PW Consulting Report: Targeted ROS1 Inhibitors for NSCLC Poised for Rapid Expansion, Forecasted at a 14.85% CAGR

Other |

2026-07-06 14:26:08

As enterprise architectures pivot toward AI‑first workloads, hybrid multicloud fabrics, and tighter regulatory regimes, colocation has moved from an operational utility to a strategic lever. PW Consulting’s latest Colocation Market research — grounded in a 2025 base year and a seven‑year forecast horizon to 2032 — quantifies that transition and translates it into operational imperatives for 2026. This article previews the research’s strategic value, outlines the practical tools included, and highlights the competitive dynamics shaping vendor selection, capacity planning, and regulatory compliance. Core granular segment tables remain gated in the full report to preserve the “trailer” principle: this briefing demonstrates our analytical depth while directing practitioners to the full research for proprietary splits, heat maps, and contract templates.

Colocation Market

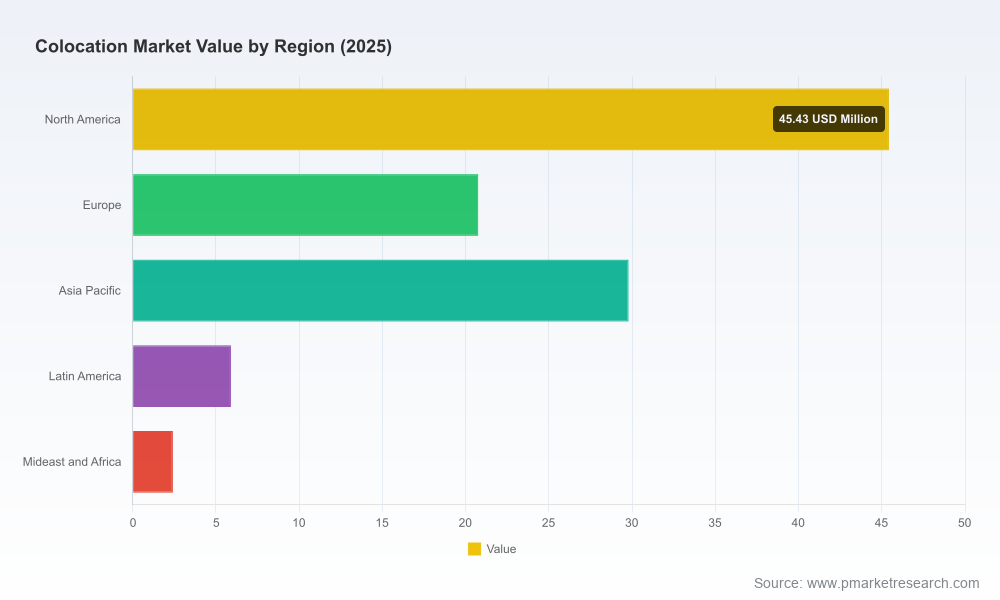

The global colocation market has more than doubled in scale over the last half‑decade, rising from roughly USD 47 million in 2020 to approximately USD 104 million in 2025 (base year).

Colocation Market

Looking forward, our forecast models project continued robust expansion, with the market tracking to roughly USD 266 million by 2032 under a compound annual growth rate (CAGR) of 14.4% through the forecast period.

Colocation Market

Market concentration is meaningful but not monopolistic: the top three providers account for a material share of capacity, and the top five capture more than half of market capacity — a structure that affects negotiation dynamics, interconnection options, and resilience strategies.

AI and high‑density compute: Hyperscale AI deployments and HPC workloads are accelerating demand for high‑density power and specialized cooling. Colocation operators that have purpose‑built racks, scalable campus designs, and proximity to fiber ecosystems are capturing disproportionate growth.

Regulatory tightening: New reporting and operational requirements are shifting the compliance burden onto operators and operators’ customers. For example, the EU’s energy efficiency recast requires larger facilities to publish PUE and water‑use metrics, and U.S. federal energy planning discussions are elevating interconnection rules for large loads — both of which affect site selection and procurement timelines.

Cost and construction constraints: U.S. construction costs for data centers remain elevated with labor availability a bottleneck; our sector analysis shows construction baselines and schedule risk that materially affect time‑to‑market for custom builds.

Energy economics and pass‑throughs: Power pricing and contractual constructs (separate pass‑throughs vs. bundled rates) have emerged as primary drivers of total cost of ownership (TCO) for rack and pod strategies. In major North American markets, power pass‑through practices lead to higher monthly per‑kW exposures than in previous cycles, changing the calculus for wholesale vs. retail engagements.

Data sovereignty and localization: Government mandates across regions are forcing regulated workloads to remain inside national borders, creating pockets of premium demand and supply stress that reward operators with local presence and certified compliance frameworks.

Executive playbook: A focused 12‑month decision roadmap for CIOs, real estate leads, and procurement teams that prioritizes RFP timing, capacity staging, and risk mitigations tied to regulatory milestones.

Market sizing and demand modeling: A reproducible demand model covering historical (2020–2025) and forecast (2026–2032) periods, with scenario runs for AI acceleration, energy‑price shocks, and localization mandates. Note: granular regional and application splits are available in the gated dataset.

Vendor selection matrix: A customizable scorecard that weights technical fit (density, latency, interconnection options), commercial terms (power pass‑through, escalation clauses), and strategic attributes (sustainability credentials, local compliance).

TCO and lifecycle costing: A configurable TCO model that lets you compare retail racks, caged solutions, wholesale shells, and owned builds across CapEx, OpEx, power, connectivity and migration costs.

Site selection and contracting playbook: Practical checklists for site due diligence, utility engagement, grid‑connection risk assessment, and a library of negotiable contract clauses and procurement timelines.

Sustainability and compliance toolkit: Templates and KPIs (PUE, WUE and other efficiency metrics), plus an impact matrix aligning regulatory deadlines to vendor readiness and contractual remedies.

Stress tests and sensitivity analyses: Portfolio‑level scenarios that simulate construction delays, power interruptions, and rapid demand spikes to quantify revenue at risk and SLA exposure.

The competitive map is diverse: hyperscale‑ready wholesale campuses sit alongside carrier‑neutral interconnection hubs and regionally focused players with regulated‑workload expertise. Several strategic archetypes have emerged, and the report profiles each with implications for partnerships and procurement:

Equinix (Redwood City, CA; equinix.com): The world’s largest carrier‑neutral interconnection platform continues to prioritize metro density and interconnection fabric, and is accelerating AI‑ready capacity while expanding into adjacent markets that require local data sovereignty controls.

Digital Realty (Austin, TX; digitalrealty.com): As a leading capacity provider and wholesale specialist, Digital Realty’s global footprint and recent Mediterranean expansion reinforce its strategy of offering enterprise‑grade shells and turnkey deployments at scale, coupled with sustainability reporting that appeals to ESG‑conscious customers.

Iron Mountain (Denver, CO; ironmountain.com): With a portfolio pitched at regulated industries and emerging hyperscale needs, Iron Mountain’s new regional campuses deliver a compliance‑forward colocation option suited to customers with strict data‑handling obligations.

QTS (Overland Park, KS; q.com): Positioning itself on AI and high‑density capacity, QTS is focusing on North American and European markets with a proposition centered on scalability and operational control.

CoreSite (Denver, CO; coresite.com): Noted for high‑density metro footprints and cloud on‑ramps, CoreSite’s thought leadership on hybrid infrastructure emphasizes the role of colocation in hybrid IT strategies.

Vantage Data Centers (Denver, CO; vantage-dc.com): Wholesale and hyperscale campuses optimized for AI and enterprise growth make Vantage a go‑to for predictable, large‑scale deployments requiring megawatt‑level commits.

CyrusOne (Washington, D.C.; cyrusone.com), Switch (Las Vegas; switch.com), NTT Global Data Centers (Tokyo; ntt.com), and ST Telemedia GDC (Singapore; sttelemedia.com): Each offers differentiated mixes of metro interconnection, regional reach, and carrier ecosystems — critical when placing latency‑sensitive or regulated workloads.

Recent market moves underscore these dynamics. In 2026, several major operators announced regional expansions and sustainability disclosures that directly affect enterprise strategy: Equinix moved into new national markets with explicit data‑sovereignty controls, Digital Realty deepened Mediterranean capacity while publishing an updated impact report, and Iron Mountain advanced its Asia‑Pacific capacity with a new campus coming online. CoreSite’s state‑of‑the‑data‑center publication reiterated colocation’s centrality in hybrid IT architectures.

Procurement timing matters: The combination of construction constraints and regulatory lead times means multi‑year procurement windows are now the default. Begin vendor RFPs and utility engagements earlier in the cycle for any project needing production capacity inside 18–36 months.

Negotiate power mechanics: With power often passed through separately and market practices varying by region, build TCO scenarios around multiple power pass‑through constructs and include contractual caps and transparency provisions.

Insist on measurable sustainability metrics: Compliance regimes increasingly require published PUE/WUE metrics. Embed reporting and audit rights into contracts to avoid post‑deployment surprises.

Design for flexibility: Hybrid approaches that blend retail colocation for latency‑sensitive workloads and wholesale shells for bulk compute optimize for both cost and speed, but they require integrated network and cross‑connect strategies.

Mitigate concentration risk: Given the market’s mid‑range concentration (top‑three and top‑five dynamics), consider multi‑vendor, multi‑region strategies for mission‑critical services to preserve bargaining power and resilience.

Our analysis synthesizes supply‑side inventories, operator filings, customer interviews, site visits, and proprietary demand models calibrated to historical spending patterns (2020–2025) and forward scenarios (2026–2032). We conduct sensitivity testing across power price shocks, construction‑delay outcomes, and accelerated AI adoption curves. To preserve client value and the report’s commercial integrity, detailed regional and application splits, interactive heat maps, and vendor scorecard templates are available exclusively in the full report package.

For 2026, the strategic imperative is clear: treat colocation as a configurable capability — one that can be scaled, optimized for cost and sustainability, and contracted to reflect regulatory and energy‑market realities. PW Consulting’s full report equips CISOs, CIOs, real‑estate VPs, and procurement leads with the models, playbooks, and vendor evaluations needed to make confident, defensible decisions. Request the full study to access the gated segmentation, detailed regional forecasts, and the vendor negotiation toolkit that turn this briefing into operational outcomes.

For detailed analysis of this topic, please visit the official page:Colocation Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com