Temperature Humidity Transmitter Market Size, Share, Growth Drivers, and Competitive Landscape

Other |

2026-06-03 13:00:04

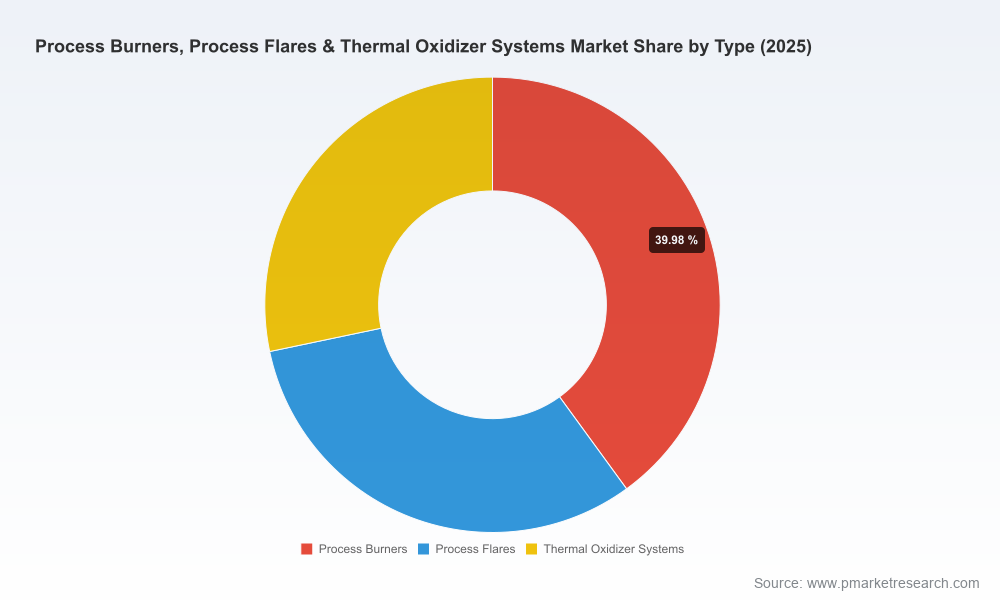

As PW Consulting releases its latest market study on Process Burners, Process Flares & Thermal Oxidizer Systems, senior executives, strategic planners and project sponsors face a narrow window to reset priorities for 2026. The market's macro trajectory is unambiguous: after a measured recovery in the early 2020s, the total addressable market reached USD 1,855 Million in our base year (2025) and is projected to expand at a 5.5% compound annual growth rate through the 2026–2032 forecast horizon, arriving at roughly USD 2,693 Million by 2032. That steady expansion masks material shift vectors — regulatory resets, capex realignments and technology inflection points — that must shape near-term decisions on procurement, retrofit strategies and M&A.

Process Burners, Process Flares & Thermal Oxidizer Systems Market

2026 is a planning inflection year. Many capital planning cycles, compliance roadmaps and vendor qualification processes initiated in 2024–2025 now hit execution gates. This report is designed as a decision-focused tool: it translates macro growth assumptions into actionable scenarios for OEM selection, retrofit prioritization and investment sizing, while protecting the granular competitive and segment intelligence that organizations rely upon to secure commercial advantage.

Process Burners, Process Flares & Thermal Oxidizer Systems Market

Timing: The forecast period (2026–2032) captures both immediate regulatory triggers and medium-term demand from industrial decarbonization and VOC control programs.

Process Burners, Process Flares & Thermal Oxidizer Systems Market

Scope: We combine a demand-side view of end-market drivers with a supply-side view of vendor capabilities, production constraints and aftermarket economics.

Decision utility: The analysis is structured to convert market insight into procurement checklists, retrofit decision trees and M&A scouting briefs suitable for 2026 execution calendars.

Three macro dynamics should dominate boardroom discussions:

Regulatory tightening and compliance windows. Several regulatory events in late 2025 and early 2026 significantly change the compliance landscape. Notably, new requirements affecting existing sources came into force in early March 2026, creating immediate retrofit mandates for certain process flares and burners. Separately, targeted certifications — such as state-level approvals for variable orifice flare technologies — have started to materialize, altering vendor qualification lists and procurement specifications.

Fuel and operating-cost volatility. The market is operating against a backdrop of pronounced natural gas price swings in early 2026, with spot benchmarks moving from materially higher levels in January to a substantial decline by April. That volatility has two implications: it changes operating cost projections used in payback models for heat-recovery and fuel-efficient burner technologies, and it shifts the sensitivity profile of customers evaluating recuperative vs. regenerative thermal oxidizers.

Fragmented supply base. Market concentration metrics indicate a fragmented vendor landscape — the top three suppliers account for a modest share of overall revenue, and even the top five leave significant market room for regional specialists and engineering-focused players. That competitive fragmentation fuels aggressive differentiation on service, technical certification, and lifecycle cost contracting rather than pure price leadership.

Across process burners, flares and thermal oxidizers, three technical themes are decisive for 2026 procurements:

Efficiency-embedded compliance. Buyers are increasingly valuing systems that pair emissions control with heat recovery or energy integration. Recuperative and high-efficiency thermal oxidizers that deliver demonstrable OPEX reductions are moving from niche to mainstream in capex approval rounds.

Modularity and rapid retrofitability. Tight compliance timelines mean that modular, skid-mounted solutions and pre-fabricated components can shorten outage windows and reduce installation risk. Vendors with proven modular portfolios will be advantaged in congested project pipelines.

Digital enablement of lifecycle services. Remote monitoring, predictive maintenance and service-as-a-contract models are replacing one-off aftermarket transactions. For asset owners focused on uptime and total cost of ownership, vendor digital maturity is becoming a procurement discriminant.

The vendor field spans legacy engineering houses, specialized burner and flare manufacturers, and systems integrators focused on oxidizer technology. Several established firms stand out for strategic reasons:

John Zink (Tulsa, Oklahoma) — recognized for its broad portfolio across burners and flaring solutions and for deep combustion-engineering expertise. Their historical strength in custom-engineered solutions and compliance-focused design makes them a go-to for projects where regulatory certification is a gating factor.

Zeeco (Tulsa, Oklahoma) — notable for high-performance flare systems and emerging work in integrated combustion-management packages. Their emphasis on testing and factory acceptance supports clients with tight commissioning windows.

Anguil Environmental Systems (Milwaukee, Wisconsin) — a specialist in oxidizer solutions with a strong track record in VOC control applications. Anguil’s modular options and service models appeal to mid-cap industrial operators seeking predictable lifecycle economics.

Process Combustion Corporation (Pittsburgh, Pennsylvania) — experienced in thermal oxidizer systems and focused on process integration. PCC typically competes on engineering depth for complex process-driven applications.

TANN Corporation (Appleton, Wisconsin) — known for engineered burner technologies and custom design services for thermal process applications.

Epcon Industrial Systems (The Woodlands, Texas) — an intensifying presence in recuperative thermal oxidizers and heat-recovery systems; Epcon’s May 2025 product showcase underlined their push into VOC control with enhanced energy-recovery emphasis.

For procurement teams, the vendor call is not binary. The optimal supplier mix often pairs an established global OEM for major flaring and burners with specialized oxidizer vendors for VOC abatement and heat recovery. Our vendor framework evaluates technical fit, delivery reliability, aftermarket coverage and financial strength — not just sticker price.

The full report is structured to be immediately operational for 2026 program managers. Key deliverables include:

A transparent market model (base year 2025, forecast 2026–2032) that maps demand drivers to spending pools and project timelines.

Scenario-based demand paths tied to regulatory milestones and fuel-price scenarios, enabling stress-tested CAPEX plans.

Vendor benchmarking with capability matrices, procurement negotiation playbooks and risk-adjusted supplier scorecards.

Technology roadmaps and retrofit decision trees that prioritize projects by payback, compliance risk and operational disruption.

Project pipeline diagnostics and an M&A heatmap identifying strategic acquisition targets and partnership levers.

Practical procurement collateral: RFx templates, factory acceptance criteria and lifecycle cost calculators calibrated to 2026 operating assumptions.

To translate market insight into competitive advantage this year, executives should prioritize four pragmatic actions:

Re-run capex approvals using scenario-adjusted fuel prices and compliance timelines. The recent volatility in natural gas pricing alters OPEX assumptions that underpin many recovery choices for thermal oxidizers and recuperative systems.

Fast-track vendor pre-qualification for modular retrofit solutions where regulatory deadlines apply. Locking in lead times and acceptance testing windows now reduces execution risk.

Negotiate service-and-performance contracts that transfer uptime risk to vendors. In a fragmented market, differentiated warranty and performance guarantees shorten the total-cost-of-ownership gap between incumbents and specialists.

Update M&A and strategic-partner scouting to reflect the fragmented concentration profile of the industry: targeted tuck-ins can rapidly expand capability in oxidizers, VOC control or modular manufacturing.

Even with a positive medium-term outlook, several risks merit ongoing surveillance in 2026:

Regulatory sequencing and enforcement. While new rules create volumes, they also introduce timing uncertainty around permits and retrofit windows; governance changes at the national or state level can accelerate or delay demand.

Commodity-price reversals. Rapid rebounds in fuel prices could re-cast the capital case for energy-recovery technologies, affecting procurement-incentive framing and ROI thresholds.

Supply-chain bottlenecks for specialty alloys and controls. Persistent lead-time pressures in specific components can create selective shortages even when aggregate capacity appears adequate.

For asset owners and technology providers, 2026 is a year to convert strategic intent into disciplined execution. The market’s steady compound growth masks a set of tactical decisions — compliance sequencing, retrofit design choices, vendor partnerships and capitalization strategies — that will determine winners and followers. PW Consulting’s study is constructed to move from insight to action: mapping compliance drivers and operating economics to procurement-ready options that materially shorten decision cycles.

To access the full suite of models, vendor scorecards and subsegment projections that underpin these findings, including granular regional and application intelligence locked in our annexes, please consult the complete report. The summary above is intentionally high-level; the detailed datasets and scenario matrices are available in the full publication for teams preparing to execute in 2026.

For detailed analysis of this topic, please visit the official page:Process Burners, Process Flares & Thermal Oxidizer Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com