Hot-Work Die Steels Market: Strategic Preview for 2026 Decision-Makers

As PW Consulting’s lead industry analyst, I present a concise yet strategically rich preview of our full Hot-Work Die Steels Market study. This briefing is designed to help senior executives, M&A teams, procurement leaders and technology strategists prioritize choices for 2026. It highlights the macro trajectory, structural dynamics, competitive tensions and the practical playbooks that will determine who captures value as the market moves into the next growth cycle — while withholding the granular segmentation tables and detailed numeric splits that are available in the full report.

Hot-Work Die Steels Market

Macro outlook: stable growth, structural upside

Using 2025 as the base year, the hot-work die steels market has demonstrated resilient expansion through the 2020–2025 period and enters 2026 from a position of momentum. Our topline model shows the market rising from just over USD 160 million in 2020 to roughly USD 215 million in 2025. With a compound annual growth rate of 6.98% through the 2026–2032 forecast window, the sector is expected to continue expanding meaningfully, with the 2026 level positioned above the 2025 baseline and a projected rise toward the mid-term forecast horizon.

Hot-Work Die Steels Market

That growth is not uniform: it is driven by a confluence of technology substitution in dies, higher service-life requirements from die-makers, increased use of high-performance alloy grades and selective capital investment in capacity by integrated suppliers. The macro profile—steady CAGR, moderate market size and pockets of premiumization—creates a strategic environment where operational excellence and product differentiation matter as much as scale.

Hot-Work Die Steels Market

Why this matters to 2026 corporate strategy

- Capex prioritization: With predictable topline growth and identifiable pockets of product premiumization, firms must decide whether to invest in additional melting/processing capacity, heat-treatment capabilities, or in downstream partnerships (die makers, repair networks) that increase lifetime value per ton.

- Supply-chain positioning: The raw-material needs for high-performance hot-work steels — particularly high-purity chrome, molybdenum and vanadium alloys — mean procurement strategies that secure alloy availability and quality will convert to competitive advantage.

- Regulatory and border dynamics: New carbon and trade mechanisms, tighter emission limits on specialty-steel melting, and updated international standards are reshaping where it makes sense to produce and sell hot-work steels. Firms must assess the cost of compliance across their footprint.

- R&D and product strategy: Incremental improvements in thermal conductivity, toughness under thermal cycling and resistance to heat-softening are the differentiators for next-generation die steels. Investments in metallurgy and process control yield direct ROI through higher die life and lower total operating costs for end users.

Key market dynamics shaping 2026 decisions

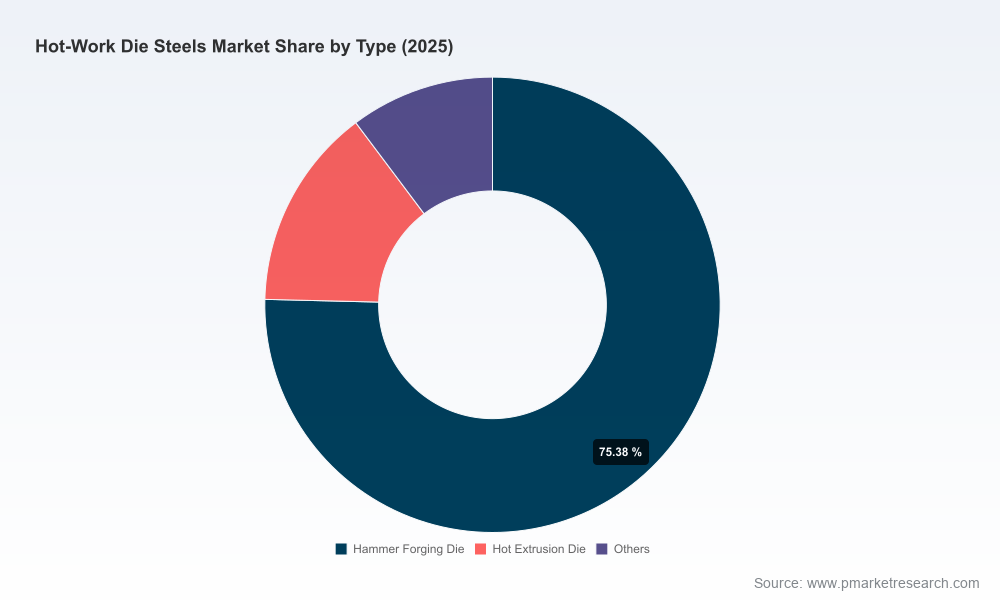

- Product premiumization vs. commoditization: The market is bifurcating. On one side, advanced grades with enhanced high-temperature properties and improved thermal management command premium pricing and longer service life. On the other, established generic grades remain cost-competitive for less demanding applications. Winning companies will manage a balanced portfolio and avoid margin erosion in the mid-market.

- Consolidation and vertical integration: Recent consolidation moves and capacity investments among European and Japanese players accelerate scale benefits and tighter downstream integration with forging and die-making operations. These actions raise the entry bar for independent smaller mills but also open partnership opportunities for specialized service providers.

- Raw-material and energy constraints: High-purity alloy inputs and emission-constrained melting processes are creating localized supply risk and cost pressure. Producers that optimize scrap blending, invest in low-carbon melting or secure long-term alloy contracts will have a visible cost advantage.

- Standards and compliance: International standards mandating impact resistance and evolving regional carbon measures are changing cost-to-serve dynamics. Companies selling into regulated markets must demonstrate process controls and traceability to retain market access.

Competitive landscape: who’s shaping the market and how

The industry comprises a mix of legacy steelmakers, specialty tool-steel houses and regional producers. Suppliers vary by degree of integration, product portfolio depth and R&D focus:

- Japanese specialty houses are notable for extremely clean metallurgy and advanced hot-work grades engineered for high-temperature strength and thermal conductivity. Their product-led differentiation makes them preferred suppliers where die life and process reliability are the primary purchase criteria.

- European premium suppliers focus on ESR/VDN processing routes and portfolio depth that emphasize premium H13 variants and specialty alloys for high-pressure die casting and forging. Strategic consolidation in Europe has recently concentrated capability and created new operational platforms.

- North American and global independent mills supply established grades with broad availability and strong service networks, particularly for die shops needing regional support and rapid lead times.

- Emerging-market producers are improving quality and scaling capacity, increasingly competing on total cost of ownership rather than only on unit price.

Recent industry moves are a clear signal of strategic direction. For example, the launch of an optimized hot-work grade by a major European producer underscores the commercialization of material innovations that extend mold life and reduce operating costs. Separately, an integrated European forging group completed a multi-company integration and injected capital into casting and heat-treatment capacity, signaling a push to control more of the value chain and capture downstream margin.

Practical, actionable contents of the full report

Our full PW Consulting study is designed as an operational playbook for 2026 decisions. Key modules include:

- Topline market sizing and a transparent forecast model (base year 2025; forecast 2026–2032) that allows scenario testing under different demand, price and input-cost trajectories.

- Segment and application analysis with buyer-intensity mapping, demand drivers and service-level expectations (note: detailed segment tables and regional splits are available in the full report).

- Supply-chain diagnostics that focus on alloy sourcing, melting routes, heat-treatment capabilities and logistics vulnerabilities, including practical mitigations and procurement contract templates.

- Regulatory impact assessment covering emission limits, carbon border frameworks and quality/standards requirements — each linked to cost-to-serve and go/no-go production scenarios by geography.

- Competitive profiles and strategic blueprints for leading suppliers, including their technology differentiators, capacity footprints and recent strategic moves (product launches, M&A, capital investments).

- Commercial playbooks for pricing, bundling, aftermarket services (repair, recoating), and product-to-service migration that increase customer stickiness.

- M&A and partnership screening frameworks that quantify value pools, integration risk and expected synergies for bolt-on and transformational deals.

- Implementation-ready roadmaps for decarbonization investments in specialty-steel melting and for upgrading heat-treatment and inspection capabilities to meet stricter standards.

Five strategic imperatives for 2026

- Prioritize alloy security: Move from spot buying to multi-year, quality-linked alloy agreements and consider backward integration for critical inputs where feasible.

- Invest selectively in premium grades: Fund R&D or JV agreements to develop coatings, tailored compositions and thermal-management solutions that demonstrably extend die life.

- Localize where regulation bites: Reassess production and sales footprints to minimize exposure to cross-border carbon tariffs and to leverage local compliance advantages.

- Capture aftermarket value: Build die repair, refurbishment and analytics services to convert one-time sales into recurring revenue streams and to gather usage data that informs next-generation alloys.

- Prepare for consolidation: Use M&A as an option strategy — secure critical capabilities (heat-treatment, ESR processing) and plug geographic gaps while keeping balance-sheet flexibility.

Risk map and mitigation

Key risks to the 2026 plan include alloy supply interruption, rapid decarbonization regulatory shifts, and disruptive technological substitutions (e.g., additive manufacturing of die components). Mitigations are pragmatic: diversify alloy sources, accelerate low-carbon investments where cost-effective, and pilot additive approaches on non-critical die components to evaluate scalability.

Next steps for leaders

If you are defining 2026 budgets, negotiating supplier contracts or assessing M&A targets, the full PW Consulting Hot-Work Die Steels Market report provides the scenario models, supplier scorecards and the practical templates you need to act. The public preview you are reading is intended to orient your priorities and highlight the strategic choices. To convert these insights into executable 90-day plans and three-year roadmaps, access the full study where we disclose the detailed segmentation, region-by-application forecasts and the proprietary supplier benchmarking that underpin our recommendations.

For executives who need a rapid, bespoke briefing: PW Consulting offers a one-day executive workshop that applies our models directly to your business case and yields prioritized actions with estimated impact on margin, CAPEX and carbon footprint. Reach out to our team to schedule your session.

PW Consulting — translating metallurgical nuance into strategic advantage for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Hot-Work Die Steels Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com