Lime Market 2026 Strategic Primer — PW Consulting

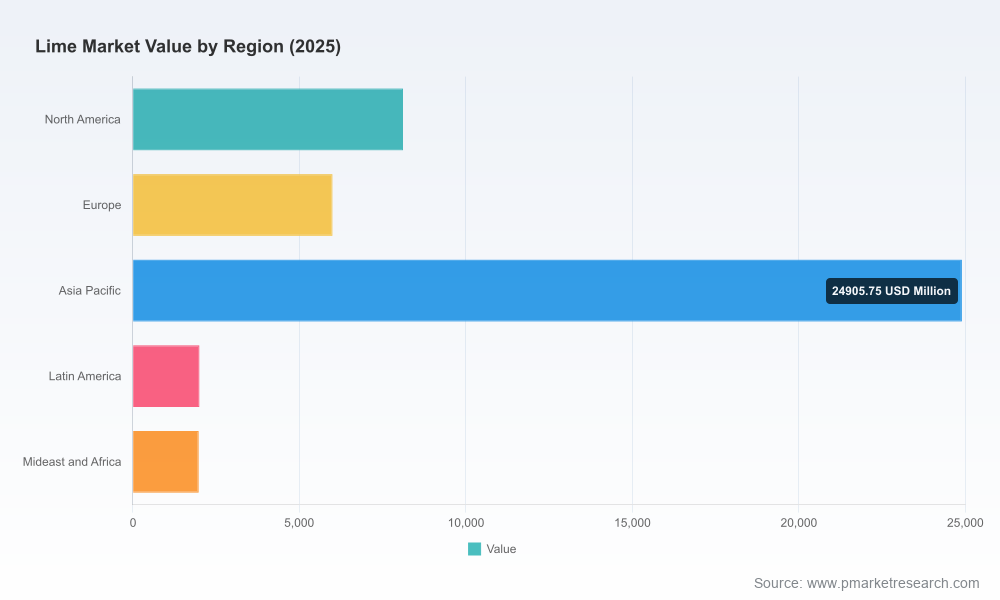

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present this executive primer to frame the strategic choices facing executives in 2026. Built on a rigorous base-year of 2025 and a forward-looking forecast through 2032, our Lime Market research translates commodity dynamics into actionable decisions for producers, buyers, investors and policy teams. The global market expanded from roughly USD 35,000 million in 2020 to an estimated USD 43,000 million in 2025, and our baseline outlook (CAGR 2.5% through the 2026–2032 forecast window) sees the market continuing to grow, reaching just over USD 51,000 million by 2032. This note previews the strategic value of the full report while intentionally withholding the granular segment tables and proprietary datasets that are included in the paid study.

Lime Market

Why this study matters for 2026 decision-making

- Investment timing and scale: Modest but steady CAGR means capex decisions (kiln upgrades, new sustainable operations, logistics investments) must be sized to defend margins rather than chase high-volume growth. Our modelling identifies the break-even horizons for typical modernization projects under multiple price and input-cost scenarios.

- Procurement and working-capital optimization: Fertilizer and soil conditioner spend continues to be a material line item for crop producers — U.S. crop farms alone spent an estimated USD 28.4 billion on fertilizer, lime and soil conditioners in 2024 — creating both demand stability and procurement leverage for large buyers. The report provides procurement playbooks and hedging approaches tailored to bulk lime flows.

- Regulatory and quality risk management: Certification and state-level labelling requirements (examples from Minnesota and New York) are shaping commercial access and product acceptance. Companies that integrate rigorous testing and certification into their commercial funnels avoid time-consuming disputes and open premium channels.

- ESG and decarbonization strategy: With kiln fuel costs and emissions under scrutiny, the economics of electrification, alternative fuels and modular carbon capture are now determinative for long-term competitiveness. Our pathways map capital, operating and policy levers for decarbonization.

- M&A and portfolio redesign: The industry’s mid-to-high concentration creates attractive consolidation opportunities — smart buyers will prefer asset-level due diligence tied to quality of reserves, kiln efficiency and logistics advantage. The report’s M&A taxonomy and target scorecards reduce execution risk.

What the Lime Market report delivers (practical components)

- Proprietary market sizing and validation methodology (base-year 2025 alignment, 2020–2025 historical reconciliation, and 2026–2032 scenario outputs).

- Demand-driver analytics: agricultural cycles, construction trends, mining/metallurgy demand, water treatment volumes and non-traditional uses — each with sensitivity to macro inputs (crop prices, infrastructure spend, commodity cycles).

- Supply-side cost curve and plant-level benchmarking: fixed/variable cost buckets, kiln fuel mixes, throughput assumptions, utilization sensitivity and a ranked list of performance improvements with payback windows.

- Regulatory and certification map: state-level licensing and testing requirements, product labelling obligations, and emerging cross-border compliance considerations for exporters.

- Competitive landscape and strategic positioning tools: CR3/CR5 concentration analysis, capability matrices for top producers, and an acquisition target screening framework.

- Commercial playbooks: pricing strategies, contract templates (indexation & escalation), channel economics for agricultural cooperatives and industrial offtakers, and buyer persona profiles.

- Scenario analysis and stress testing: base case (CAGR 2.5%), downside (macro shock / feedstock scarcity), and upside (accelerated infrastructure or water-treatment demand), with portfolio-level P&L impacts.

- Excel data annex and interactive dashboards: consolidated datasets used for modeling (note: detailed regional/application splits and company-level revenue tables are retained in the full report).

Competitive landscape — what to watch

The market shows a concentrated structure at the national and international levels (CR3 ~55%, CR5 ~75%), reflecting a mix of integrated global players and strong regional specialists. This concentration creates distinct strategic playbooks for incumbents, challengers and niche specialists.

Lime Market

- US Lime & Minerals, Inc. (Dallas, Texas) — Established producer with breadth across quicklime, hydrated lime and slurry products. Strengths include integrated supply to agriculture and industrial channels; watch for digital improvements in logistics and product traceability as differentiators.

- Mississippi Lime Company (Bonne Terre, Missouri) — Known for technical-grade and dolomitic lime production. The company’s 2025 investment in a sustainable kiln operation signals industry momentum toward lower-carbon assets and indicates how capacity renewals can be framed as both operational and ESG investments.

- Carmeuse Lime Inc. (Pittsburgh, Pennsylvania) — Strong play in agricultural limestone and soil conditioning; its global network suggests playbooks for moving higher-value product categories and providing agronomic services alongside the commodity.

- New Enterprise Stone & Lime Co., Inc. (Roaring Spring, Pennsylvania) — Regional leadership in aglime with deep customer relationships; an example of how localized quality and service excellence protect margins despite commoditization.

- Pete Lien & Sons, Inc. (Sheridan, Wyoming) and Cheney Lime & Cement Company (Cheney, Washington) — Solid regional suppliers that benefit from proximity to agricultural demand centers and unique feedstock sources; critical partners for distribution network optimization.

- Graymont Limited (Toronto) and Lhoist Group (Brussels) — International players with resources to invest in low-carbon technologies and cross-border market strategies. Their moves will set benchmarks for pricing and premium product development.

- American Crystal Sugar Company (Crookston, Minnesota) — An example of circular feedstock use — beet pulp and by-products being certified (Minnesota) for agricultural liming highlights downstream value capture opportunities for processors and co-product owners.

- Linwood Mining & Minerals Corporation (Linwood, Missouri) — Representative of quarry-led players with control over raw material quality; these companies play a pivotal role in supply security.

Regulatory and operational dynamics shaping 2026

- State-level certification and labelling regimes (recent activity in Minnesota and New York) are increasing the bar for product acceptance in both agricultural and municipal channels. Producers that invest early in testing infrastructure and brand-compliant documentation gain privileged access to institutional buyers.

- Some states are reducing reporting burdens (examples include program changes in Ohio and Vermont), creating a patchwork of obligations that complicates multi-state commerce — compliance-driven segmentation can be a source of competitive advantage.

- Quality metrics (such as calcium carbonate equivalent and effective neutralizing power) are becoming commercial differentiators rather than purely regulatory inputs. Buyers are willing to pay for predictable performance; producers that can document ENP and neutralizing power reliably will win share in premium channels.

- Recent facility investments — notably the 2025 kiln expansion program announced by Mississippi Lime Company — show the industry prioritizing sustainable operations as both a cost and market-access decision. Expect more announcements as companies convert sustainability commitments into capital programs.

Actionable strategic recommendations for 2026

- Adopt a three-horizon capex plan: prioritize short-cycle efficiency upgrades, medium-term fuel diversification, and long-term low-carbon kiln investments. Use scenario P&L overlays from our model to set investment triggers.

- Secure feedstock and co-product supply through long-term offtakes and partnerships (e.g., sugar processors, municipal treatment facilities) to de-risk price and quality volatility.

- Embed product quality certification into commercial offers. Invest in lab capabilities or trusted third-party testing to accelerate acceptance in regulated markets and premium ag channels.

- Pursue adjacency and capability M&A selectively — focus on logistics hubs, high-quality reserves, or hydrated-lime/water-treatment product lines that carry higher margin potential.

- Design customer contracts with transparent escalation clauses and quality specifications; this reduces commercial disputes and preserves margin in inflationary cycles.

- Launch pilot decarbonization projects today (fuel-switch pilots, electrification of ancillary processes, modular CCUS assessments) with clear KPIs and public reporting to attract financing and offtake partners.

- Invest in data-driven supply-chain visibility: demand signals from cooperatives, inventory hubs, and real-time logistics data reduce working capital and improve service levels to agricultural customers at peak planting seasons.

How PW Consulting can help

Our full Lime Market report provides the underlying datasets, regional & application splits, plant-level cost curve, company revenue tables and interactive scenario models that enable operational planning, M&A diligence and commercial negotiations. The research package includes a downloadable Excel annex, playbooks for procurement and regulatory compliance, and a bespoke briefing for C-suite and board teams.

Lime Market

For teams preparing investment cases, negotiating contracts with cooperatives, or drafting sustainability roadmaps, the full study converts market signals into executable steps and measurable milestones. The analysis in this primer intentionally summarizes the finding set; access to the detailed segment tables, company-level profiles and modelled scenarios is available through the Lime Market report page and bespoke advisory engagements.

PW Consulting stands ready to run a targeted workshop to translate these findings into a 90‑day action plan tailored to your portfolio. In a market characterized by steady demand growth, patchwork regulation and accelerating sustainability requirements, the difference between maintaining margin and expanding it will be defined by who moves first — and who moves with data.

For detailed analysis of this topic, please visit the official page:Lime Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com