Nylon‑MXD6 Market — Strategic Brief for 2026 Decision‑Makers

Executive snapshot

Over the past half‑decade Nylon‑MXD6 has moved from niche specialty material to a commercially relevant polymer class with cross‑industry applications in packaging, automotive engineering plastics and high‑performance films. Our market model shows the global Nylon‑MXD6 market expanding from roughly USD 380 million in 2020 to about USD 506 million in 2025, and we forecast further growth to roughly USD 749 million by 2032. This trajectory implies a mid‑single digit compound annual growth rate of 5.85% across the 2026–2032 forecast window.

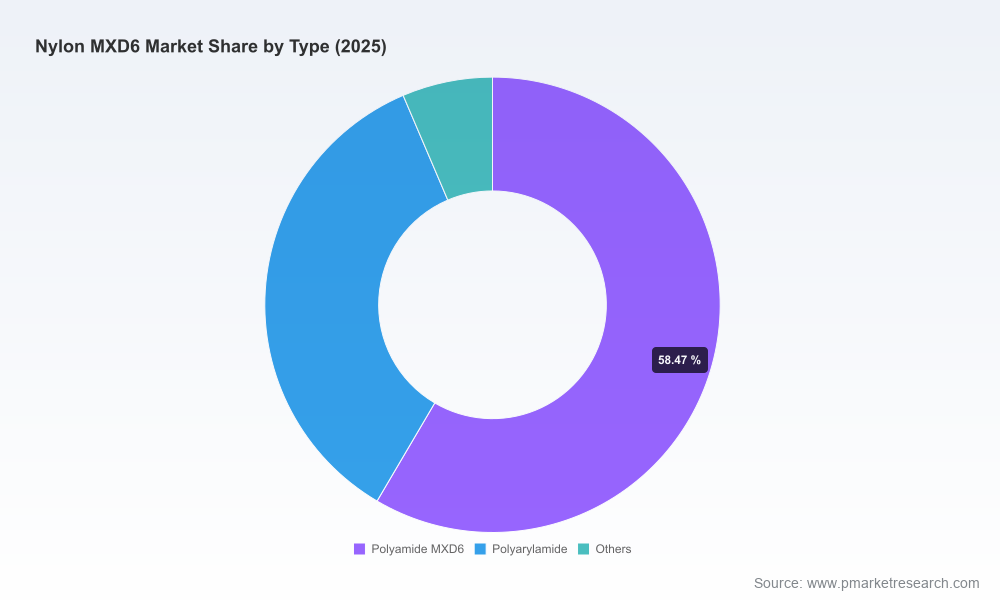

Nylon-MXD6 Market

Concentration is meaningful but not absolute: the top three players control a majority share of the market, and the top five increase that concentration further. This structure creates a market where technology leadership, licensing relationships and first‑mover capacity advantages matter materially for commercial outcomes.

Nylon-MXD6 Market

Why this research matters for 2026 strategic choices

- Transition timing: 2026 is the inflection point where bio‑mass balance certification, new domestic capacities, and an increased demand for specialty grades converge — altering supplier bargaining power, product roadmaps and commercial contracting norms.

- Risk posture: Feedstock volatility and upstream concentration in MXD6 precursors expose manufacturers and end‑users to price and availability shocks; timely mitigation choices made in 2026 will determine margin resilience through 2030.

- Value capture: As the market scales, premium differentiation (barrier performance, long‑fiber reinforcement, bio‑content) will become the primary lever for pricing power — not volume alone.

- M&A and partnership windows: The combination of established licensors, new domestic entrants and specialty compounders creates a three‑tier landscape ripe for bolt‑on acquisitions, licensing agreements and JV‑style capacity plays.

What the report delivers — practical, transaction‑grade insight

Our Nylon‑MXD6 Market report is built for practitioners making capital allocation, sourcing and product strategy decisions in 2026. The work goes beyond desk research and includes:

Nylon-MXD6 Market

- Validated market sizing and a transparent forecast model (2026–2032) that you can adapt to bespoke scenarios.

- Demand drivers and segmentation logic with scenario sensitivity (price, substitution, end‑use adoption rates).

- Supply‑side mapping: global producer capacity, technology/licensing footprints, and time‑phased capacity additions (including pilot‑to‑commercial ramps).

- Value chain cost analysis highlighting feedstock exposure, conversion economics, and margin waterfalls by product form (resin, film, specialty compounds).

- Competitive benchmarking and strategic positioning assessment for each major supplier, including licensing relationships and product portfolios.

- Commercial due diligence checklists: supplier questionnaires, quality and regulatory compliance scorecards, and sample contractual clauses for offtake and tolling.

- Risk and mitigation playbooks covering feedstock hedging, dual‑sourcing, inventory strategies, and regulatory change management.

- M&A and partnership playbook: target screening criteria, valuation multiples observed in adjacent specialty polymer deals, and integration risk matrices.

- Sustainability and regulatory roadmap with implications of mass‑balance certification and practical steps for claims management and chain‑of‑custody.

Competitive landscape — who matters and why

The Nylon‑MXD6 ecosystem is shaped by a small set of technology leaders, a growing group of regional compounders, and specialist converters that extract value through formulation and reinforcement.

- Mitsubishi Gas Chemical Company (MGC) — As the originator and dominant licensor of MX‑nylon technology, MGC underpins the material’s commercial architecture. Its MX‑Nylon portfolio spans film‑grade, molding‑grade and barrier‑enhanced variants. Critically, MGC has moved into certified mass‑balance bio‑based grades, launching a commercial product in early 2026 that achieves 25% bio‑sourced MXDA equivalence under ISO 22095. For buyers and investors, MGC’s roadmap sets the baseline for performance expectations and sustainability claims.

- Licensed and regional producers — Licensed producers play a dual role: they expand global capacity and create points of commercial friction through localized pricing and supply reliability. Licensees can offer closer logistics and faster commercial response than licensors, but buyers should validate license scope, feedstock consistency, and intellectual property boundaries when transacting.

- Chinese compounders and new entrants — A cluster of producers in China and greater Asia is shifting MXD6 from an import‑reliant specialty to a domestically supported polymer. Recent pilot projects and planned capacity additions evidence national import‑substitution strategies. These entrants are also the source of differentiated products (long‑fiber‑reinforced LFT‑MXD6, high rigidity compounds) that change the competitive calculus for engineering plastics in automotive and industrial applications.

- Specialty compounding houses and converters — Firms that integrate fillers, fibers and barrier technologies are capturing value downstream by creating application‑ready materials. For OEMs evaluating material switches, working with compounders reduces implementation risk—but it also creates dependency on formulation IP that should be contractually managed.

Supply chain and feedstock dynamics — the hidden cost driver

Nylon‑MXD6 is chemically tied to meta‑xylylenediamine (MXDA), itself derived from m‑xylene and ammonia. That linkage places MXD6 economics squarely within aromatics and basic chemicals markets. Industry data shows that crude oil and aromatics price swings can produce more than a 30% variation in feedstock cost profiles, materially affecting producer margins and contract pricing.

Practical implications for 2026 procurement and strategy:

- Hedging and contract design: Long‑dated offtakes with price collars or index‑based pass‑throughs reduce spot exposure for both buyers and sellers.

- Diversification: Nearshoring or local licensed supply can mitigate logistics shocks but requires careful supply‑risk and IP audits.

- Sustainability as a hedge: Mass‑balance certified bio‑content grades can insulate brands from regulatory cost increases tied to carbon or feedstock constraints—but they also require transparent chain‑of‑custody validation.

Regulation, sustainability and certification

Two regulatory realities are particularly influential in 2026: the operationalization of mass‑balance certification (ISO 22095) and national strategies focused on specialty polymer self‑sufficiency. The ability to market a mass‑balance bio‑based MXD6 grade at commercial scale—now demonstrated at a 25% bio content level—alters buyer negotiations in food packaging, consumer goods and regulated product categories where renewable content is a purchase criterion.

Strategic recommendations — prioritized actions for 2026

- Immediate (0–6 months): Conduct supplier resilience audits for top‑tier MXD6 sources; negotiate price‑index clauses tied to aromatics benchmarks; validate supplier ISO 22095 mass‑balance credentials if bio‑content is a strategic requirement.

- Near term (6–18 months): Pilot application trials with composite and barrier grades; explore licensing or JV options with technology owners to secure preferential access to novel grades; pursue conditional offtake agreements with staged volume commitments to support new capacity ramps.

- Medium term (18–36 months): Consider bolt‑on acquisitions of regional compounders to internalize formulation IP and accelerate time‑to‑market for high‑value applications (automotive structural parts, barrier film for packaging).

- Risk planning: Build scenario models that stress test oil/aromatics shocks, regulatory tightening on non‑renewable content, and accelerated adoption of substitution polymers. Use these models to stress test pricing, inventory policies and capex timing.

How to use the full report

This briefing demonstrates the strategic contours of Nylon‑MXD6 as of 2026, but executives require granular inputs to finalize decisions: time‑phased capacity tables, regional cost curves, customer‑level demand forecasts, and supplier scorecards. The full report contains those datasets, a downloadable forecast model you can run under bespoke assumptions, and transaction templates aligned to the nuances of this market.

Conclusion — the window for strategic advantage

Nylon‑MXD6 is moving from specialty to scale. The market’s steady mid‑single digit CAGR, meaningful incumbent concentration and nascent waves of domestic capacity and bio‑content innovation together create a landscape where 2026 choices will have outsized impact on performance through the rest of this decade. Companies that act now—aligning procurement, R&D, commercial contracts and M&A strategy—will capture disproportionate value from this maturing market.

For a practitioner‑ready playbook, granular regional and application splits, and the downloadable financial model that underpins our projections, consult the full Nylon‑MXD6 Market report. It contains the actionable intelligence your 2026 investment committee needs to move from analysis to execution.

For detailed analysis of this topic, please visit the official page:Nylon-MXD6 Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com