North America Bronchoscopy Device Market Driven by Precision Pulmonary Diagnostics

Health |

2026-06-29 18:10:56

As companies finalize capital allocation and product roadmaps for 2026, the bottle blowing machine market presents a decisive intersection of technology, regulation, and sustainability. This preview synthesizes PW Consulting’s latest full study — based on a 2025 base year and a seven-year forecast through 2032 — to highlight the strategic choices facing manufacturers, brand owners, and equipment suppliers. We show the macro trajectory and the practical decision levers; we intentionally withhold granular segment tables and proprietary vendor scores to motivate direct access to the full dataset and models.

Bottle Blowing Machine Market

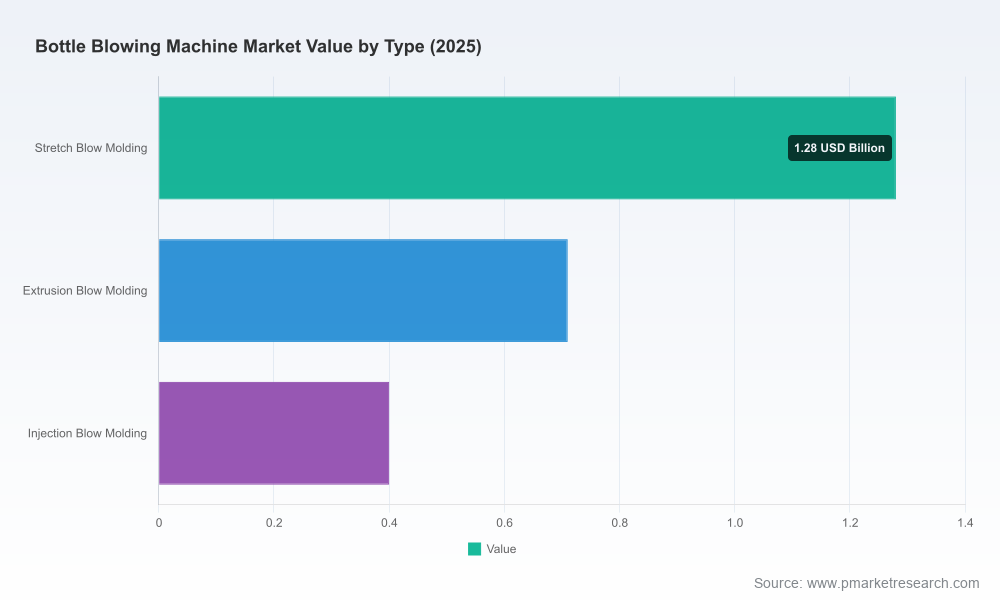

PW Consulting’s top-line modelling traces the market from the early 2020s into the next decade. The global market expanded from the low‑billion range in 2020 to an estimated USD 2.39 Billion in 2025, and our forecast sees continued steady growth to roughly USD 3.28 Billion by 2032, underpinned by a compound annual growth rate of 4.57% across the forecast window. That pace reflects the combined effect of equipment replacement cycles, incremental capacity additions in emerging supply chains, and demand driven by beverage and packaged consumer goods sectors.

Bottle Blowing Machine Market

For 2026 specifically, the market sits at an inflection point: policymakers are tightening requirements on energy and recycled content, while OEMs are launching higher-throughput and lower-footprint systems. These dynamics compress the decision window for 2026 CapEx: delaying investments risks higher compliance retrofits and lost first-mover advantage on lightweighting and recycled-material bottle formats.

Bottle Blowing Machine Market

The full study is structured as a hands‑on toolkit for 2026 decision-makers. Highlights include:

To preserve the strategic value of the full dataset, detailed regional and application share tables, unit pricing matrices, and the vendor scoring matrix are available only in the complete report and model package.

The market is served by a blend of integrated systems suppliers and specialized equipment makers. PW Consulting’s qualitative assessment shows distinct strategic postures among the leading players:

Market concentration is moderate — the top three and top five players account for a substantial portion of industry revenue — which benefits buyers through mature product portfolios but creates vendor lock‑in risk if aftermarket service networks are weak in a buyer’s target geography.

Recent vendor activity underscores these strategic directions: OEMs showcased advanced blow molding lines at major exhibitions in 2026, and multiple companies launched higher-capacity or material‑savings solutions in 2025–2026. These moves accelerate the diffusion of energy-efficient and high-throughput systems into higher-volume beverage and water segments.

Two regulatory forces are particularly salient for 2026 planning. First, mandatory energy-monitoring modules for injection and blow molding equipment under the EU EcoDesign rules take effect on May 1, 2026 — creating an immediate compliance requirement for lines sold into or operating within the EU. Second, the EU’s Packaging and Packaging Waste Regulation sets progressively rising minimum recycled-content targets for single‑use beverage bottles, with notable thresholds approaching 2030 and beyond. These regulations force a re-evaluation of equipment specifications, process controls, and material sourcing strategies.

Operationally, labor-market friction — technician shortages and skills gaps — adds execution risk to retrofit programs and new-line start-ups. Resin-price volatility further complicates ROI calculations. The full report provides stress-tested scenarios to quantify how these variables alter payback periods and TCO across machine classes.

This preview is designed to inform the strategic narrative and to highlight the actionable levers available to executive teams in 2026. For procurement directors and strategy leads who need the operational detail — regional demand breakdowns, application-specific forecasts, vendor scorecards, unit-price matrices, and editable financial models — PW Consulting’s full Bottle Blowing Machine Market report and dataset are the essential follow-up. The full package equips teams to convert the high-level insights in this briefing into procurement specs, investment approvals, and supplier negotiations with confidence.

Contact PW Consulting to request the full report, model access, and a briefings workshop that adapts our scenarios to your company’s product mix and investment calendar. The 2026 policy and technology inflection points make timely, data-backed decisions a competitive advantage — this preview shows the path; the full study provides the map and the instruments to navigate it.

For detailed analysis of this topic, please visit the official page:Bottle Blowing Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com