Alcohol Ingredients Market Consumer Preferences and Purchase Behavior Analysis 2026–2034

Food |

2026-06-25 10:59:07

As organizations prepare capital, R&D and sourcing plans for 2026, the Linear Friction Welding (LFW) machines market has transitioned from niche pilot projects to an investable industrial technology with measurable revenue momentum. PW Consulting’s latest market study—anchored on a 2025 base year and a forecast window through 2032—identifies the structural forces shaping supplier economics, adoption pathways, and competitive advantage. The market expanded steadily in the first half of the decade and, supported by a compound annual growth rate (CAGR) of 5.59% across the 2026–2032 forecast horizon, is projected to grow meaningfully through the end of the forecast period. This preview summarizes the strategic value of our analysis for 2026 decision cycles while intentionally withholding granular segment-level figures to prompt direct engagement with our full report for transaction‑grade detail.

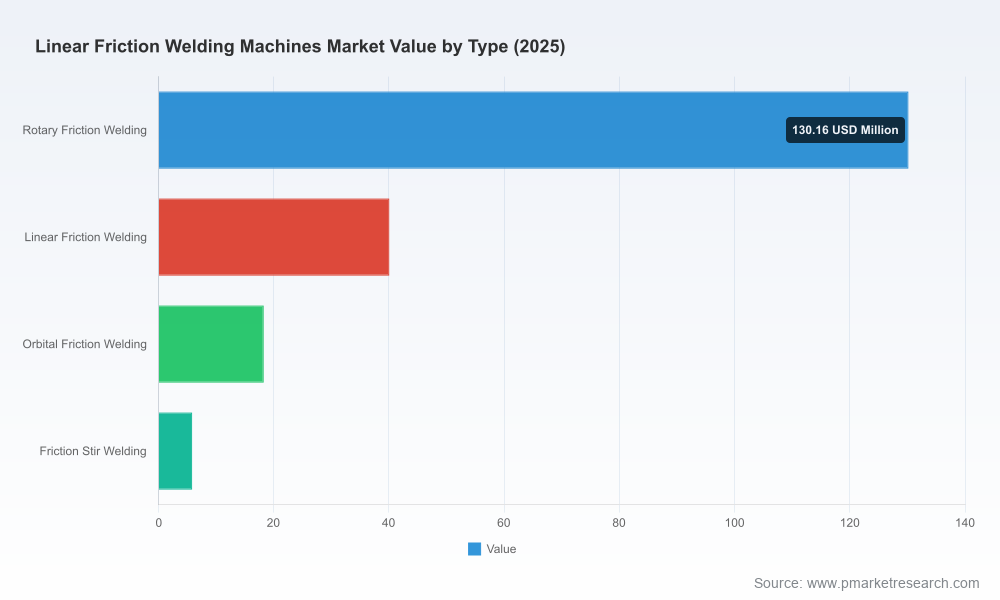

Linear Friction Welding Machines Market

Capital allocation clarity: LFW entails high‑ticket equipment and tooling investments. Our study translates market momentum and supplier economics into investment envelopes and payback sensitivities that CFOs and plant strategists can use to prioritize projects in 2026 CAPEX rounds.

Linear Friction Welding Machines Market

Technology integration roadmaps: R&D and manufacturing leads need an executable path to incorporate LFW into high‑value assemblies (notably aerospace and advanced automotive structures). We map adoption sequences—process validation, tooling standardization, and quality controls—so teams can accelerate from prototype to certified production.

Linear Friction Welding Machines Market

M&A and partnership screening: The market shows mid‑level concentration among a few incumbent suppliers. Our competitive scorecards and scenario modelling help corporate development teams identify acquisition targets, JV partners, or licensing opportunities consistent with strategic growth or consolidation plays.

Risk and compliance alignment: With aerospace-grade process controls and standards increasingly dictating purchase decisions, procurement and quality functions require an operational checklist to ensure AS9100 alignment and audit readiness before committing to equipment orders.

From a historical foothold in 2020 to a materially larger installed base by 2025, the overall market demonstrates healthy demand pull across high‑precision manufacturing sectors. The aggregated market size rose steadily through the 2020–2025 period and continues on a growth path into the 2026–2032 forecast window. At a market‑level CAGR of 5.59% for the forecast period, the sector is large enough to support multi‑tier supplier ecosystems yet concentrated enough that market leadership and first‑mover advantages matter. The market concentration metrics in our study indicate that the top three suppliers control a majority share of revenue, while the top five capture roughly three quarters of the market—conditions that favour strategic alliances and value‑based differentiation rather than pure price competition.

Material and process fit: Titanium and high‑performance alloys are core to LFW’s aerospace value proposition because the process delivers fatigue‑robust, filler‑free joints. That material–process affinity creates a durable demand base in aerospace and other high‑reliability sectors.

Labour and quality economics: One of LFW’s compelling operating benefits is its ability to deliver defect‑free, repeatable welds that reduce dependence on extensive manual rework and downstream inspection. This matters in contexts where labour cost volatility or scarcity drives automation and process consistency premiums.

Regulatory and certification thresholds: High‑value applications demand documented, auditable processes. Compliance with aerospace standards (such as AS9100 quality frameworks and their equivalents) is a gating factor for many buyers, increasing the total cost of adoption but lowering lifetime risk.

Capital intensity as a diffusion limiter: High up‑front equipment and tooling costs mean adoption tends to concentrate in well‑funded manufacturers and OEM supply chains. This dynamic creates an opening for service models (e.g., contract manufacturing, machine leasing, or process qualification as a service) that lower entry barriers for smaller adopters.

The competitive topology combines specialist OEMs, systems integrators, and research service providers. Each class presents different partnership and procurement implications for buyers and investors.

Manufacturing Technology Inc. (MTI) (South Bend, Indiana) — MTI is a purpose‑built linear friction welding equipment manufacturer with systems designed for full‑sized aerospace components and an aftermarket service footprint. Their product mix and services orientation make them a logical partner for OEMs seeking turnkey machine supply and lifecycle support.

Taylor‑Winfield Technologies (Wheatland, Pennsylvania) — With a focus on patented, compact LFW designs, Taylor‑Winfield positions itself for mainstream manufacturing applications where floor space and cost parity matter. Their approach signals a potential pathway for broader adoption in industries beyond aerospace where throughput and capital efficiency are primary constraints.

Bielomatik (Germany) — A supplier with depth in specialized industrial LFW machines. European engineering firms like Bielomatik leverage regional aerospace and industrial demand for niche, application‑specific solutions.

Thompson Friction Welding (part of KUKA) (UK) — Operating within a larger automation group provides a systems‑integration advantage, particularly for customers seeking comprehensive robot‑to‑process solutions and scale‑up paths tied to manufacturing automation roadmaps.

Dukane Corporation (USA) — Known for addressing aerospace and composite applications, Dukane’s focus underscores the crosscutting opportunity between LFW and next‑generation composite joining strategies.

STIRTEC GmbH (Germany) — A technology and tooling innovator whose advanced LFW techniques and fixtures are of particular interest to aerospace primes and tier suppliers pursuing weight and performance optimization.

TWI Ltd. (UK) — As a pioneer and incubator for LFW process development, TWI offers process validation, training and machine‑agnostic services that de‑risk adoption for conservative OEMs and regulators.

Strategic takeaways for suppliers and buyers: incumbents are defending margins with aftermarket and service offerings; challengers are targeting cost‑and‑footprint advantages; and research groups continue to reduce adoption friction by standardizing qualification pathways. For investors, these patterns suggest differentiated return profiles between product sellers, service providers, and integrators.

Aftermarket and lifecycle services: As installed bases grow, consumables, retrofits, and qualification/validation services will represent recurring, higher‑margin revenue that offsets capital sales cyclicality.

Process standardization and tooling IP: Companies that own robust tooling portfolios and process recipes for specific alloys and assemblies will be able to capture value through licensing and performance guarantees.

Integration with automation and inspection: Seamless integration of LFW heads with robotic cells and in‑line non‑destructive examination (NDE) will unlock productivity gains and broaden the addressable market.

Flexible financing models: Leasing, capacity‑as‑a‑service, and contract manufacturing will lower buyer barriers and broaden adoption in mid‑tier manufacturers.

Our full report is designed to be immediately actionable for executive teams, program managers and investors. Key deliverables include:

Validated market sizing and demand modelling across 2020–2032, with sensitivity analyses tied to aerospace platform ramp rates and material adoption curves.

Scenario‑based forecasts that isolate downside and upside market outcomes under varying macro and industry assumptions.

Supplier scorecards and capability matrices that benchmark machine OEMs on throughput, footprint, service coverage and certification support.

Capital cost and TCO models that translate equipment choices into plant‑level economics and ROI timelines.

Compliance and audit playbooks for AS9100 and related production qualification steps, tailored to LFW process characteristics.

M&A target lists and partnership archetypes, ranked by strategic fit and integration risk.

Technology roadmap and tooling IP assessment, highlighting where process innovation can create defendable margins.

Procurement: use our equipment TCO models and supplier scorecards to shorten RFQ cycles and negotiate lifecycle commitments rather than upfront price alone.

Operations: prioritize pilot projects where material fit (e.g., titanium alloys) and quality economics are most compelling; lock in process qualification upfront to avoid rework.

Corporate development: target small‑to‑mid cap specialists with proprietary tooling or aftermarket channels for tuck‑in acquisitions that expand serviceable addressable market.

R&D: focus on tooling modularity and inspection integration to reduce cycle time and increase throughput without compromising certification readiness.

Our study takes a practitioner’s view—hard financial models, supplier intelligence and operational checklists—while recognizing that granular segmentation and contract‑level detail are commercially sensitive and best consumed in the full report. The summary above is intended to equip 2026 planners with the strategic lens necessary to ask the right questions at board, program and plant levels. To access the full dataset, supplier benchmarking files, and downloadable modelling tools that support transaction and site‑level decisions, please consult the full PW Consulting report.

For detailed analysis of this topic, please visit the official page:Linear Friction Welding Machines Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com