietary demand model covering 2020–2032 with multiple demand scenarios (baseline, downside and high‑growth) and sensitivity levers for feedstock price, conversion rates and regulatory outcomes.

- Price curve scenarios and spot vs contract pricing mosaics, including scenario testing for alternative feedstock and energy cost paths.

- Supplier scorecards and a capex & capacity tracker with commissioning schedules for announced projects and historical utilization trends.

- Regulatory risk matrix with actionable playbooks for trade investigations, mitigation steps, and likely timelines for remedies and appeals.

- M&A and partnership playbooks: valuation benchmarks, synergies calculators, diligence checklists and a shortlist of potential targets and acquirers by strategic rationale.

- Commercial templates for offtake contracts, hedging clauses and sustainability KPIs that align buyer/seller incentives while protecting margin and supply security.

To preserve the commercial value of our segmentation and supplier‑level analytics, the report intentionally withholds granular regional and application splits within this briefing — these are available with the full dataset and interactive dashboards.

Competitive landscape — practical implications for 2026

Our competitive analysis profiles incumbent producers and highlights strategic moves to watch in 2026:

- Large integrated players with plantation access and conversion capability. These producers benefit from capture opportunities when the premium for specialty grades widens and when integrated fibre producers seek secure internal supply. Their 2026 strategies will likely center on optimizing product mix and strengthening long‑term offtakes.

- Specialty and high‑purity focused mills. Facilities that produce ultra‑high alpha‑cellulose grades for acetate and pharmaceutical markets command different risk/return profiles and often pursue smaller volume, higher margin customers. Continued process upgrades and yield improvements will be core 2026 capex themes.

- Resource‑constrained merchant suppliers. Merchant players who lack captive fibre supplies face higher exposure to feedstock swings; expect heightened commercial activity — long‑term contracts, tolling arrangements, and selective geographic reorientation to hedge risk.

- M&A and alliance activity. Given the market concentration dynamics, 2026 could see targeted acquisitions to secure feedstock, expand specialty capacity or integrate downstream into fibre or acetate production, particularly where regulatory uncertainty creates temporary dislocations.

Notable company developments that inform our 2026 outlook include reallocation of mill lines toward dissolving pulp by major producers and ongoing process upgrades at specialty mills. These moves, alongside trade actions initiated in late 2025, will influence supply availability and negotiating leverage across the value chain.

Scenarios and near‑term risks

- Base scenario: Gradual market expansion in line with the 3.05% CAGR, moderate price volatility and steady substitution patterns.

- Downside scenario: Escalation of trade remedies and sustained feedstock price increases that compress margins for merchant suppliers and accelerate consolidation.

- Upside scenario: Faster adoption of sustainable regenerated fibres and expanded pharmaceutical demand that increases premium segment growth and rewards capacity additions targeted at high‑purity grades.

Key risks to monitor in 2026 include trade investigations affecting major exporting countries, supply disruptions from weather and logistics, and faster‑than‑expected substitution in end‑markets driven by regulatory or brand commitments to sustainability.

Actionable priorities for executives in 2026

- Lock in strategic offtakes with graduated pricing. Negotiate multi‑year contracts with volume bands and indexed pricing to protect against feedstock and freight swings while preserving upside participation should spot soften.

- Run rapid supplier stress tests. Map critical suppliers’ feedstock exposure, financial resilience and geopolitical risk, then develop two alternative sourcing plans per major spending line within 90 days.

- Invest selectively in grade flexibility. Prioritize modest retrofit projects that enable switching between commodity and specialty grades; the option value is often greater than the immediate NPV of conversion capex.

- Prepare regulatory playbooks. Build a rapid response capability for trade investigations, including documentation templates, legal contingency funding and PR messaging to keep operations resilient during proceedings.

- Evaluate opportunistic M&A. Use the next 12–18 months to target assets that fill strategic gaps — secure feedstock, add specialty capacity or expand downstream conversion — while pricing in potential remedial tariffs.

- Embed sustainability as a commercial lever. Accelerate traceability and LCA investments to win preferred supplier status with textile brands and pharmaceutical buyers; this can be a differentiator that commands price premia or preferred allocation.

Conclusion — the decision window in 2026

2026 presents a window where tactical moves — capacity reallocation, contract structure changes, and targeted capex — will deliver disproportionate strategic advantage. The dissolving pulp market’s steady baseline growth masks episodic supply shocks and regulatory events that can reprice risk and opportunity rapidly. Executives who combine rigorous supplier analytics, flexible production options and proactive regulatory playbooks will be best positioned to capture margin and secure supply.

PW Consulting’s full Dissolving Pulp Market report supplies the granular models, supplier scorecards, scenario tests and contract templates required to operationalize the priorities above. Access the full dataset and strategic playbooks via the report portal to convert this briefing’s insights into 2026 actions and measurable outcomes.

For detailed analysis of this topic, please visit the official page:Dissolving Pulp Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com