PW Consulting: Acrolein Market Set to Reach USD 1,347M by 2032

Other |

2026-07-12 06:15:07

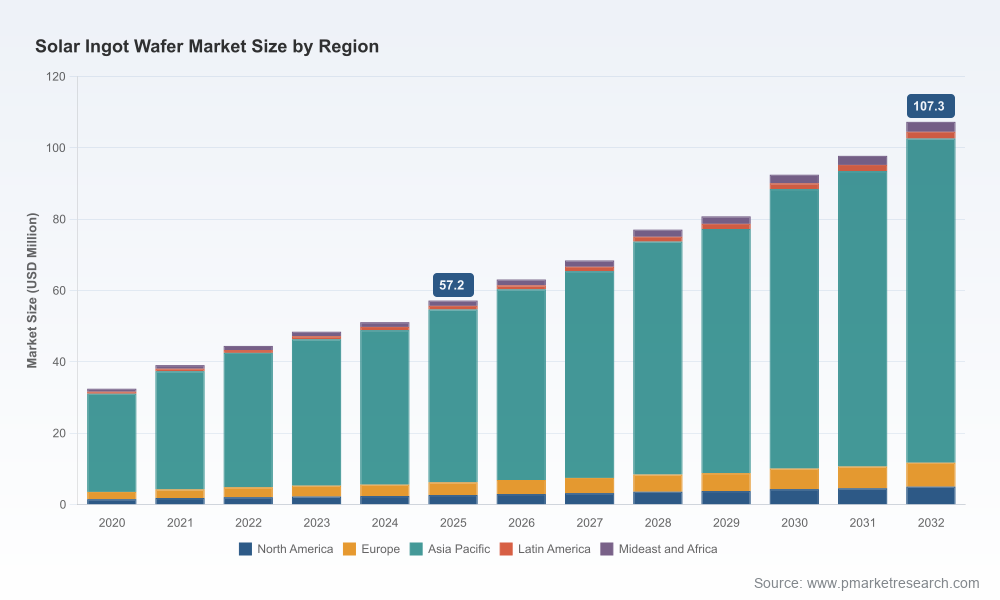

As the solar value chain accelerates into a new phase of scale and policy-driven localization, the solar ingot and wafer segment emerges as a strategic choke point for module makers, system integrators and national industrial strategies. Our PW Consulting base-year analysis (2025) and detailed forecasts through 2032 show the market continuing a robust expansion, growing at a compound annual growth rate (CAGR) of 9.39% across the 2026–2032 forecast window. From a measured USD market size in 2025, the industry is projected to roughly double by 2032, a trajectory that has immediate implications for capital allocation, technology choices and supply‑chain architecture in 2026.

Solar Ingot Wafer Market

Timing for capacity investment: The market’s near‑term momentum creates a narrow window to secure brownfield sites, equipment lead times and engineering talent. Delays in 2026 can shift project economics materially given rising input costs and policy windows for incentives.

Solar Ingot Wafer Market

Policy arbitrage and localization: Multiple government programs and trade measures are reshaping where ingots and wafers are produced and consumed. Notable incentives — including an Advanced Manufacturing Investment Tax Credit in the U.S. and substantial capital subsidies in major emerging markets — change the calculus on greenfield versus contract manufacturing and should be factored into all 2026 capex decisions.

Solar Ingot Wafer Market

Technology and product premiuming: Premium wafer types and next‑generation ingot processes command price differentials and margin uplift. With N‑type wafer supply tightening and price pressure evident early in 2026, players must choose between volume-driven commodity strategies and higher-margin differentiated pathways.

Supply resilience and trade risk: Escalating tariffs and origin restrictions on Chinese‑origin materials mean procurement strategies must now bake in scenarios for material diversion, reshoring and multi‑sourcing — all decisions that should be locked in during 2026 planning cycles.

Market scale and growth: After steady growth through the early 2020s, the industry’s structural expansion in 2026 is supported by accelerating downstream demand and capacity additions across North America, Europe, and Asia. Our forecast shows the market expanding materially beyond the 2025 base, reinforcing the need for strategic positioning this year.

Cost structure pressures: Conventional wafering processes still suffer significant silicon loss — industry analysis attributes as much as 40–45% silicon kerf loss to wire‑saw methods — which inflates material and labor components of cost. This dynamic makes investments in kerf‑reduction or kerfless technologies an economically urgent consideration.

Incentives and trade policy: The enactment of a 25% manufacturing investment tax credit in the U.S. (applied retroactively) and generous capital subsidies in markets like India create temporal arbitrage: facilities brought online or committed in 2026 can access outsized economics that materially improve IRRs. Conversely, tariffs approaching mid‑double digits on certain origins mean that supply strategies optimized in 2026 must internalize non‑linear cost shocks.

Raw material tightness and price signals: Early 2026 witnessed double‑digit upward movements in premium‑type wafer pricing — a clear signal of constrained high‑efficiency wafer supply relative to demand. Buyers and investors must interpret these signals as both margin opportunity and supply risk when negotiating contracts this year.

The ingot and wafer market exhibits a concentrated structure at the top: the combined share of the three largest firms and the top five producers remains meaningful, indicating a competitive dynamic where scale, purity expertise and integrated supply chains matter. This concentration changes how new entrants and downstream buyers should engage incumbents in 2026 — competition is less about price alone and more about guaranteed throughput, quality continuity and strategic alignment with national policies.

Technology and purity leaders: Long‑established silicon specialists headquartered in Japan, Germany and Taiwan continue to dominate high‑purity monocrystalline supply, leveraging decades of process IP. These firms remain the first port of call for high‑reliability applications.

Integrated Chinese players: A cadre of vertically integrated groups has moved to control polysilicon through wafer output, enabling cost optimization and faster scale‑up. Their strategic response to trade barriers and global demand is a core 2026 risk to model.

Specialist innovators and regional players: Firms focused on n‑type wafers and specific product lines are increasingly relevant for technology transition strategies. New capacity announcements and regional expansions underscore a bifurcated market where local scale and product differentiation coexist.

Greenfield and brownfield capacity moves: Regionally significant add‑ons and new facilities have started construction or ramped up production, altering supply geography and logistics. These actions matter for short‑term availability and long‑term pricing dynamics.

Large industrial investments: Strategic capital approvals in key emerging markets signal intent to localize ingot‑wafer manufacturing and capture downstream value; such moves unlock subsidy windows and create regional competition for procurement spend.

Price and material tightness for premium wafers: Visible price inflation for advanced wafer types is already influencing module BOMs and the relative economics of n‑type adoption versus incumbent choices.

Our full Solar Ingot & Wafer Market study is built for executives, investors and procurement leaders who must make binding decisions in 2026. Highlights include:

Comprehensive market sizing and a transparent forecasting methodology, with scenario variants that isolate policy, raw‑material and technology adoption sensitivities.

Cost‑curve and breakeven modelling that decomposes capital, energy, silicon input and labor under alternative process routes (wire saw, diamond wire, kerfless).

Trade‑policy impact matrices that quantify the earnings and margin impacts of tariff scenarios, incentive uptake and localization policies by region.

Supplier benchmarking: qualitative and quantitative vendor dossiers, operational KPIs, capacity roadmaps and a deal‑readiness checklist for offtake, tolling and JV structures.

Investment and M&A playbooks: valuation ranges, due diligence templates and integration risk maps for buyers considering vertical integration or bolt‑on capacity.

Procurement and risk mitigation tools: suggested hedge instruments, contract clauses and inventory strategies to manage price volatility in premium wafers and polysilicon.

Prioritize option diversity: Lock optionality into greenfield timelines and equipment orders to capture investment tax credits or subsidies without overcommitting to a single location.

Negotiate strategic offtakes: For buyers, early multi‑year offtake agreements with flexible location and origin clauses are the most effective hedge against tariff and price shocks.

Invest selectively in kerf‑reduction: Where economics permit, pilot kerfless or high‑yield wafering processes to lower silicon footprint and reduce exposure to silicon price swings and labor intensity.

Capitalize on premium wafer scarcity: Developers and OEMs pursuing high‑efficiency module roadmaps should secure allocations of advanced wafer types now; late participation will reduce bargaining leverage and increase BOM risk.

Model policy windows explicitly: Build financial models that capture retroactive tax credits and direct capital subsidies — the delta can flip feasibility analyses for 2026 investments.

The ingot and wafer segment is transitioning from a commodity supply pool into a policy‑sensitive, technology‑differentiated market where early movers capture the most valuable positions. With a solid growth trajectory underpinning the segment and clear policy levers altering project economics, 2026 is the year when strategic choices become binding. Companies that integrate supply‑chain resilience, technological optionality and policy‑aware investment timing will convert market expansion into durable competitive advantage.

PW Consulting’s full report delivers the granular data, regional forecasts and company financials necessary to operationalize the strategies outlined above. This preview intentionally omits detailed segment tables and regional/application share breakdowns to preserve the strategic utility of the complete study. Visit our report page to access the full dataset, model files and an executive briefing tailored to your 2026 decision calendar.

For detailed analysis of this topic, please visit the official page:Solar Ingot Wafer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com