Point-of-Care Molecular Imaging Devices Market Growth and Future Trends

Other |

2026-06-23 07:09:30

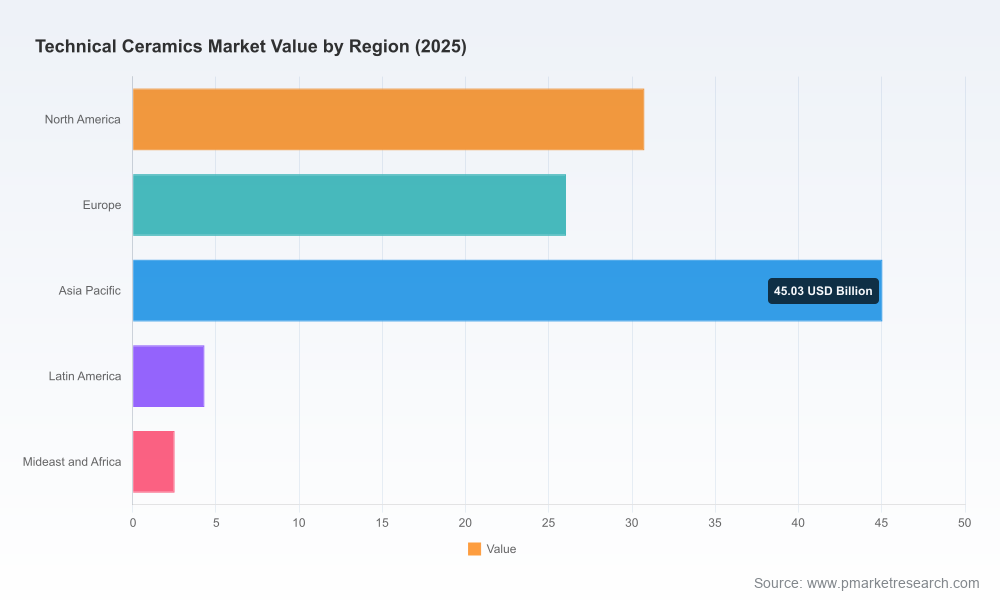

As firms position for the next cycle of capital allocation, product roadmaps, and M&A, technical ceramics are moving from a specialist materials category to a strategic lever across medical, energy, automotive, and semiconductor value chains. PW Consulting’s latest market study — with a 2025 base year and a forward look to 2032 — synthesizes five years of historical performance (2020–2025) and a scenario-based forecast for 2026–2032. The headline: the global technical ceramics market expands from roughly USD 76.4 billion in 2020 to USD 108.6 billion in 2025 and proceeds toward approximately USD 172.1 billion by 2032, tracking a mid-single-digit compound annual growth rate (CAGR) of 6.8% in the forecast window. This trajectory underscores a durable structural opportunity for firms that act with speed and precision in 2026.

Technical Ceramics Market

Timing of investment: 2026 is where macro growth and technology transition overlap. The market’s momentum to 2032 implies that near-term choices—capex for advanced sintering lines, partnerships for bioceramics prototyping, or capacity reshoring—will determine who captures disproportionate share during the next expansion phase.

Technical Ceramics Market

Regulatory and standards risk: New and evolving medical and device standards increase time-to-market and compliance cost. Our study maps the regulatory topology (including biological evaluation requirements and implant standards) that materially affect product launch windows and capital planning for 2026.

Technical Ceramics Market

Competitive positioning: With measured concentration at the top (our concentration metrics indicate a modestly fragmented supplier base), there is strategic room for focused players to scale through specialization or consolidation. The report supplies decision frameworks for select inorganic plays versus organic capability build-outs.

Macro growth is not uniform; it reflects a convergence of demand drivers (miniaturization and reliability in electronics and semiconductors, biocompatibility needs in medical devices, thermal and wear resistance in power and automotive sectors) and supply-side constraints (raw material purity, precision manufacturing costs, and highly specialized sintering infrastructure). The headline CAGR of 6.8% to 2032 indicates a healthy expansion, but beneath that figure lies a divergence of margin profiles and volume elasticity across product tiers. For 2026, the practical implication is that revenue growth alone will not guarantee profitability—manufacturers and OEMs must optimize mix, vertical integration, and service-enabled offers.

Advanced materials R&D: Developing next‑generation compositions (e.g., high‑performance zircons, engineered hydroxyapatites) yields premium pricing and defensibility, but requires sustained R&D and regulatory readiness. The study identifies the development timelines and regulatory checkpoints that buyers should budget into 2026 roadmaps.

Manufacturing scale and precision: Investments in precision sintering and contamination control are high fixed-cost items; our sensitivity analysis shows that modest improvements in yield and cycle time can unlock outsized margin gains—critical for 2026 capital allocation prioritization.

Regulatory assurance and productization: For firms targeting medical and dental device segments, alignment with biological evaluation standards and implant-specific norms is non-negotiable. Case examples in the report (including recent regulatory milestones) illustrate pathways to accelerate clinical adoption without sacrificing compliance.

Services and integration: Companies that couple materials supply with design-for-manufacturing services, rapid prototyping, and regulatory support capture stickier customer relationships—an increasingly important differentiator in 2026 procurement decisions.

The technical ceramics industry combines legacy specialists with emerging regional champions. Our competitive analysis synthesizes company profiles, strategic moves, and capability maps to help executives spot partners, acquisition targets, and benchmark peers.

CeramTec GmbH (Plochingen, Germany) — Recognized for medical-grade technical ceramics and established product families used in orthopaedic and dental applications. CeramTec’s lineage in implant materials positions it as a reference for clinical-grade performance and long-term reliability. (https://www.ceramtec-medical.com/en/)

Morgan Advanced Materials — Technical Ceramics (United Kingdom) — A provider of hermetic, biocompatible ceramic assemblies for surgical instruments and instrumentation. Morgan’s systems-level capability is relevant to OEMs seeking integrated components with demanding environmental tolerances. (https://www.morgantechnicalceramics.com/en-gb/)

Bloomden Bioceramics Co., Ltd. (Changsha, China) — A fast-moving participant in dental zirconia blanks and pre-shaded materials with recent product upgrades and regulatory milestones. Bloomden’s catalog refreshes and regulatory clearances demonstrate how agile product development and regulatory engagement can accelerate access to clinical markets. (https://www.bloomden.com/)

Himed (Old Bethpage, New York, USA) — Supplies hydroxyapatite powders and coatings and has invested in collaborative centers to shorten prototyping cycles. Himed’s facility certifications underline the importance of accredited manufacturing for implantable materials. (https://www.himed.com/)

CAM Bioceramics BV (Leiden, The Netherlands) — A contract manufacturer with flexible density and particle-size capabilities for orthopaedic and dental implants, relevant to firms seeking outsourcing partnerships for regulated product runs. (https://cambioceramics.com/)

CoorsTek Inc. (Golden, Colorado, USA) — Offers custom implantable ceramics and technical components, and stands out for high-performance ceramic product engineering across devices. (https://www.coorstek.com/)

Recent corporate and regulatory developments in the sector serve as practical signposts for decision-makers in 2026. Examples include product catalog upgrades and FDA engagements that materially alter market access timelines and competitive dynamics:

Bloomden rolled out multiple upgraded zirconia block lines in early 2025 and later secured regulatory clearance for several dental zirconia blanks in March 2026—an outcome that reshapes go-to-market timing for dental CAD/CAM applications.

Himed advanced a partnership model in 2024 to create an integrated bioceramics center combining rapid prototyping and analytical services, a blueprint for how service-enabled offerings can accelerate customer development cycles.

Cost structure sensitivities: High material purity requirements and precision processing drive production costs. Cost pressures limit penetration into price-sensitive segments unless offset by differentiated performance or integrated services.

Regulatory complexity: Standards for implantable ceramics and biological evaluation require lead time and capital to comply. Firms must incorporate compliance timelines into product development milestones and supplier selection criteria.

Fragmentation vs. consolidation: Quantitative concentration metrics show a market where the top few vendors do not dominate completely, leaving strategic space for both niche specialists and acquisitive platforms. For 2026, executives should treat M&A as an extension of capability build-out rather than purely revenue grab.

Supply chain resilience: Critical raw materials and specialized equipment can create single points of failure. The report provides supplier-mapping and contingency scenarios to inform 2026 sourcing playbooks.

The full study is designed for action. It contains:

A transparent forecasting engine with base-year reconciliation (2020–2025 historicals), scenario runs for 2026–2032, and sensitivity testing for raw material, cycle time, and regulatory delay variables.

A decision matrix for capex prioritization, contrasting capacity expansion, precision equipment upgrades, and automation, with IRR and payback modelling under conservative and aggressive demand scenarios.

An M&A target-screen with scoring across technological fit, regulatory readiness, customer overlap, and integration risk—built to accelerate due diligence and reduce execution risk.

Regulatory playbooks and compliance checklists aligned to international standards and biological evaluation requirements to support product roadmaps and clinical timelines.

Commercial strategy templates: pricing sensitivity guides, channel selection frameworks, and service bundling strategies that translate material performance into durable margin capture.

Competitive benchmarking dossiers on the leading players listed above, including capability maps, recent strategic moves, and suggested countermeasures for incumbents and challengers.

Prioritize shortlists: Use the report’s capability-fit matrices to narrow capital projects and partnership targets that must be decided in 2026.

Model regulatory timelines: Translate the regulatory playbooks into calendar milestones and budget reserves to prevent launch slippage and cost surprises.

Stress-test supply chains: Implement the supplier-mapping and contingency scenarios to validate single-source dependencies and to quantify the insurance value of dual sourcing or strategic inventory.

Design M&A pathways: For acquirers, apply the target-screen to identify acquisitions that buy critical capabilities with manageable integration risk; for targets, prepare to demonstrate certified process control and regulatory readiness to maximize valuation.

Technical ceramics are no longer an obscure materials niche; they are a cross-industry performance enabler where strategic choices made in 2026 will determine market position through 2032. PW Consulting’s study combines market-scale visibility, a practical toolbox for execution, and competitive intelligence to convert market growth into sustainable value. For executives preparing budgets and product roadmaps in 2026, the study’s forecasts, regulatory mapping, and deal-ready frameworks are purpose-built to reduce uncertainty and accelerate value capture.

To access the segmented demand matrices, regional and application-level scenarios, and downloadable due-diligence assets that inform these recommendations, please consult the full report on our website. The preview above is intentionally focused on strategic direction; the complete datasets and granular split analyses are available in the full PW Consulting Technical Ceramics Market report.

For detailed analysis of this topic, please visit the official page:Technical Ceramics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com