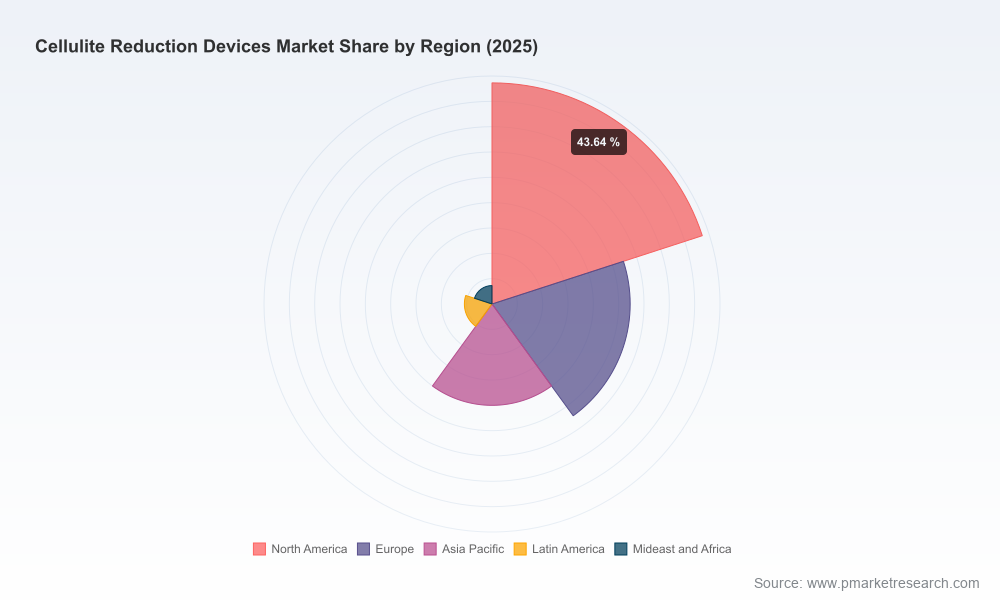

Cellulite Reduction Devices Market — Strategic Preview for 2026 Decision-Makers

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present an executive preview of our comprehensive Cellulite Reduction Devices Market study. This piece is designed as a strategic “trailer” for executives, investors, and corporate development teams preparing 2026 plans: it highlights the evidence-based trends, competitive dynamics, and decision frameworks contained in the full report while intentionally preserving proprietary segment-level findings to encourage full-report access.

Cellulite Reduction Devices Market

Macro snapshot: why this market matters in 2026

Between 2020 and 2025 the global market for cellulite reduction devices expanded materially, reflecting rising patient demand, broader acceptance of aesthetic procedures, and steady device innovation. Our base-year synthesis (2025) captures this acceleration: the addressable market doubled from early-decade levels and is projected to continue growing through the forecast window (2026–2032) at a compound annual growth rate of 11.3%. By 2032 the market is expected to be more than twice its 2025 size, a trajectory that creates meaningful commercial and strategic opportunities for device makers, distributors, private equity, and clinical operators.

Cellulite Reduction Devices Market

Report value: what decision-makers will get (and why it matters)

- Actionable market-sizing and forward scenarios calibrated to 2026 choices — including downside and upside adoption curves tied to reimbursement and regulatory outcomes.

- Commercial playbooks for product launches, channel expansion, and service models that reflect real-world provider economics and patient acceptance patterns.

- A detailed competitive heatmap and capability matrix covering established device OEMs, emergent technology entrants, and adjacent therapy providers.

- Regulatory and reimbursement pathway roadmaps with decision triggers — helping prioritize investments in clinical trials, labeling strategies, and geographic market entry sequencing.

- M&A and partnership candidate screening filters and integrated valuation sensitivities aimed at helping acquirers differentiate between strategic assets and commodity plays.

These deliverables are structured for near-term execution (12–18 months) and strategic planning (2–6 years). The full report includes models, templates, and playbooks that we use with clients to convert insight into executable plans; this preview surfaces the strategic implications without disclosing the proprietary split-level figures that underpin our recommendations.

Cellulite Reduction Devices Market

Competitive landscape — what to watch in 2026

The market exhibits moderate concentration: the top three players account for a notable share of commercial revenues, while the top five approach a plurality. That structure creates room for differentiated entrants but also signals increasing competitive intensity around clinical claims, provider economics, and service footprints.

- Venus Concept (Canada) — Strengths: strong platform strategy with RF-based body-contouring systems cleared for non-invasive cellulite reduction; strengths in channel partnerships with medspa and dermatology networks. Strategic focus for 2026: scaling consumables and subscription services to improve recurring revenue.

- Lumenis (Israel) — Strengths: established RF portfolio with broad clinical indications and recognized brand equity among physicians. Strategic focus: consolidating top-to-toe device positioning with clinical evidence that supports multi-indication utilization.

- InMode (Israel) — Strengths: technology innovation and modular platforms; recent 2025 launch pairing RF with acoustic technology underscores a push toward differentiated efficacy claims. Strategic focus: leveraging platform modularity to accelerate cross-sell.

- Cynosure / Syneron (United States) — Strengths: recognized devices cleared for temporary cellulite appearance improvement and integrated channel presence. Strategic focus: defend installed base while optimizing consumable economics and physician training programs.

- Sofwave Medical (Israel) — Strengths: ultrasound-based approach recently cleared for cellulite appearance improvements. Strategic focus: establishing claims differentiation where downtime and comfort are decision drivers.

- RESONIC (Allergan Aesthetics, AbbVie) — Strengths: rapid acoustic pulse technology with long-term appearance improvement claims; strong corporate backing. Strategic focus: leveraging global marketing muscle to accelerate adoption in aesthetic clinics and hospitals.

- Merz Aesthetics (United States) — Strengths: minimally invasive subcision (Cellfina™) with durable outcomes; established relationships with surgical and aesthetic specialists. Strategic focus: positioning subcision as the premium, durable option for specific patient segments.

- LPG Systems (France) — Strengths: mechanical solutions with long regulatory track record in non-energy devices. Strategic focus: defend mechanotherapy niche through service and training differentiators.

Across these competitors, 2025–2026 activity has emphasized regulatory clearing, product launches, and cross-technology pairing. Notable recent developments documented in the industry timeline include new international clearances and device launches that expand the technology mix available to clinicians. These moves are accelerating the market’s maturation and changing the argument set for purchasers.

Technology and clinical dynamics shaping 2026 strategy

- Technology bifurcation: Non-invasive energy-based technologies (radiofrequency, ultrasound, acoustic pulses) are the dominant approaches for zero-downtime treatments and rapid clinic throughput. Minimally invasive subcision remains important for patients seeking longer-lasting structural correction.

- Clinical evidence as gatekeeper: Regulatory clearances are necessary but not sufficient; differentiated clinical outcomes and real-world effectiveness data determine provider uptake and payer consideration.

- Reimbursement and access constraints: Cosmetic indications currently carry limited reimbursement support in most healthcare systems, constraining adoption to elective spenders and cash-pay clinic networks — a structural limit that influences pricing strategy and channel choice.

- Provider economics: Device selection is increasingly driven by total procedure economics (device throughput, consumables, training burden, and patient satisfaction metrics) rather than singular efficacy claims.

Risks and executional pitfalls

- Commoditization risk: As multiple vendors claim incremental efficacy gains, price erosion and margin compression become material unless vendors can capture recurring revenue or unique clinical positioning.

- Evidence and labeling mismatch: Investing heavily in commercial rollout before securing robust, comparative evidence risks retraints on adoption and future reimbursement opportunities.

- Service and training underinvestment: Many devices require operator sensitivity to achieve outcomes; insufficient post-sale support undermines satisfaction and referral generation.

- Regulatory and geographic variability: Different clearance requirements and timelines across markets mean that geographic expansion must be sequenced against regulatory milestones.

Practical decision framework for 2026

For corporate leaders preparing budgets and strategy cycles in 2026, the following prioritized actions will materially affect outcomes:

- Near term (0–12 months): Tighten evidence roadmap — fund pragmatic comparative studies and real-world evidence generation that target the specific clinical endpoints purchasers value. Lock in commercial pilots with high-throughput clinics to validate provider economics.

- Medium term (12–36 months): Build a differentiated monetization model — combine device sales with service, training, and consumable contracts to convert one-time sales into recurring revenue streams. Consider selective geographic rollouts tied to regulatory wins and high-population, high-out-of-pocket markets.

- Strategic / M&A focus (24–48 months): Use M&A and partnerships to acquire missing capabilities: evidence generation teams, regional distribution reach, or complementary technologies (e.g., pairing energy-based with mechanical subcision approaches).

- Organizational priorities: Ensure your commercial force is clinically fluent; invest in data capture infrastructure; and build a clear value argument for clinic administrators, not just clinicians.

How PW Consulting’s report supports execution

Our full market study provides the calibrated inputs and operational tools that turn the above frameworks into deliverables you can use in a boardroom or commercial planning session: revenue models with sensitivity to adoption drivers, go-to-market playbooks segmented by clinic type, an evidence prioritization matrix, due diligence templates for M&A, and a competitive scorecard that ranks companies across technology, evidence, and channel control.

Importantly, while this preview shares the market trajectory and strategic implications, the full report contains the granular segmentation, regional adoption curves, unit economics, and benchmarking tables that underpin our recommendations. Those data are intentionally reserved for report subscribers to preserve analytic IP and to ensure clients receive the full operational value necessary for confident decision-making.

Conclusion — the strategic inflection for 2026

The cellulite reduction devices market is at an inflection point: accelerating innovation, selective regulatory clearances, and evolving provider economics are making 2026 a pivotal year. Organizations that align investment in evidence, commercial execution, and recurring-revenue models will capture disproportionate value as the market matures. Conversely, actors who treat this as a point-solution market risk commoditization and margin erosion.

If your 2026 planning includes product launches, geographic expansion, M&A, or strategic partnerships in aesthetic devices, PW Consulting’s full report provides the detailed maps and operational tools you need. Access to the complete dataset and models will transform the strategic directions outlined here into concrete, financially-sound initiatives — and that is precisely the distinction this market demands.

For detailed analysis of this topic, please visit the official page:Cellulite Reduction Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com