Dental Gypsum Market — Strategic Briefing for 2026 Decision-Making

By PW Consulting — Senior Strategy Advisor & Lead Industry Analyst

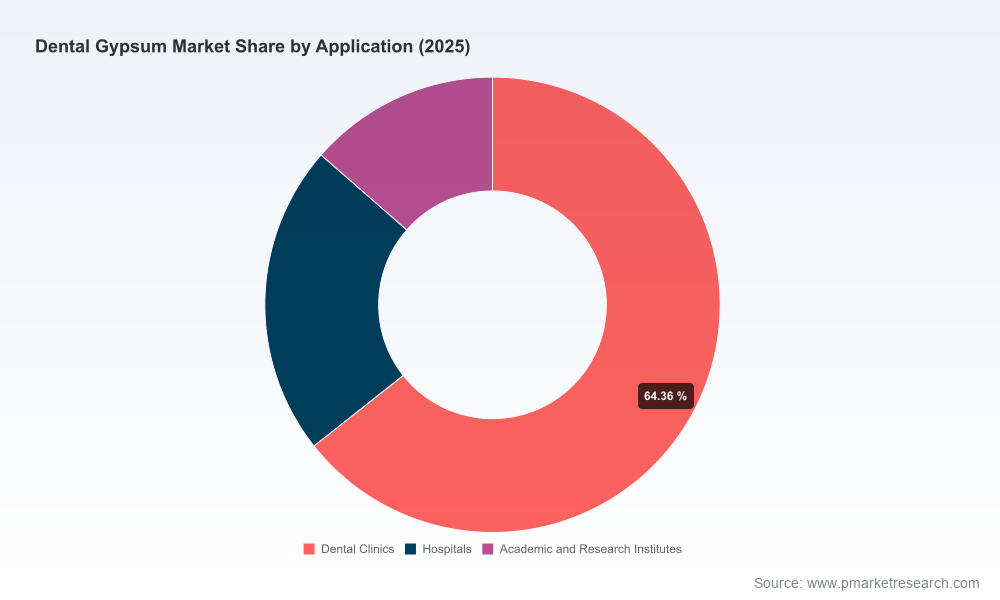

Dental Gypsum Market

Executive snapshot

The dental gypsum market has entered a period of orderly expansion following a mid‑decade rebound. Our base-year calibration (2025) and extended historical series (2020–2025) show the market increasing from approximately USD 95 million in 2020 to about USD 118 million in 2025. Under the baseline forecast the market grows at a compound annual growth rate (CAGR) of roughly 4.8% through the 2026–2032 planning horizon, reaching an estimated USD 164 million by 2032 (all figures in USD Million). These macro dynamics, combined with a moderately consolidated supplier landscape (CR3 ≈ 35%, CR5 ≈ 48%), create a predictable but competitive environment for manufacturers, distributors and clinical technology integrators.

Dental Gypsum Market

Why this research matters for 2026 strategic choices

- Timing investments: The forecasted steady growth and projectable demand profile enable capital planners to stage capacity additions, automate set‑line operations, and prioritize product lines with less risk of near‑term overcapacity.

- Regulatory certainty: With dental gypsum recognized as a Class II medical device under FDA guidance and governed by ISO standards for setting characteristics and biocompatibility, compliance timelines and certification costs must be incorporated into any go‑to‑market timetable.

- Competitive positioning: The market’s moderate concentration suggests room for both incumbent scale plays and focused niche strategies. Strategic moves (premium quality vs. cost leadership, color/setting differentiation, or clinical‑validated biocompatibility claims) will materially affect margin outcomes.

- M&A and partnership design: Predictable headline growth and fragmented mid‑tier competition create windows for bolt‑on acquisitions or distribution alliances intended to climb the CR curve without courting regulatory or anti‑trust pushback.

Market trajectory and what it implies

Across the historical 2020–2025 window the market recovered from pandemic‑era disruption and moved into a structurally growth phase. The projection to 2032 at a ~4.8% CAGR reflects a combination of steady procedural volumes in clinical dentistry, replacement demand from laboratory workflows, and incremental consumption driven by educational and research institutions modernizing their facilities.

Dental Gypsum Market

For executives, the implication is straightforward: this is not a hyper‑growth, winner‑takes‑all market, but neither is it a declining commodity. Tactical decisions that optimize operational efficiency, ensure regulatory alignment, and create product differentiation (performance, handling characteristics, or clinical validation) will generate outsized returns relative to peers who treat gypsum as a low‑touch commoditized input.

Regulatory and reimbursement context — operational impacts

- Device classification: Dental gypsum is classified as a Class II medical device in the US, with applicable FDA device listings and pathways (510(k) where required). Organizations must account for third‑party review options that reference recognized standards for dental materials.

- Standards and testing: Compliance with ISO 6873 (setting time, expansion, compressive strength) is table stakes for market access in many jurisdictions. ISO 10993 biocompatibility testing is also required where gypsum components interface with patient tissues or are part of prosthetic workflows.

- Reimbursement environment: While consumables like gypsum are generally claimed through dental billing processes, no material changes to CPT/DRG frameworks for gypsum have been observed. Operationally, this means product adoption decisions rely primarily on clinical preference, laboratory economics and procurement arrangements rather than direct reimbursement incentives.

Demand drivers and structural forces

- Clinical and lab throughput: The core demand engine remains restorative and prosthodontic procedures and the laboratory workflows that support them. Capacity planning in manufacturing should be aligned to observable clinic and lab utilization trends rather than short‑cycle promotions.

- Digital substitution pressures: The rise of intraoral scanners, CAD/CAM and additive manufacturing creates a long‑term structural headwind for some gypsum applications, while simultaneously opening opportunities for hybrid workflows where gypsum remains relevant (e.g., verification models, splint fabrication, teaching labs).

- Product performance differentiation: Speed of set, dimensional accuracy, and handling characteristics continue to be primary purchase criteria. Manufacturers that invest in R&D to tune these attributes—while maintaining compliance—can command premium positioning.

- Supply chain resilience: Raw gypsum sourcing, calcination processes, and regional logistics are operational levers. Companies with diversified feedstock or integrated calcination capabilities will demonstrate shorter lead times and better margin stability during commodity price swings.

Competitive landscape — strategic profiles

The market comprises a mix of global specialty materials players and regionally focused manufacturers. Below are high‑level strategic assessments of several prominent participants (illustrative, non‑exhaustive):

- USG Corporation (Chicago, IL, USA) — Broad portfolio and distribution reach; leverages a range of formulations for impression and laboratory use. Strategic advantage: well‑known industrial scale and channel relationships.

- Whip Mix (Louisville, KY, USA) — Deep furnishings for dental labs and universities with comprehensive product families. Strategic advantage: reputational strength with technical customers and educational institutions.

- Garreco (Heber Springs, AR, USA) — Emphasizes US‑manufactured product lines with configurable set times and color options; recent catalog refresh (June 2025) expanded transparency around SKUs. Strategic advantage: agility and made‑in‑market messaging.

- ETI Empire Direct (Anaheim, CA, USA) — Focus on differentiated products (e.g., colored die stones) and direct distribution. Strategic advantage: direct‑to‑clinic channel and price/promotion flexibility.

- Saint‑Gobain Formula (Walkenried, Germany) — Strong compliance focus with ISO 6873 alignment and established European presence. Strategic advantage: trusted materials quality and regulatory pedigree.

- Heraeus Kulzer / Modern Materials (Hanau, Germany) — Combines legacy brand trust with specialty natural gypsum products; well‑placed for premium lab channels.

- Kerr Dental (Brea, CA, USA) — Legacy dental OEM with strong ties into restorative workflows; positions gypsum as part of an integrated materials portfolio.

- Dentona AG (Dortmund, Germany) — Niche technical differentiation (e.g., zero‑expansion formulations) that serve precision articulator and prosthetic applications.

- Yoshino Gypsum Co., Ltd. (Tokyo, Japan) — Offers calcined gypsum for clinical and denture forming; strategic strength in feedstock processing expertise.

Collectively, the top three players account for roughly a third of the market, while the top five approach half—an environment that rewards focused differentiation and selective scale plays.

Strategic imperatives for 2026

For market participants planning actions in 2026, we recommend a set of high‑leverage initiatives designed to convert the forecasted steady growth into durable competitive advantage:

- Prioritize regulatory readiness: Invest in ISO 6873 and ISO 10993 testing pipelines early. Incorporate regulatory timelines into product development roadmaps to prevent launch delays and to shorten time‑to‑revenue.

- Segment product portfolios: Separate commodity plaster offerings from premium, clinically validated stones. Protect margin by charging for demonstrable performance attributes and validated handling benefits.

- Hedge raw material risk: Pursue supply contracts or vertical integration options for calcined gypsum feedstock to stabilize costs and secure lead times.

- Pursue targeted M&A: Look for bolt‑on acquisitions that add formulation expertise, geographical distribution, or laboratory channel access—rather than pursuing large, transformational deals in this moderately concentrated market.

- Engage clinical and academic champions: Fund applied studies with leading dental schools and reference labs to generate independent performance data that supports premium claims and clinician adoption.

- Plan for digital coexistence: Develop product lines and marketing messages that position gypsum as a complementary technology to digital workflows rather than an either/or choice.

What PW Consulting’s full report delivers (operationally focused)

The complete Dental Gypsum Market study provides practitioners with the actionable tools needed to execute the recommendations above while preserving strategic confidentiality of granular segment shares. Key deliverables include:

- Market model (2020–2032) with scenario options—baseline, conservative, and accelerated—delivered in editable spreadsheets (USD Million; base year 2025).

- Regulatory and compliance playbook that maps certification routes, typical test batteries, estimated timelines and vendor selection criteria for ISO/biocompatibility testing.

- Supply‑chain heatmap and cost sensitivity analysis that identifies critical feedstock nodes and alternative sourcing strategies.

- Competitive scorecards and go‑to‑market strategies for incumbents, challengers and distributors (without publishing sensitive proprietary segment-level revenues in this summary).

- Commercial templates—pricing playbooks, tender response frameworks, and clinical validation study outlines—to accelerate commercialization.

- Opportunity matrix highlighting high‑ROI initiatives (product upgrade, geographic channel expansion, targeted M&A) and a prioritized 24‑month implementation roadmap.

Next steps and how to use this briefing

Use this briefing to align your 2026 capital and product plans around predictable demand and regulatory realities. If your board is weighing manufacturing investments, M&A, or R&D prioritization, the full PW Consulting study supplies the granular datasets, scenario tools, and regulatory checklists required to finalize budgets and project charters.

For procurement leaders, the study delivers supplier scorecards and negotiation levers. For product and R&D leads, it provides prioritized formulation targets and clinical validation protocols. For corporate development teams, it identifies high‑fit acquisition & partnership themes and the due diligence frameworks to de‑risk deals.

Invitation

This briefing is designed to demonstrate the depth and framing of PW Consulting’s Dental Gypsum Market study while preserving the detailed segment matrices that underpin our recommendations. To access the full dataset, detailed segmentation, and downloadable tools referenced above, please visit our report page or contact PW Consulting for a confidential briefing.

For detailed analysis of this topic, please visit the official page:Dental Gypsum Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com