Remote Data Monitoring Market: Size, Share, and Future Growth~

Other |

2026-05-07 03:33:01

As global manufacturers and automation integrators prepare capital plans and product roadmaps for 2026, understanding where the grippers market is headed — and why — is mission-critical. PW Consulting’s forthcoming Grippers Market study synthesizes five years of historical industry performance (2020–2025) with a seven‑year forecast (2026–2032), presenting a forward-looking view grounded in primary interviews, vendor benchmarking, and quantitative modelling. This preview highlights the strategic value of that research for executives, while intentionally omitting granular segment tables and regional splits to preserve the full report’s commercial value.

Grippers Market

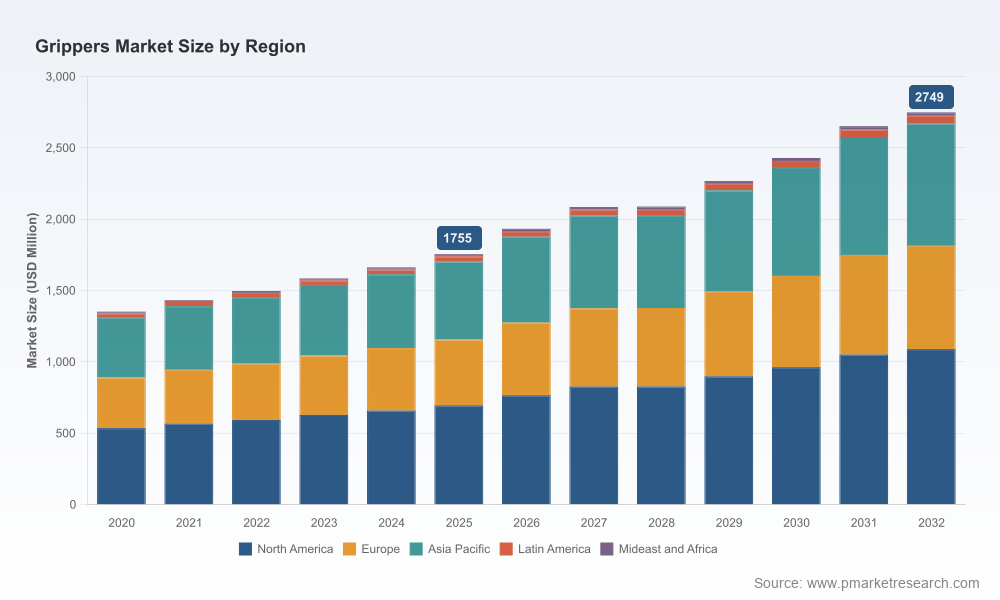

The grippers market is at an inflection point. After expanding steadily through 2020–2025, the market reached an approximate USD 1,755 million base in 2025. Our forecast projects a near-term uplift to about USD 1,933 million in 2026 and continued expansion through the 2026–2032 horizon, reaching roughly USD 2,749 million by 2032. That trajectory reflects a compound annual growth rate (CAGR) of approximately 9.4% over the forecast period — a pace that transforms mid‑market forecasts into boardroom imperatives.

Grippers Market

Two high‑level takeaways emerge from these numbers: first, demand is broad-based rather than niche, driven by converging forces across industrial automation, collaborative robotics (cobots), and sector-specific needs (e.g., food handling, electronics); second, the growth is sufficient to justify both product investment and M&A activity for incumbents and challengers who can execute fast.

Grippers Market

Labor and unit economics: Tight labor markets are a primary adoption driver. In Q3 2025, manufacturers reported an average of 4.2% of roles unfilled, with nearly a quarter of companies facing vacancy rates above 5%. That scarcity is pushing line managers to automate repetitive, ergonomically challenging tasks — the classic playground for grippers — but with new requirements for flexibility and safety.

Regulatory pressure and safety integration: Updates to ISO 10218‑2 in 2025 now include explicit guidance for end‑effector tooling and collaborative safety thresholds. For any firm deploying grippers near human workers, compliance is no longer a documentation exercise but a product design constraint: force and power limiting, risk assessments for dropped loads, and integration of safe stop behaviors must be baked into development and procurement cycles.

Technology convergence: Expect product differentiation to come from multi‑disciplinary integration — tactile sensing, force/torque feedback, soft materials for delicate handling, and plug‑and‑play interfaces for cobots. Recent launches (reported through mid‑2026) already demonstrate this trend: teachable sensors on electric parallel grippers, food‑grade adaptive silicone grippers, tactile fingertips integrated with adaptive hands, and soft vacuum grippers tailored for confectionery and food lines.

Market concentration and competitive positioning: The market exhibits moderate concentration — the top 3 vendors account for roughly 45% of market value, while the top 5 capture about 55%. That structure favors well financed incumbents for high‑volume industrial deals but leaves room for specialist entrants to capture niche value through technology or channel advantages.

The competitive field is evolving from component suppliers to systems partners. Across the established players and newer specialists, three positioning archetypes are emerging:

Modular systems leaders: Firms with deep pneumatic and electric portfolios are leveraging modularity to win integration projects where uptime, spare‑parts commonality, and serviceability drive total cost of ownership. Their advantage is in scale and distribution, especially in traditional manufacturing verticals.

Cobot‑first specialists: A distinct cluster focuses on plug‑and‑play collaborative grippers, adaptive two‑finger hands, and integrated sensor packages. These players emphasize ease of deployment and software ecosystems, targeting small‑to‑mid size automation projects and contract manufacturers seeking rapid ROI.

Application specialists: Vacuum and soft‑material gripper makers are intensifying investments into hygienic materials, tailored contact surfaces, and industry‑specific certifications (e.g., food safety). Their moat is deep application knowledge and adaptability to gentle handling challenges.

Recent product activity provides tactical signals for 2026 strategy: electric parallel grippers with teachable sensors indicate a shift toward configurable automation building blocks; adaptive food‑grade grippers show demand for hygienic, easy‑clean end‑effectors; tactile fingertips underscore that sensing is becoming mainstream rather than optional; and expanded soft gripper capacities reflect growing uptake in confectionery and other delicate goods.

Procurement and supplier strategy: Given the market’s moderate concentration, procurement teams should segment sourcing strategies by use case. For high‑volume, commodity deployments, prioritize suppliers with global service footprints and modular platforms. For high‑value or niche tasks, evaluate specialists offering integrated sensing and application‑specific materials.

R&D prioritization: Invest in force/torque integration, tactile sensing, and hygienic materials. Compliance with the 2025 ISO updates demands that new gripper designs include safety features at the mechanical and control layers; this should be a gating criterion for product roadmaps.

Go‑to‑market and channel development: For component vendors, the fastest path to growth is through system‑level partnerships with robot OEMs and integrators. For functional specialists, develop vertical playbooks (e.g., food, electronics, automotive subassembly) that quantify productivity gains and compliance benefits.

M&A and investment screening: The forecasted ~9.4% CAGR makes bolt‑on acquisitions attractive for firms seeking to augment sensor suites, soft‑material capabilities, or cobot‑friendly interfaces. Use deal screens that prioritize IP in tactile sensing, validated hygienic materials, or existing certified installations in regulated industries.

Aftermarket and service models: As gripper fleets proliferate, predictive maintenance and spare‑parts bundling become differentiators. Offer outcome‑based contracts (e.g., uptime guarantees for pick‑and‑place cells) to capture recurring revenue and deepen customer relationships.

This study is built for operators who must turn insight into action. Highlights of the full deliverable include:

Robust market sizing and forecasting model (2020–2032) with sensitivity scenarios and upside/downside cases aligned to macroeconomic and adoption variables.

Vendor scorecards and capability matrices — comparing mechanical architectures, sensing integration, software maturity, and service footprints — to support procurement shortlists and RFP design.

Detailed go‑to‑market playbooks for five priority verticals, including decision frameworks for cobot vs. industrial deployments and ROI calculators that reconcile labor substitution with capital recovery timelines.

Technology roadmaps and a 36‑month blueprint for product managers outlining prioritized features, certification requirements, and go‑to‑market timing to capture early mover advantages.

M&A heatmaps and valuation benchmarks, highlighting capability gaps attractive to strategic acquirers and private equity buyers.

Customizable implementation checklists and compliance templates aligned to the ISO 10218‑2:2025 updates, reducing integration risk and accelerating deployment approvals.

Modular system incumbents continue to leverage breadth: large manufacturers offering pneumatic and electric portfolios are doubling down on modularity and global service networks to win enterprise automation programs.

Cobot specialists are monetizing ease‑of‑use: companies focusing on plug‑and‑play grippers and tactile sensor integration are expanding into contract manufacturing and light industrial segments through embedded software ecosystems.

Application experts are monetizing domain knowledge: vacuum and soft‑gripper companies are advancing material science and hygienic designs to capture higher‑margin food and packaging opportunities.

Notable tactical moves through mid‑2026 — product launches that validate these trends — include electric grippers with teachable sensors, food‑grade adaptive hands, tactile fingertip modules, and expanded soft gripper capacities for confectionery handling. These product introductions are more than incremental updates; they represent a shift in how end‑users expect grippers to behave — safer, softer, and smarter.

For executives balancing CAPEX discipline with the need to increase automation density, the grippers market is a lever with measurable impact. A disciplined investment in sensing, compliant design, and aftermarket services can convert the forecasted market growth into sustainable margin expansion and defensible customer relationships. Conversely, delay risks commoditization of product lines and loss of channel mindshare to cobot‑native entrants and specialist application vendors.

PW Consulting’s Grippers Market study equips leaders with the data and playbooks to make these calls with confidence. Note that this preview intentionally omits granular regional and application splits and other sensitive segment tables — the full report contains those detailed models, vendor scorecards, and downloadable forecast files required to operationalize strategy.

For procurement teams, product leaders, and corporate development groups planning 2026 initiatives, the full PW Consulting Grippers Market report will convert the market’s 9.4% CAGR opportunity and the 2025 baseline into concrete projects: prioritized supplier shortlists, RFP templates, product feature roadmaps, and M&A screens. Contact PW Consulting to access the complete study and the underlying models that power executable strategies.

For detailed analysis of this topic, please visit the official page:Grippers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com