A Practical Approach to Hazard Identification and Risk Control

Other |

2026-04-01 09:49:00

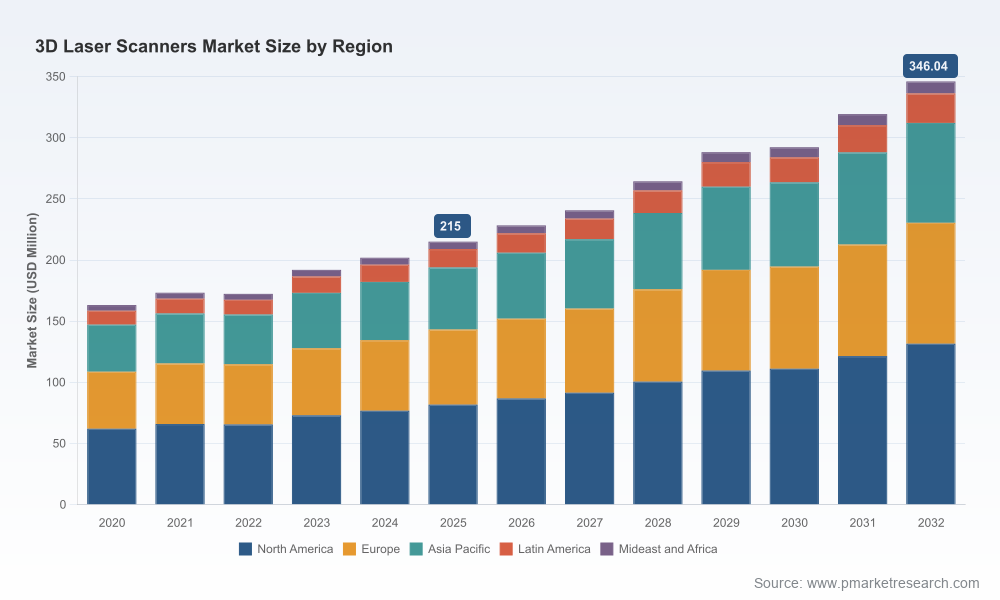

PW Consulting presents a concise, decision-focused introduction to our full 3D Laser Scanners Market study (base year 2025). This briefing synthesizes the market trajectory, competitive dynamics, regulatory inflection points, and the practical, executable intelligence that will matter to procurement leaders, program managers, and C-suite sponsors planning investments in 2026. The global market reached a base-year valuation of USD 215.0 Million (USD, Million), rebounding after mid-cycle volatility, and PW Consulting’s forecast models project a compound annual growth rate (CAGR) of 6.98% through the 2026–2032 horizon, with the market approaching roughly USD 346 Million by 2032. The full report contains the detailed segment-level tables, vendor scorecards, and proprietary models (access details at the end). This note intentionally emphasizes strategic implications while withholding granular split figures to guide readers to the full dataset.

3D Laser Scanners Market

Procurement timing: Many capital equipment cycles and software contracts initiated in 2024–2025 reach renewal or expansion in 2026. Our study indicates optimal windows for negotiating system-plus-service bundles and multi-year calibration agreements.

3D Laser Scanners Market

Digital transformation alignment: 3D laser scanning is now a foundational input to digital twin, BIM, PLM and MRO processes. Selecting scanning technologies with assured data fidelity and integration paths materially reduces integration costs downstream.

3D Laser Scanners Market

Regulatory compliance and forensics: New standards and guidelines (notably OSAC 2025-N-0022 and updated ISO metrology protocols) are already shaping procurement specs for forensic, infrastructure, and metrology-grade use cases; the report maps compliance requirements to vendor capabilities.

Risk management and TCO: Beyond sticker price, labor, data processing, calibration, and long-term software maintenance dominate total cost of ownership. Our models isolate those drivers and show where marginal spend delivers outsized operational value.

The 3D laser scanners market has moved from early adopter pockets into a broader, multiprofile demand base. Between 2020 and 2025 the market experienced episodic shifts—supply-chain and macro headwinds in some years, followed by accelerated adoption in construction, industrial inspection, and reverse engineering. Our forecast (CAGR 6.98% over 2026–2032) reflects persistent demand across use cases: high-accuracy metrology for manufacturing quality control, mobile and airborne LiDAR for infrastructure and topographic mapping, and handheld systems for inspection and reverse engineering.

Key structural drivers include:

Automation and Industry 4.0: Manufacturers require rapid, in-line and off-line capture for inspection and digital twin creation.

Infrastructure refresh cycles: Roads, bridges and major construction programs increasingly specify point-cloud deliverables as a contractual deliverable.

Regulatory and accreditation pressure: New and updated standards (ISO 10360-13, ISO 17123-9, VDI/VDE 2634 Part 3, and ISO/IEC 17025 accreditations) elevate the value of metrology-certified devices and accredited service providers.

Project economics: Labor intensity and project complexity remain primary drivers of scanning project budgets — larger, more complex sites disproportionately increase data collection and processing costs.

Our full study is structured as a practitioner’s playbook rather than an academic compendium. Highlights include:

Proven market-sizing methodology and a reconciled historical series (2020–2025) with transparent assumptions for 2026–2032 forecasting.

Vendor landscape and capability matrices—technical scoring across accuracy, throughput, usability, software ecosystem, and calibration support.

Procurement-ready templates: RFP language, technical acceptance test checklists, SLAs for firmware/software updates, and calibration/reverification clauses aligned to ISO standards.

Use-case ROI models and TCO calculators tailored for quality control, AEC/BIM workflows, and topographic mapping—built to be dropped into capital planning submissions.

Integration playbooks: data-format guidelines (point-cloud standards), ingestion patterns for leading CAD/BIM/PLM platforms, and sample ETL workflows for enterprise data lakes.

Compliance and accreditation roadmap: step-by-step guides to meeting OSAC and ISO metrology requirements for forensic and metrology-grade deployments.

Interactive scenario analysis: sensitivity models that show how labor rates, sample sizes, and processing choices change break-even points for handheld vs. terrestrial vs. mobile solutions.

The market combines a set of global, engineering-focused incumbents with a growing cohort of specialized handheld and prosumer suppliers. Market concentration metrics are instructive: the top three players account for roughly 24.6% of reported market share while the five largest capture approximately 26.2% — a profile consistent with a fragmented market that nevertheless contains well-defended niches for metrology and survey-grade systems.

Metrology and large-site specialists: Leica Geosystems, Hexagon, Trimble, RIEGL, and Topcon continue to dominate large-scale surveying, construction verification, and metrology applications. Their strengths are product robustness, integrated workflows, and long-standing service networks.

Industrial and CMM-integrated providers: FARO and Nikon Metrology focus on factory-floor inspection and integration with coordinate measuring systems, often pairing hardware with mature software suites and calibration services.

Handheld and portable innovators: Creaform and Artec 3D emphasize portability, metrology-grade handheld performance, and certification milestones that appeal to on-site inspection and reverse engineering teams. Recent product updates from both firms have tightened the gap between portable and fixed systems in accuracy and repeatability.

New entrants and Chinese ecosystem players: SHINING 3D, SCANOLOGY, 3DMakerpro, Revopoint and others are expanding offerings, with competitive pricing and regional support. Some recent launches target high-definition topographic scanning and prosumer workflows, forcing incumbents to respond on software and service.

Specialist airborne/mobile vendors: Zoller + Fröhlich and others continue to supply niche mobile and airborne solutions where range, scan rate, and post-processing pipelines are decisive.

Notable recent moves to watch (selected): Artec 3D’s 2026-certified refresh of Spider II improves metrology stability and optics; Creaform’s HandySCAN 3D PRO enhancements deepen ISO-compliance credentials; FARO’s firmware updates for Focus platforms improve field reliability; 3DMakerpro’s Raven LiDAR launch targets HD topographic workflows. These developments reflect parallel innovation paths: hardware refinement, metrology certification, and firmware/software ecosystems.

Define fit-for-purpose specs by use case. Avoid “one-size-fits-all” procurement. Metrology-grade QA requires devices and accredited calibration; site documentation and as-built BIM prioritize throughput and registration speed.

Operationalize standards compliance. Specify ISO and OSAC-relevant acceptance tests in contracts, and require traceable calibration and ISO/IEC 17025 accreditation for critical use cases.

Price beyond capex. Build project-level TCO models that include labor for capture and post-processing, cloud storage and processing, and periodic recalibration. Our calculators show these often eclipse hardware cost over a three-to-five year lifecycle.

Prioritize software ecosystems and data pipelines. Vendor differentiation is increasingly driven by point-cloud processing, automated feature extraction, and upstream integration with CAD/BIM/PLM.

Run a controlled pilot. Use a staged procurement with a performance gate—assess fidelity, throughput, calibration drift, and operational ergonomics before scaling purchases.

Lock in services: negotiate firmware maintenance windows, calibration SLAs, and training packages. With firmware and certification activity accelerating, ongoing support materially affects uptime and data quality.

Consider strategic partnerships. For organizations building internal capabilities, partnering with a metrology lab or a vendor offering calibration-as-a-service can shorten time-to-compliance.

Commoditization pressure for lower-tier handheld systems could compress margins and shift competition to software and services.

Supply-chain volatility and semiconductor shortages remain wildcard factors for high-end platforms.

Regulatory shifts — especially in forensic and public-safety applications — can raise compliance costs and change acceptable device lists rapidly.

Interoperability challenges across point-cloud formats and processing stacks can create hidden integration costs; insist on open formats and demonstrated ingestion pipelines.

This briefing surfaces the strategic implications of the 3D Laser Scanners market and the practical assets your team can use to make procurement, program, and portfolio decisions in 2026. The full PW Consulting report contains the complete segmentation tables, regional and application splits, downloadable RFP templates, vendor scorecards, and our interactive scenario models. To review the detailed segment-level data and obtain the vendor benchmarking matrices and calculators, please visit the PW Consulting report landing page or contact our advisory team for a guided walk-through and a complimentary extract tailored to your use case.

PW Consulting — translating market data into executable strategy for the era of precise, digital capture.

For detailed analysis of this topic, please visit the official page:3D Laser Scanners Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com