Circumferential Abdominoplasty in Dubai Results Guide

Health |

2026-06-25 06:56:59

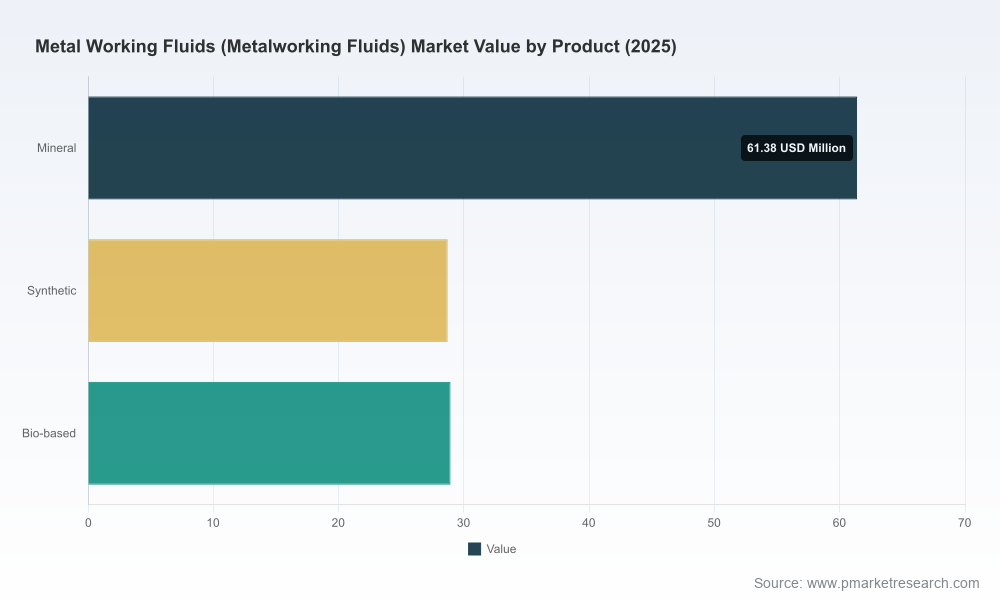

As manufacturers and chemical suppliers reassess priorities in 2026, Metalworking Fluids (MWF) remain a deceptively strategic product class: low-margin on the surface but mission-critical to productivity, part quality, worker safety and environmental compliance. Our research — built on a 2020–2025 historical baseline with a 2026–2032 forecast horizon — shows the global MWF market continuing to expand at a steady compound annual growth rate (CAGR) of 4.8%. From an estimated market of roughly USD 95 million in 2020, the industry reached about USD 119 million in our 2025 base year and is projected to approach USD 165 million by 2032. That trajectory underpins a suite of commercial decisions for 2026: from R&D prioritization and go‑to‑market moves to raw‑material hedging and targeted M&A.

Metal Working Fluids (Metalworking Fluids) Market

Strategic focus: The MWF category sits at the intersection of operational performance and regulatory exposure. Small formulation choices ripple through tool life, throughput, occupational health, and supplier economics. Our analysis converts those linkages into executable options for executives who must choose where to invest scarce R&D, capex and procurement dollars in 2026.

Metal Working Fluids (Metalworking Fluids) Market

Risk framing: The industry faces simultaneous supply‑side and regulatory shocks in 2026 — from base‑oil constraints to evolving restrictions on legacy chemistries — that will reconfigure sourcing, pricing and product portfolios. This study maps risk tolerance to specific commercial levers.

Metal Working Fluids (Metalworking Fluids) Market

Competitive positioning: Market concentration is meaningful but not prohibitive — the top three firms account for roughly a third of the industry and the top five, under half. That structure creates space for differentiated plays: technology leadership, niche high‑performance formulations, and customer intimacy at scale.

The macro picture is unambiguous: demand for metalworking fluids is recovering and compounding. After the 2020–2025 period in which the market expanded to our 2025 base, continued industrialization in targeted end‑markets and incremental adoption of higher‑value, synthetic and bio‑based formulations support growth through 2032. The projected CAGR of 4.8% reflects a mixed environment — persistent replacement demand and sporadic green premium adoption offset by regulatory headwinds and raw material pressure. For planners in 2026, the implication is clear: scale matters, but so does the ability to pivot portfolio mix toward higher‑value, lower‑regulatory‑risk formulations.

Regulatory acceleration: 2025–2026 saw multiple regulatory developments that directly affect formulation choices. Notable items include updates to regional VOC limits, intensified scrutiny of formaldehyde and certain chlorinated additives, and PFAS risk‑management discussions that are now appearing in industry committee agendas. These changes create both compliance costs and opportunity windows for early movers who can certify lower‑risk products.

Raw‑material volatility: Independent analysis and industry reports indicate a worsening base‑oil supply situation entering 2026. That squeeze will exert upward pressure on ingredient costs and potentially force formulators to substitute or reformulate. Suppliers with secure feedstock access or advanced additive engineering will enjoy a durable margin advantage.

Technology and performance innovation: Recent product introductions—from established majors and specialist formulators alike—signal a bifurcation of the market into commodity mineral oils and performance‑driven synthetic/neo‑synthetic or bio‑compatible fluids. Innovations focus on tool life extension, sump longevity, multi‑metal compatibility, and lower tox profiles — attributes that buyers in aerospace, automotive and precision engineering increasingly prioritize.

Channel and service differentiation: Beyond product chemistry, customers are buying trust: on‑site fluid management, recycling services, monitoring and data‑enabled dosing systems. Vendors that pair chemical portfolios with lifecycle services will lock in longer contracts and offset price erosion.

The competitive field comprises global majors, regional specialists and additive suppliers. Industry stalwarts and integrated oil companies continue to leverage scale and distribution; precision formulators and niche players compete on technical differentiation and regulatory positioning. Key firms featured in our review include global oil and chemical majors and specialized solution providers across Europe, North America and Asia — reflecting both legacy strengths and emergent capability sets.

Major integrated suppliers maintain reach, formulation breadth and access to base oils and additives — a tactical advantage during raw‑material constraint periods.

Specialists and independent formulators are gaining share in high‑value segments through product innovations that promise extended tool life and reduced occupational exposure.

Additive houses and chemical technology firms are pivotal: their capability to deliver multifunctional packages (corrosion control, anti‑microbial, foam suppression, biodegradability) determines the pace of portfolio migration.

Recent market developments underline these shifts. In 2025 some major suppliers launched eco‑oriented lines and next‑generation emulsions catering to aerospace and multi‑metal machining. Other independent vendors introduced neo‑synthetic water‑soluble formulations targeting harder alloys and extended sump life. Such moves illustrate how product announcements are being used to pre‑empt regulation, command price premiums and deepen application‑level partnerships.

Procurement and supply‑risk: Treat base oil constraints as a top procurement risk for 2026. Actions: diversify feedstock contracts, negotiate formula‑specific clauses, and secure strategic safety stock for critical SKUs. Consider long‑term supply agreements with additive partners whose products are difficult to substitute.

Product portfolio: Segment your portfolio into “must‑have” compliance‑safe formulations and “value‑add” high‑performance fluids. Move quickly to reformulate products that are likely to be affected by the latest regulatory trajectories; pre‑emptive reformulation costs will be lower than post‑regulatory redesign.

R&D prioritization: Invest in low‑tox, bio‑compatible and neo‑synthetic chemistries that deliver measurable machining ROI (tool life, cycle time, surface finish). Prioritize cross‑functional validation in collaboration with key OEMs and tier‑1 customers to accelerate adoption.

Commercial model: Embed fluid‑management services to increase customer switching costs and create recurring revenue streams. Service bundles — monitoring, sump maintenance, and recycling — are a lever to protect margins in a commoditizing environment.

M&A and partnerships: Use M&A to acquire specialized chemistries or regional access where you lack scale. Target assets that provide regulatory‑compliant formulations, unique additive IP, or on‑site service capabilities rather than volume alone.

Pricing and contracting: Move from spot pricing to value‑based contracting where formulation performance is explicitly linked to customer KPIs (e.g., tool life improvement). That enables price differentiation even as raw‑material costs rise.

Regulatory preparedness: Build a regulatory horizon‑scanning function that maps upcoming rules to product portfolios and timeframes. Early engagement with industry associations and regional regulators can shape compliance timelines and create lobbying leverage.

Market sizing and validated forecasts (2020–2032) with scenario analysis calibrated to regulatory and raw‑material shocks.

Supply‑chain stress tests and procurement playbooks tailored for 2026‑specific base‑oil risk scenarios.

Regulatory impact matrices mapping likely policy outcomes to formulations, timelines and cost implications.

Competitive profiles and capability maps for leading manufacturers and additives suppliers, including go‑to‑market strengths and technical differentiators.

Commercial templates: pricing constructs, service bundle frameworks, and R&D prioritization rubrics to accelerate time‑to‑value.

Deal‑flow guidance for M&A and partnership sourcing, with diligence checklists focused on IP, compliance readiness and service execution.

Case studies of successful product launches and adoption strategies that illustrate how suppliers translated chemistry advances into commercial wins.

For CEOs and business unit leaders: use the report to align capital allocation — target acquisitions that buy regulatory‑safe chemistry and service capability rather than low‑value volume. For heads of procurement: the scenario‑based supply‑risk playbooks provide a concrete negotiation posture to protect margins. For R&D and product teams: prioritize reformulation and third‑party validation with strategic customers to accelerate acceptance of higher‑value fluids. For sales and commercial teams: adopt outcome‑based contracting tied to measurable machining KPIs.

The Metalworking Fluids market in 2026 is not a static commodity arena. It is a battleground where chemistry, service, regulatory foresight and supply‑chain resilience combine to produce durable competitive advantage. With a mid‑single‑digit CAGR and meaningful concentration among market leaders, there is room both for scale plays and targeted niche strategies — but timing matters. Companies that act now to secure feedstock, reformulate ahead of regulation, and bundle services with chemical offerings will capture the disproportionately large value that flows to first movers.

PW Consulting’s full market study translates this diagnosis into a step‑by‑step operational blueprint. For executives who need to make decisive 2026 bets — on product portfolios, M&A, or procurement strategy — the full report provides the granular evidence and playbooks to move from intent to impact.

For detailed analysis of this topic, please visit the official page:Metal Working Fluids (Metalworking Fluids) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com