Polycarbonate Sheet Market — Strategic Preview for 2026 Decision-Makers

As companies position for growth and resilience in 2026, our Polycarbonate Sheet Market study from PW Consulting provides the strategic intelligence executives need to convert macro momentum into sustainable advantage. The market we modelled has grown from approximately USD 3.48 billion in 2020 to USD 4.45 billion in 2025 and is forecast to expand to roughly USD 4.58 billion in 2026 on the way to an estimated USD 6.45 billion by 2032, reflecting a compound annual growth rate of 5.46% across the 2026–2032 forecast horizon. These headline numbers tell the story of steady demand expansion—but the commercial choices behind them will determine winners and laggards. This article previews the report’s strategic value for 2026 while intentionally withholding the fine-grained segment tables that are available in the full publication.

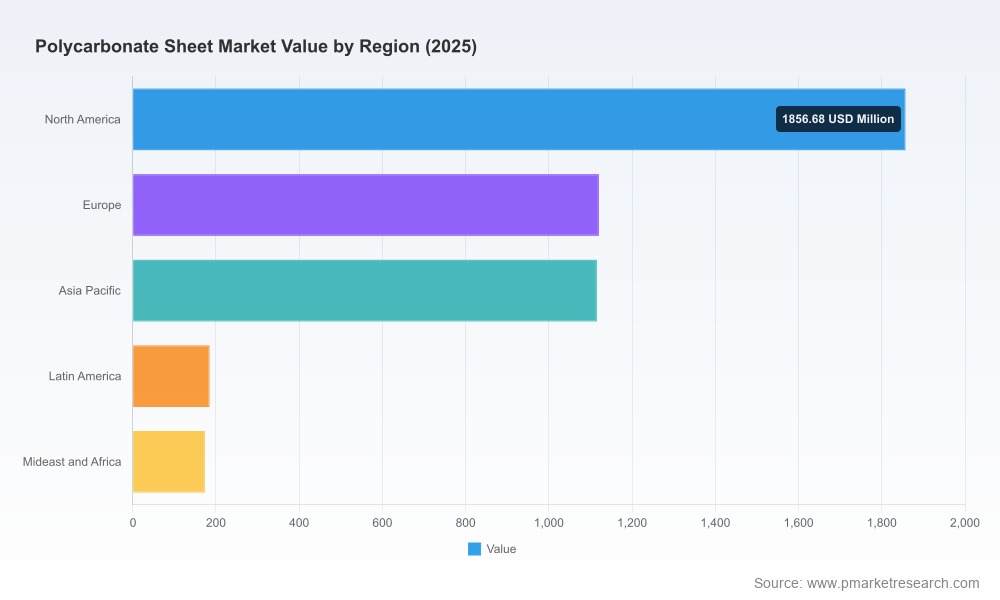

Polycarbonate Sheet Market

Market Trajectory and What It Means for 2026

The market’s historical climb through 2020–2025 and our 2026–2032 base-case scenario indicate a maturing industry with durable end-market demand across construction, transportation, electronics, and specialized industrial applications. Growth is neither hyper-cyclical nor static; it reflects a mix of secular drivers—urbanization, retrofit and renovation in mature markets, increased adoption of polycarbonate for lightweight and durable applications in transportation and electronics, and steady agricultural and industrial volumes.

Polycarbonate Sheet Market

For senior leaders, the key implication is this: 2026 is a year to translate favorable top-line momentum into structural defensibility. Moderate but persistent CAGR implies that incremental capacity, pricing power, and commercial excellence will matter more than one-off volume plays. Firms that align raw-material sourcing, differentiated product portfolios, and targeted go-to-market tactics will capture a disproportionately large share of the growth.

Polycarbonate Sheet Market

Market Dynamics and Risk Vectors Shaping Strategy

- Input-cost volatility: Bisphenol A (BPA), a core feedstock, exhibited pronounced price pressure—reaching approximately USD 1,215/MT in the U.S. in December 2025—while European production faced upward energy-linked cost migration in early 2026. Procurement strategies must now assume higher frequency of feedstock shocks and plan layered hedges and supplier diversification accordingly.

- Supply-side rationalization and capacity shifts: Recent capital deployments—most notably a significant capacity expansion announced by a major polymer producer in March 2026—signal a partial easing of domestic supply constraints in certain markets, while also creating short-term competitive pressure on pricing and product differentiation.

- Geopolitical and trade frictions: Tariffs and cross-border trade barriers are re-shaping sourcing and distribution economics. The China–U.S. trade dynamic has made localized sourcing and near-shore capacity options more than a cost conversation—they’ve become strategic hedges.

- Regulatory and sustainability momentum: New European Commission chemical transition measures and growing regulatory focus on chemical content will raise compliance costs, change product specifications, and accelerate demand for low-chemical-intensity and recycled-content grades.

- Margin compression from inflation and logistics: Persistent inflation and rising logistics costs have shrunk factory-gate margins and increased the importance of operational efficiency and freight-optimized network design.

Competitive Landscape — Concentration, Capabilities, and Strategic Moves

The polycarbonate sheet market exhibits a concentrated structure: the top three players control a substantial portion of market value, and the top five capture an even larger share, underscoring both incumbent scale and the importance of national/regional champions. This concentration creates attractive entry barriers for specialty players but also opportunities for agile mid-sized suppliers to exploit service, customization, and channel advantages.

- Plaskolite, Inc. (USA): North America’s leading engineered thermoplastics sheet manufacturer has doubled down on first-surface digital printing and specialty white/transmission products. Its recent launches show a focus on value-added formats for signage, security, and architectural finishes—areas where margin expansion is possible despite raw-material headwinds.

- Palram Industries Ltd. (Israel): A global brand in corrugated and flat polycarbonate with established product lines for construction and DIY, Palram’s strength lies in channel breadth and sustainability-oriented product variants—an increasingly important differentiator in regulated markets.

- Excelite Plastic Co., Ltd. (China) and other Chinese producers: Manufacturers with broad type portfolios and export capabilities play a dual role—competing on price in commodity segments while selectively pursuing higher-margin custom fabrication and export niches in developed markets.

- Regional fabricators and distributors (e.g., Varico LTD, A&C Plastics): These players earn outsized returns through local stock, fast-turn fabrication, and project services. For many end-users, logistics lead times and fabrication capabilities are as decisive as raw material price.

- New capacity and product introductions: The March 2026 capacity expansion by a major European/US polymer firm and product innovations launched in 2025 illustrate how supply actions and portfolio upgrades can quickly shift competitive dynamics—especially in fast-moving application segments.

What the Full Report Delivers — A Practical Toolkit

Our full PW Consulting study is designed as an executable playbook for commercial, supply chain, and corporate strategy teams. It includes:

- Verified market sizing and trend models (2020–2025 historical base and 2026–2032 scenarios) with downloadable forecasts and sensitivity toggles.

- Segment-level demand drivers and adoption curves by application type and region (note: segment tables are available in the full report).

- Raw-material and pricing analysis, with stress-tested scenarios for BPA and energy cost volatility, plus recommended hedging strategies and supplier scorecards.

- Supply-chain maps, lead-time matrices, and a factory-footprint optimization model to evaluate near-shore vs. central production choices.

- Competitive heatmaps and capability benchmarking for the leading manufacturers, regional fabricators, and distribution partners.

- M&A screening framework and a target shortlist methodology based on capacity gaps, channel access, and technology fit.

- Regulatory impact assessment and a compliance playbook for navigating the European Commission chemical transition and other jurisdictional shifts.

- A 12–36 month prioritized action plan with KPIs, risk mitigations, and a roll-up executive dashboard for board reporting.

Strategic Imperatives — Concrete Actions for 2026

- Secure feedstock resilience: Implement layered sourcing (spot, term, strategic partners), index-linked pricing corridors, and financial hedges for BPA exposure. Negotiate supplier agreements with shared cost-transparency clauses to reduce margin surprise.

- Reassess capacity strategy: Before committing to greenfield or large brownfield projects, run the report’s factory-footprint model to evaluate near-shore vs. import economics under multiple tariff and freight scenarios. Consider tolling or toll-processing partnerships to preserve capital while ensuring supply access.

- Differentiate by product-service systems: Invest in value-added SKUs (light-diffusing sheets, first-surface printable grades, bullet-resistant/technical laminates) and co-located fabrication to shorten lead times for project customers.

- Commercial and pricing playbook: Move from list-price competition to value-based pricing on specialty lines; deploy dynamic price-index clauses where possible on commoditized SKUs to protect margins.

- Regulatory and sustainability readiness: Map product portfolios against impending chemical-transition actions and define a low-chemical-content roadmap, including recycled-content trials and supplier audits to support claims and compliance.

- M&A and partnership scouting: Prioritize targets that close geographic distribution gaps, provide fabrication capabilities, or offer proprietary formulations. Use staged earn-outs tied to performance and integration milestones to de-risk transactions.

- Operational excellence and digitalization: Implement factory OEE improvements, predictive maintenance, and a digital order-to-delivery tracker to defend service levels as lead times compress.

How to Use This Preview — Next Steps for Executives

This preview frames the strategic choices facing industry players in 2026. If your team is evaluating capacity investments, procurement changes, product development budgets, or M&A options this year, the full PW Consulting Polycarbonate Sheet Market report provides the quantitative detail, scenario models, and tactical templates you need to operationalize those choices. It contains the segment-level revenue tables, regional and application breakdowns, and excel models that we have intentionally withheld here to preserve the utility of the full dataset as a decision-making asset.

To convert market growth into durable competitive advantage, companies must couple commercial discipline with supply resilience and regulatory foresight. The macro outlook is constructive, but the path to above-market returns will be determined by three capabilities: superior feedstock management, product and channel differentiation, and nimble footprint strategy. Our report gives leaders the maps and instruments to act decisively in 2026.

For detailed analysis of this topic, please visit the official page:Polycarbonate Sheet Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com