https://arthrovit-arthritis-pain-relief-cream-israel.lovable.app/

Art |

2026-06-02 17:14:42

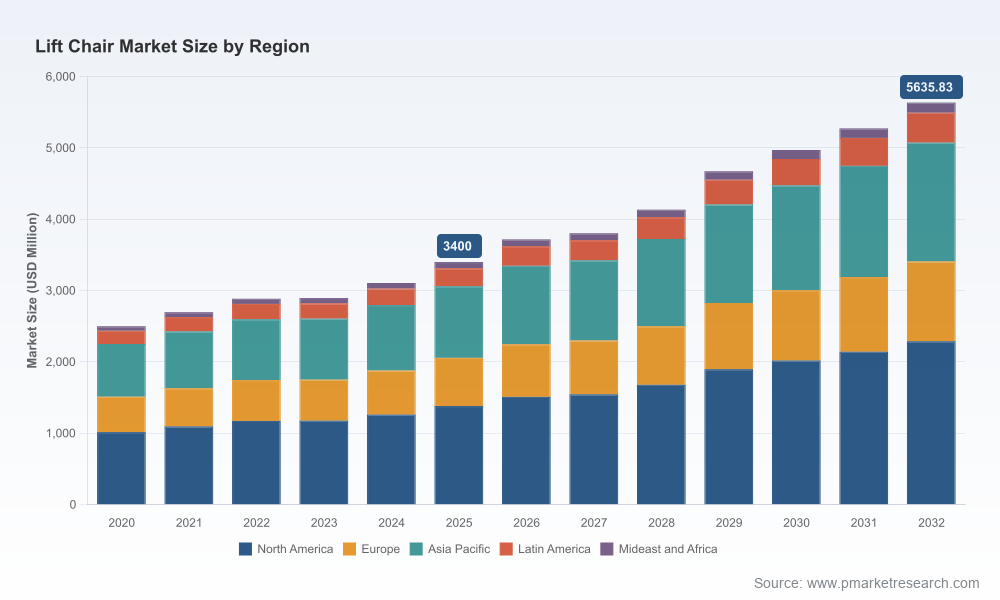

As PW Consulting’s senior industry analyst, I present a strategic introduction to our Lift Chair Market study — a practical guide tailored for executives making high-stakes resource, product, and M&A choices in 2026. The global lift chair market (base year 2025) stood at approximately USD 3,400 Million and, under the scenarios modeled in this report, grows at a compound annual growth rate of 7.5% across the 2026–2032 forecast window, reaching roughly USD 5,636 Million by 2032. Historical performance (our 2020–2025 series) demonstrates resilience through episodic supply shocks and evolving reimbursement rules.

Lift Chair Market

This study is intentionally operational. It blends quantitative forecasting with executable tools that your management team can apply immediately:

Lift Chair Market

The competitive architecture combines legacy furniture incumbents with specialized mobility manufacturers. The report profiles the leading firms, their strategic DNA, and tactical moves you should watch in 2026:

Lift Chair Market

Recent developments underscore the pace of competitive response: Golden Technologies shortened lead times and broadened model sizes in early 2026; UltraComfort received recognition in consumer rankings; Pride expanded domestic manufacturing capacity to tighten control on quality and throughput. These moves matter because they alter the timing and probability of winning dealer and institutional contracts.

Regulatory classification and reimbursement rules alter effective prices, sales cycles, and required clinical documentation. In key markets, motorized lift mechanisms are reimbursable as durable medical equipment under Medicare Part B — but only the lifting device component and only when prescribed and provided by an enrolled DME supplier. Some vendors market chairs as FDA Class II devices when positioned as aiding persons with disabilities, which has implications for pre-market controls, labeling, and post-market surveillance. For product teams, this means aligning product claims, evidence generation, and supplier enrollment to enable a covered pathway where appropriate, while also optimizing direct-to-consumer propositions for non‑reimbursable channels.

Lift chairs are engineered products whose BOMs include precision motors, linkages, and structural steel. These inputs create pinch points — motor lead times, heat-treated steel supply, and electronics/control modules. Our analysis highlights three tactical moves that materially improve outcomes:

Demographics and changing care models are the primary demand drivers. An aging population, broader home‑healthcare adoption, and increased clinical recognition of mobility-related quality-of-life gains create structural tailwinds. At the same time, consumer expectations have shifted: ergonomics, integrated wellness features (heating, massage), and easy serviceability now factor into purchase decisions alongside price and reimbursement eligibility. Successful product strategies in 2026 will balance clinical-grade durability for DME channels with lifestyle-oriented variants for direct retail and e‑commerce.

To preserve strategic value for subscribers, this brief intentionally omits granular regional splits, application-level shares, and line-item revenue breakdowns. The full study contains detailed regional and application segmentation, SKU-level forecasts, and 10-year rolling scenarios that you can download or license. Those micro datasets are where operational teams translate strategy into inventory plans, sales targets, and run-rate budgets.

By 2026, lift chairs sit at the intersection of clinical utility, consumer lifestyle, and mechanical engineering. The sector’s projected mid-single-digit-plus growth and fragmented competitive structure reward focused investment in regulatory strategy, supply-chain resilience, and product differentiation. PW Consulting’s Lift Chair Market study translates macro forecasts into executable initiatives — from SKU rationalization and supplier contracts to channel redesign and M&A targets. For leaders seeking to convert growth projections into measurable commercial outcomes, the full report and our tailored advisory engagements provide the models, benchmarks, and decision frameworks you’ll need.

To obtain the granular regional, application, and SKU-level forecasts and to explore a custom briefing or scenario workshop, please visit the report page or contact PW Consulting’s Lifecare & Mobility practice. Our advisory team will help you convert the report’s insights into a prioritized 2026 action plan.

For detailed analysis of this topic, please visit the official page:Lift Chair Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com