Mind-Body Techniques for Chronic Pain Relief at Home

Health |

2026-04-22 06:20:40

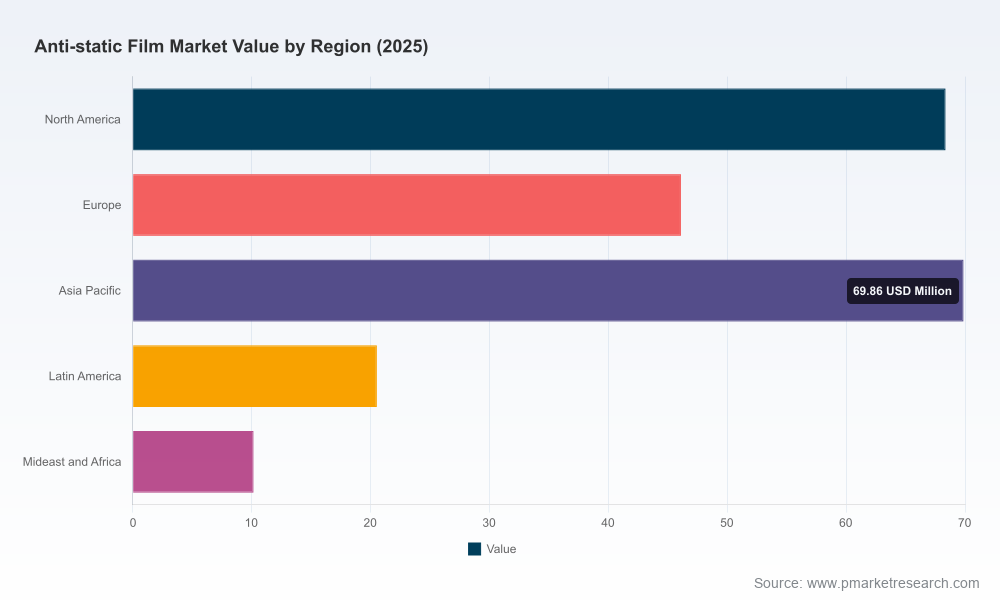

As global supply chains and end‑markets wrestle with electrification, miniaturization and stricter sustainability mandates, the anti‑static film market is entering a phase of measured expansion and structural re‑rating. Our new market study (base year 2025, forecast 2026–2032) shows the industry continuing a steady climb from a mid‑market base, expanding at a compound annual growth rate of 6.98%. From 2020 through 2025 the industry demonstrated resilient demand patterns; under our central scenario the market grows from roughly USD 215 million in 2025 to an expected USD 345 million by 2032 (USD, Million). This preview explains why that trajectory matters for corporate decision‑makers in 2026, what operational levers will drive outcomes, and how to use the full study to convert insight into action.

Anti-static Film Market

Procurement and sourcing strategies are at an inflection point. Raw material cost volatility and heightened trade measures mean purchasing teams must move beyond supplier price lists to actively manage input risk and certification compliance.

Anti-static Film Market

Product and packaging leaders must reconcile functional protection (ESD performance, barrier properties) with new sustainability and traceability expectations; regulatory changes in 2026 materially raise the cost of non‑compliance and the commercial value of certified recyclability.

Anti-static Film Market

M&A and investment choices hinge on careful mapping of capability gaps — in specialty PET formulations, cleanroom‑grade manufacturing, and biodegradable static‑dissipative solutions — all of which carry different margin and capital intensity profiles.

The headline growth rate (6.98% CAGR into 2032) is not merely arithmetic: it reflects a market balancing healthy end‑use demand from electronics, pharmaceuticals and precision manufacturing with cost and regulatory headwinds. The market’s historical progression into 2025 demonstrates steady underlying demand and room for premiumization, while the forecast path to 2032 implies sustained investment in differentiated materials (e.g., specialty PET, engineered PE blends and functional coatings) rather than commoditization.

For executives, the two practical implications are clear: (1) time‑phased investment in upstream capabilities (additive compounding, cleanroom extrusion, in‑line coating) will protect margins in a rising‑cost environment, and (2) strategic commercial segmentation — by end‑use performance, not just geography — will unlock premium pricing and deeper customer partnerships.

Proprietary market sizing and a 2026–2032 forecast model with scenario toggles. Buyers and strategists can stress‑test outcomes under alternate raw material and regulation pathways.

Value‑chain heatmaps and cost‑build templates showing where margin pools sit today and how they shift with resin prices, additive costs and tariff impacts.

Practical playbooks: supplier segmentation and scorecards, procurement negotiation levers, go‑to‑market tactics for premium ESD film propositions, and a prioritized roadmap for capex and capacity expansion.

Regulatory and sustainability readiness checklists aligned to 2026 compliance thresholds (including traceability certification frameworks), plus a carbon and circularity impact calculator for packaging teams.

Deal origination resources and an M&A radar: target profiles, valuation benchmarks and integration pitfalls for buyers seeking scale or technical differentiation.

The anti‑static film arena is structurally fragmented, with the top three players accounting for roughly a quarter of market share and the top five still representing only a little more than that — a configuration that favors nimble innovation as much as scale advantages. That fragmentation creates opportunity for specialists and regional champions to capture high‑value niches, particularly where cleanroom certification, custom formulation or medical‑grade quality are required.

Key industry actors reflect a mix of regional specialists and global technology providers. Several firms have built value propositions around polyethylene anti‑static systems tailored to electronics and cleanroom environments, while others emphasize engineered polyester (PET) films for semiconductor and medical packaging applications. Market leaders differentiate along three vectors: formulation control (additives and in‑film conductive networks), process capability (co‑extrusion, biaxial orientation, coating), and service (custom bagging, cleanroom handling, validated sterility workflows).

Recent corporate activity signals two important strategic moves: (1) an acceleration toward sustainable ESD solutions and (2) convergent product features that pair static‑dissipative performance with ancillary protection such as corrosion inhibition or antiviral surfaces. These moves are reshaping supplier value propositions and buyer selection criteria.

Sustainable ESD launches: Some suppliers have extended biodegradable and compostable static‑dissipative lines, catering to electronics and automotive segments that are demanding lower lifecycle impacts.

Integrated functionality: New permanent ESD stretch films combining long‑lasting discharge protection with corrosion inhibition indicate a tilt toward multifunctional packaging solutions that reduce SKU complexity.

Antiviral + anti‑static hybrids: The introduction of antiviral anti‑static films for electronics packaging signals adjacent market opportunities (healthcare logistics, medical device packaging) for firms that can certify both protection and biocidal performance.

Three cross‑cutting dynamics will determine winners and laggards in 2026:

Raw material volatility: Significant polyethylene price swings and periodic supply constraints are increasing working capital needs and compressing time‑to‑market. Firms that implement hedging strategies, vertically integrate resins/additives, or develop lower‑cost alternative formulations will gain resilience.

Regulatory tightening and trade measures: New sustainability requirements (including traceability certifications) and ongoing antidumping reviews on PET imports raise compliance burdens and alter sourcing economics. Procurement teams must now evaluate total landed cost inclusive of compliance risk, not just unit price.

Tariffs and import controls: Emerging measures are already raising import costs for specialty resins and additives in some markets, prompting short‑term reshoring of critical capacity and longer‑term supplier diversification strategies.

Make raw material strategy strategic: Convert ad‑hoc spot buying into a layered procurement approach with contracted volumes, index‑linked pricing, and contingency stock aligned to critical SKUs.

Invest in certification and traceability: Prioritize RecyClass and similar traceability credentials that many customers will require in 2026 and beyond; certification acts as both a market gatekeeper and a pricing lever.

Pursue product convergence: Differentiate by bundling ESD performance with defensive features (corrosion inhibition, antiviral coatings) that reduce client vendor counts and increase switching costs.

Rationalize the portfolio: Use margin and demand elasticity analytics to pare commoditized SKUs and reallocate capacity to premium, certified, or specialty lines.

Prepare M&A playbooks: Identify targets that add technical capability (e.g., specialty PET) or regional production that mitigates tariff exposure; prioritize bolt‑ons that accelerate sustainability credentials.

This preview outlines the strategic forces reshaping the anti‑static film market and provides a tactical lens for decision‑makers in 2026. The full PW Consulting study contains the granular scenario models, segmented forecasts, supplier scorecards, and executable playbooks that procurement heads, product executives and corporate development teams need to convert macro insight into profitable action.

We deliberately withhold the detailed region‑by‑region and application‑by‑application breakdowns here to preserve the strategic exclusivity of the full analysis. If you are responsible for buying, sourcing, or building capability in anti‑static and specialty films, the complete report provides the concrete numbers, sensitivity runs and supplier evaluations required to justify investment and procurement decisions in 2026.

Contact PW Consulting to access the full study, scenario dashboards and our practitioner toolkits — or brief one of our senior strategists for a tailored workshop that applies the findings directly to your cost base, supply chain and product roadmap.

For detailed analysis of this topic, please visit the official page:Anti-static Film Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com