High Voltage Cables Market — Strategic Outlook for 2026 Decision-Making

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present this forward-looking primer to accompany our new High Voltage Cables Market study. This piece is written as a strategic “preview”: it demonstrates the analytical depth that underpins our full report while deliberately withholding core segmentation tables and granular market slices that are reserved for subscribers. The goal is simple — equip executives with the context and decision frameworks they need for 2026, and show why the full dataset is essential before committing capital, supply contracts, or M&A moves.

High Voltage Cables Market

Macro trajectory: a compact market with sustained expansion

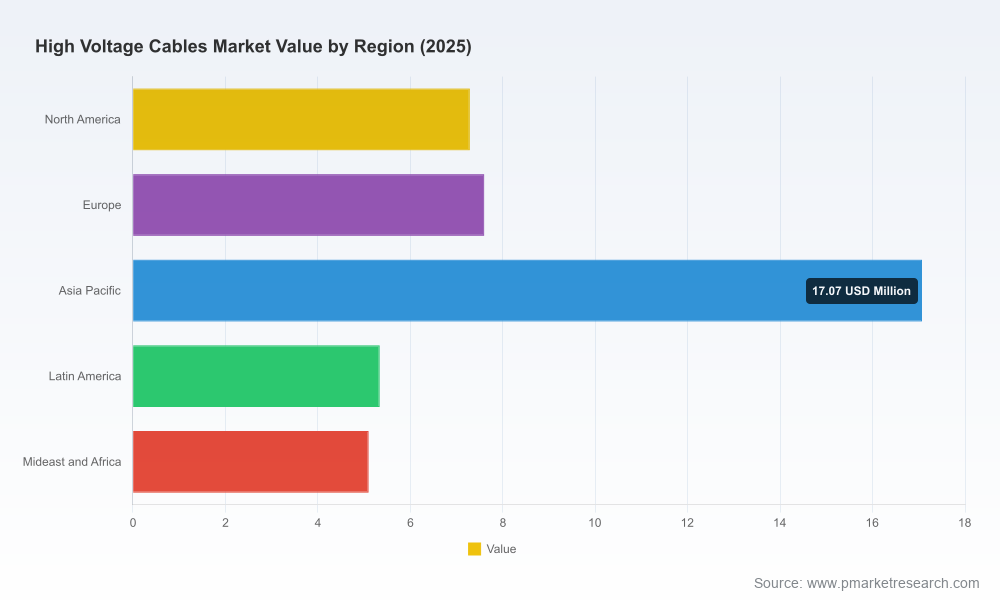

The high voltage cables market has moved from a smaller base into a phase of steady expansion driven by large HVDC and HVAC transmission projects, offshore wind connections, and grid reinforcement programmes. On a consolidated basis, the market expanded from roughly USD 25.6 million in 2020 to USD 42.4 million in our base year of 2025. Our forecast horizon (2026–2032) projects continued growth at a compound annual growth rate (CAGR) of about 6.08%, reaching a market size in the low‑sixty millions by 2032 under the baseline scenario.

High Voltage Cables Market

Two macro takeaways for 2026: first, growth is persistent rather than explosive — implying sustained order books and predictable revenue streams for established suppliers. Second, the market remains concentrated: the top three players account for a plurality of supply, and the top five for slightly more than half of the industry’s revenue. That concentration has practical consequences for procurement, contracting dynamics, and competitive entry strategies.

High Voltage Cables Market

Dynamics shaping near‑term strategy

- Project-led demand: Large national and transnational transmission projects — including offshore grid multipliers and interconnectors — are the primary demand drivers. These programmes create multi‑year procurement windows and lumpier demand profiles that favour suppliers with project execution scale.

- Raw material and input cost volatility: Copper and other conductors remain a key cost driver. For example, copper electric wire prices were observed near USD 416 per thousand linear feet in April 2026, a level that materially impacts margin planning, indexation clauses, and hedging strategies for long delivery contracts.

- Policy and regulatory accelerants: Large capex proposals and coordinated TSO initiatives have elevated the visibility of HVDC investment programmes. Notable examples include a major HVDC upgrade proposal submitted in late 2025 in a developed market context and a coalition of European TSOs that advanced an offshore cable infrastructure initiative in April 2026 — both signals that systemic transmission buildouts will underpin demand through the decade.

- Technology and scope creep: As projects scale to higher voltage levels and longer subsea crossings, technical risk migrates from raw conductor supply to insulation systems, jointing technologies, and installation capabilities. Execution risk increasingly differentiates vendors.

Competitive landscape — capabilities matter more than cost alone

Across major procurements in 2025–2026, the competitive field has consolidated around a handful of suppliers that combine manufacturing scale, project engineering, and specialized installation competencies. Recent company developments illustrate where capability investment is concentrated and where marginal advantage will be won.

- Nexans (Paris, France): Executed a world‑record subsea installation in January 2026 — a 500 kV HVDC subsea cable laid at depths over 2,150 meters for a significant interconnection project. The milestone highlights Nexans’ ability to handle extreme subsea conditions and complex logistics.

- Prysmian Group (Milan, Italy): Continued focus on high‑voltage HVAC solutions tailored to floating offshore wind platforms, demonstrating a product strategy that serves renewables‑driven transmission needs where dynamic mechanical performance matters.

- NKT A/S (Copenhagen, Denmark): In March 2026 NKT secured a major HVDC power cable system contract that stands as the largest single cable project award in its history, signalling the firm’s successful escalation into large interconnector projects and reinforcing its execution credentials.

- Sumitomo Electric Industries Ltd (Tokyo, Japan): Secured a strategic 525 kV HVDC contract in late 2025 for a high‑profile link, reflecting the continued demand for ultra‑high voltage systems and the premium placed on proven high‑voltage experience.

- LS Cable & System Ltd (Seoul, South Korea): Active on high‑voltage HVDC programmes with multi‑project exposure in regional grids, underlining the global spread of capable suppliers beyond the European incumbents.

- Regional specialists (examples include Tratos, Finolex, Cable Corporation of India): These firms are increasingly focused on domestic transmission needs and renewables integration plays, occupying niches where local certification, cost discipline, and speed to market matter.

Strategic implications: buyers should evaluate vendors on execution history for analogous environments (deepwater, long subsea crossings, high‑voltage shore crossings), financial flexibility to manage raw material swings, and integrated installation capabilities (vessels, jointing teams, long‑lead items). Sellers should prioritize demonstrable project references, de‑risking clauses, and supply chain resilience.

What the PW Consulting report delivers — practical, decision‑grade outputs

Our full study is designed as an operational playbook for strategy, procurement, and corporate development teams in 2026. Highlights include:

- Proprietary market sizing and a validated demand schedule across 2020–2032 with base‑year normalization (2025) and scenario variants for high and low project activity.

- Forward cost modelling that isolates conductor, insulation, and installation cost lines and shows sensitivity to raw material indices; models are delivered in editable formats for client‑specific inputs.

- Supplier landscaping with capability scorecards that go beyond revenue share to evaluate technical competence, submarine installation track record, manufacturing redundancy, and balance sheet strength.

- Regulatory risk matrix mapping likely policy windows and permitting bottlenecks by project type (interconnectors, offshore wind, domestic reinforcement), along with recommended engagement tactics for TSOs and regulators.

- M&A and JV playbooks tailored for both strategic and financial acquirers, including target selection filters, integration checklists, and pricing heuristics under varying market growth scenarios.

- Procurement templates and contract clauses (indexation, milestone payments, LTIs, liquidated damages) aligned to mitigate copper volatility and installation schedule risk.

- Scenario planning modules that model the impact of coordinated grid initiatives and concentrated supplier market shares on pricing leverage and time‑to‑market.

Each deliverable is accompanied by a concise recommendation memo that translates insight into the next‑quarter actions our clients can take.

How executives should use this intelligence in 2026

- Procurement strategy: Use the report’s supplier scorecards and cost models to shift from lowest‑price awarding towards balanced scorecards that internalize execution risk and long‑term O&M exposure.

- Contract design: Defend margins by incorporating raw material pass‑through mechanisms and clear scope delineation for subsea/land transitions; the April 2026 copper price demonstrates the need for flexible indexation.

- Capex timing: Align project sanctioning with forecasted supply‑chain lead times; the report’s demand schedule identifies likely window clustering across 2026–2032 so that factory capacity and vessel bookings can be secured in advance.

- Partnerships and JV formation: Where incumbents dominate on large HVDC builds, consider localized JV structures to access installation capacity and regulatory goodwill while sharing technical risk.

- M&A and investment screening: Use the report’s M&A playbook to assess targets for complementary capabilities (e.g., jointing tech, specialized insulation, or fleet ownership) rather than solely chasing revenue scale.

Why the full report matters: bridging insight to execution

The strategic value of the complete PW Consulting study is in its combination of granular delivery risk analytics, editable cost models, and supplier capability assessments linked directly to the procurement and investment decision cycle for 2026. The preview above surfaces the forces at work — steady market growth, concentrated supply, raw material volatility, and a wave of grid and offshore projects — but the full intelligence suite is required to quantify tradeoffs, stress‑test contracts, and build execution plans that preserve margin and schedule.

If your priorities for 2026 include securing long‑lead components, negotiating multi‑year supplier frameworks, executing a targeted M&A, or staging a market entry into high‑voltage project supply, the report provides the evidence base and tactical templates to act with confidence.

Next steps

This preview is intended to orient senior teams and investment committees. For access to the full datasets, supplier scorecards, editable financial models, and bespoke advisory support, please consult the PW Consulting High Voltage Cables Market report and associated advisory offerings. The complete deliverables translate the strategic themes summarized here into executable workplans for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:High Voltage Cables Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com