Fine Pixel Pitch LED Displays: A 2026 Strategic Preview for Decision Makers

PW Consulting’s Fine Pixel Pitch LED Displays Market study is our field-grade briefing for executives planning capital allocation, procurement, product roadmaps, and supply‑chain hedging in 2026. This preview summarizes the report’s strategic value, synthesizes the macro trajectory shaping near‑term decisions, and highlights the competitive and supply‑side dynamics that will determine winners and losers as the sector scales. We intentionally show the analytical scaffolding and decision levers you need to evaluate opportunities — while preserving the report’s proprietary segment-level datasets that are only available in full on our portal.

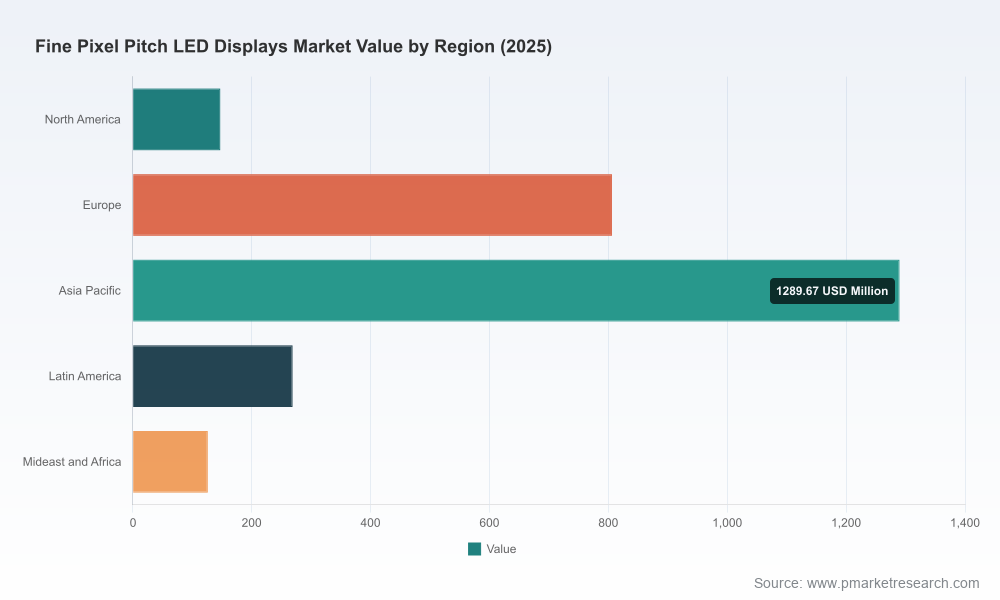

Fine Pixel Pitch LED Displays Market

Market snapshot: growth trajectory and structural position

The fine‑pixel‑pitch LED market has moved from a niche specialty to a mainstream indoor visualization platform within five years. On an annualized basis, the market more than doubled from 2020 through 2025, rising from roughly USD 1.27 billion in 2020 to about USD 2.64 billion in 2025 (base year). Our forecast models project continued rapid expansion through the coming decade: the market is expected to exceed USD 3.0 billion in 2026 and, under the central forecast, grow at a compound annual growth rate of 15.55% during 2026–2032 to reach an addressable market on the order of magnitude of several billion dollars by 2032.

Fine Pixel Pitch LED Displays Market

Concentration metrics point to a market where a small group of established players hold a majority share while room remains for specialized entrants. The top three vendors account for just over half of current market revenue, while the top five approach two-thirds — a structure that rewards both operational scale and differentiated technology roadmaps.

Fine Pixel Pitch LED Displays Market

Why this research matters for 2026 decisions

- Timing of investment and capacity expansion. With mid‑single‑digit to high‑teens CAGR dynamics, 2026 is a pivotal year to decide whether to expand in-house manufacturing capacity, partner with large integrators, or adopt an asset‑light reseller strategy. Decisions taken this year will significantly affect cost bases and time‑to‑market through 2028–2030.

- Procurement and margin protection. ASP and procurement trends have been volatile: improved chip yields and automated assembly drove large ASP declines earlier in the decade, but component pressure and localized shortages have recently pushed module pricing up in places. Executives need a nuanced procurement playbook to lock in margin protection while preserving technical flexibility.

- Technology platform road‑mapping. COB and MicroLED platforms are maturing rapidly. Selecting the right technology node (COB vs SMD vs MicroLED), pixel pitch targets, and color‑gamut capabilities for your end‑markets requires forward‑looking scenario modeling to avoid overengineering or stranded inventory.

- Geopolitical and regulatory contingency planning. Export controls on advanced semiconductor designs and concentrated supply chains in China and Taiwan have altered risk profiles. Firms must include export‑control and localization variables in any multi‑year investment or sourcing decision.

What the full report delivers (practical, executable content)

- Top‑line demand modeling and scenario runs keyed to alternative macroeconomic and supply‑chain stress tests — enabling stress‑tested revenue and margin projections for 2026–2032.

- Integrated cost‑of‑ownership (TCO) matrices for dominant pixel pitches and platform types, including sensitivity analyses to key input cost drivers (LED chips, driver ICs, PCBs, and assembly labor).

- Vendor scorecards and go‑to‑market mapping: a vendor short‑list for enterprise procurement, with capabilities, delivery lead‑times, certification status (including TAA where applicable), and typical commercial terms.

- Supply‑chain heatmaps and dual‑sourcing playbooks, identifying critical nodes where dual‑sourcing, local buffer inventory, or strategic vertical partnerships reduce delivery risk.

- Commercial contract templates and procurement checklists tailored to fixed‑price, cost‑plus, and performance‑based engagements — designed to lock in warranty, service SLAs, and upgrade clauses.

- Implementation playbooks for key verticals (broadcast, control rooms, simulation/visualization, retail and corporate), addressing optical calibration, content workflow integration, and lifecycle service strategies.

- Capex vs SaaS financial templates that enable CFOs to evaluate owning vs renting models for large installations over 3–7 year windows.

Competitive landscape — who to watch and what they’re doing

The competitive field comprises a mix of legacy display manufacturers, LED specialists, and integrators moving up the value chain. Leading vendors are investing aggressively in COB and MicroLED designs to capture premium indoor applications that demand near‑pixel‑perfect fidelity.

- Planar (Oregon, USA) — continuing its push into ultra‑fine pitches with a new MicroLED COB series introduced in fall 2025 that emphasizes cinema‑grade color space and high brightness for mixed lighting environments.

- Nanolumens (Atlanta, USA) — expanded its NXT family at the start of 2026 to broaden COB options for retail and corporate applications, highlighting supply‑chain compliance (including TAA‑aligned SKUs) for public sector procurement.

- Vanguard LED Displays & American LED Wall (USA) — both emphasize sub‑1mm offerings that target rental/staging and enterprise boardrooms, with a focus on modularity and rapid deployment.

- Leyard & Absen (Shenzhen, China) — pursue scale and low‑pixel‑pitch innovation, including sub‑0.5mm MicroLED platforms aimed at control rooms and retail visualization.

- PixelFLEX (Nashville, USA) — differentiates on flexible form factors and COB production techniques to reach specialized visualization and experiential markets.

Recent product launches and expansions signal a race to define premium performance tiers — we expect product announcements to become more frequent as vendors push to lock enterprise reference customers and to demonstrate performance ceilings for MicroLED/COB technologies.

Supply‑side dynamics and policy tailwinds/headwinds

- Falling ASPs, but rising component volatility. Improvements in chip yields and automated assembly drove sizeable ASP declines earlier in the decade. However, component pricing and intermittent driver IC shortages have recently increased module pricing and introduced supply delays for a meaningful share of manufacturers.

- Export controls and geopolitical exposure. U.S. export‑control measures affecting advanced semiconductor designs are already influencing access to certain driver ICs, with implications for design cycles and time‑to‑market for some suppliers in major production hubs.

- Concentration risk. The heavy upstream concentration of chip fabrication and panel assembly creates systemic risk: a localized disruption can cascade through lead times and price points across multiple markets.

- Procurement leverage. Buyers who act quickly to standardize architectures and lock multi‑year volume agreements can capture lower unit economics; late movers risk paying a premium as component cycles and capacity constraints re‑assert.

Strategic implications and recommended moves for 2026

- Adopt a tiered sourcing strategy. Combine a core long‑term supplier with a set of regional partners for tactical surge capacity. Insist on clause‑based protection: agreed lead times, change‑order pricing formulas, and penalty/bonus mechanisms tied to delivery and conformity.

- Prioritize platform‑level flexibility. Design systems that allow pixel replacement and module swaps to extend useful life across pixel pitches — this reduces the risk of obsolescence as pixel pitch economics evolve.

- Revisit commercial models. For high‑visibility installations, move toward hybrid models that pair upfront CapEx with recurring service and image‑management fees to smooth margins and align incentives with technology upgrades.

- Insure and hedge. Use inventory hedges for critical driver ICs, work with insurers on supply‑chain disruption policies, and explore localization where scale justifies a domestic source of modules or critical components.

- Differentiate on services. With hardware increasingly commoditized, post‑installation calibration, lifecycle content management, and uptime SLAs become durable differentiators. Bid service bundles as part of the value proposition.

- Monitor regulatory vectors. Build a regulatory watch function into procurement and product teams to surface export‑control impacts early and redesign supply chains proactively.

Risk map and mitigation quick checklist

- Geopolitical shock: dual‑source critical components; maintain safety stock for 2–3 delivery cycles.

- Component price spikes: adopt index‑linked pricing clauses and agree on change‑order ceilings.

- Product obsolescence: modular design and software‑first control architectures extend device useful life.

- Vendor concentration: diversify across at least three certified suppliers for mission‑critical projects.

How to use this preview — and why read the full report

This preview frames the strategic choices that matter in 2026. The full PW Consulting report contains the granular, actionable intelligence you need to implement the recommendations above: market‑level demand curves by pixel pitch and application, regional roll‑outs and timing windows, vendor cost models, validated TCO calculations, and downloadable procurement templates. Importantly, the full study includes our proprietary segment-level tables, supplier scorecards, and scenario spreadsheets — information we withhold here to preserve competitive value and to enable bespoke consultation with your team.

For procurement leads, product managers, and corporate strategy teams preparing 2026 budgets, this report converts high‑level trends into executable workstreams. If your 2026 plan depends on LED display performance, delivery certainty, or predictable TCO, your next step should be a focused review of the full dataset and vendor short‑lists in our portal — or commissioning a tailored workshop with PW Consulting to map the findings directly to your product lines, supply contracts, and deployment roadmaps.

Contact PW Consulting to schedule a briefing or to access the complete Fine Pixel Pitch LED Displays Market report, which contains the segment‑level forecasts, supplier evaluations, and tactical templates needed to make high‑confidence decisions in 2026.

For detailed analysis of this topic, please visit the official page:Fine Pixel Pitch LED Displays Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com