Global iPaaS Market Growing at 27.1% CAGR Through 2032

Other |

2026-06-20 11:33:15

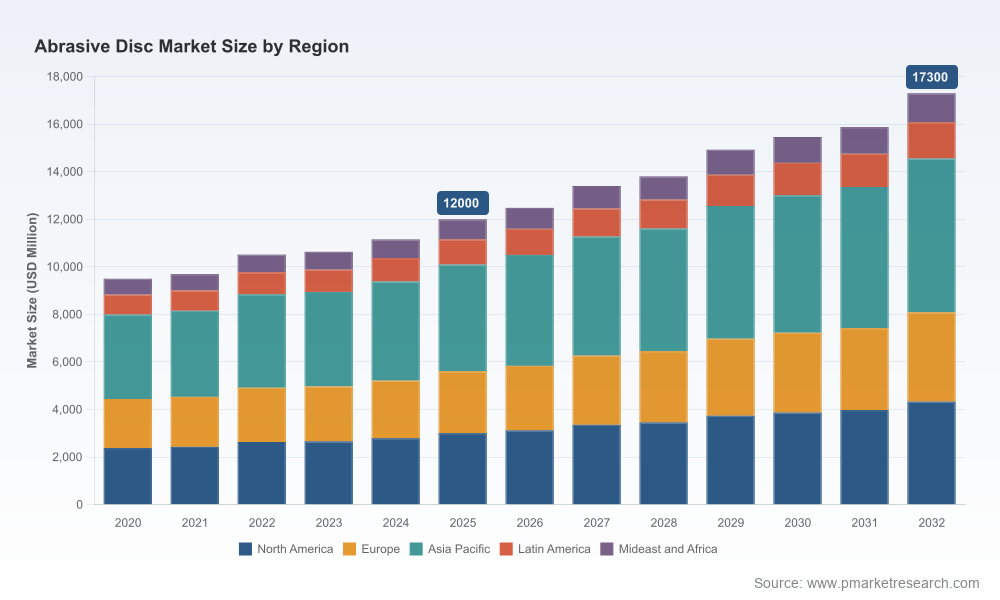

As PW Consulting’s lead industry analyst, I present a focused strategic preview of our new Abrasive Disc Market study — an operationally oriented resource tailored for executive teams, strategy leads, and corporate development groups planning for 2026. The global abrasive disc market demonstrated resilient expansion through the early 2020s, reaching approximately USD 12.0 billion in our base year (2025). Projected at a compound annual growth rate (CAGR) of 5.4% across the 2026–2032 forecast window, the market is expected to exceed USD 17.3 billion by 2032. Those headline metrics frame a market that is neither commodity-flat nor runaway-high-growth; instead, it is a mid-growth industrial goods sector where product innovation, supply-chain management, and compliance differentiate winners from the pack.

Abrasive Disc Market

Actionable, revenue-focused foresight: Our study translates macro growth forecasts into decision-ready guidance for product portfolio prioritization, pricing strategy, and capacity planning — critical inputs for budgeting cycles that begin in late 2025 and drive capital allocation in 2026.

Abrasive Disc Market

Supply chain and margin protection: With raw material volatility and resin/grain price shifts increasing margin pressure, the report provides scenario-based cost models and hedging levers suitable for both manufacturers and large industrial buyers.

Abrasive Disc Market

Regulatory and certification roadmap: New labeling, conformity, and EHS requirements across major markets are influencing go-to-market timelines. Our compliance timetable helps product teams sequence certification investments to avoid delayed launches or restricted access to key accounts.

M&A and partnership signal map: The market sits at a moderate concentration level (the top three players account for roughly mid-forties percent of market share; top five near-high-fifties percent). That structure supports bolt-on consolidation plays alongside continued competition from regional specialists — the study outlines target profiles and integration checklists.

Market sizing & forecast toolkit: A transparent model built on our historical analysis (2020–2025) and a granular scenario engine for 2026–2032, allowing you to stress-test assumptions around raw material cost trajectories, demand elasticity, and replacement cycles.

Go-to-market playbooks: Channel-by-channel strategies for professional distribution, OEM partnerships, and direct-to-professional accounts — including margin models, promotional frameworks, and volume thresholds for profitable scale.

Regulatory compliance checklist: A jurisdictional map of mandatory labeling elements and certification regimes, with suggested timelines and estimated approval lead times for new product introductions.

Competitive battlecards: Executive summaries for the industry’s leading manufacturers with key strengths, positioning, and likely strategic moves — useful for negotiation, partnership assessment, and competitive response planning.

Cost-to-serve analysis & procurement levers: Supplier segmentation, logistics vulnerability heatmaps, and contracting templates that procurement teams can use to reduce cost volatility and secure continuity of supply.

Innovation & product-roadmap accelerator: A prioritized list of R&D themes — from abrasive grain chemistry to backing materials and attachment systems — with commercial gating criteria and expected payback horizons.

M&A diligence checklist and valuation comparators: Practical templates for buy-side teams — synergy levers, integration risks, and a shortlist of target archetypes suited for vertical integration or geographic expansion.

The abrasive disc market is served by a mix of global incumbents and regionally strong specialists. Strategic moves by these players set the pace for product innovation, channel control, and sustainability signaling — all factors that will influence 2026 procurement and partnership decisions.

Klingspor (Germany): Strong in high-quality coated products and flap discs. Their European manufacturing footprint and emphasis on premium performance make them a relevant partner or competitor for firms targeting industrial OEM channels.

United Abrasives / SAIT (United States): Deep in industrial coated abrasives, with established relationships in fabrication, welding, and construction markets. Their distribution muscle matters for scale roll-outs in North America.

Flexovit Abrasives (United States): Known for non-woven and Type 29 formats, Flexovit’s product introductions accelerate category migration toward specialized finishing solutions favored by professional users.

Saint-Gobain Abrasives / Norton (US brand presence): A global brand with recent sustainability signaling — publishing Environmental Product Declarations — that sets a new benchmark for customers demanding lifecycle transparency.

3M Abrasives (United States): Technology-driven disc platforms (e.g., ceramic- and precision-engineered grains) that support higher throughput and longer life, appealing to OEMs and service providers looking to reduce total cost of ownership.

Specialist European and Asian manufacturers (VSM, Mirka, PFERD, Tyrolit, Bosch, Rupes, etc.): Each brings specific advantages — from precision finishing to tool-system integration and aftermarket reach — and their participation keeps market dynamics fluid.

Emerging North American and regional players (Bluerock, Preco, Carborundum Universal and others): Typically price-competitive and agile on customized formats, these companies are attractive acquisition targets or channel partners for rapid market entry.

Recent industry moves — trade show product debuts, new product introductions, and certification releases — underscore strategic themes we flag in the report: portfolio premiumization, platform-based product families, and sustainability credentials becoming procurement filters. For example, product launches and global trade show participation in early 2026 demonstrate that incumbents continue to invest in both new formats and visibility in fabrication and metalforming channels.

Raw-material and input-cost volatility: Resin systems and abrasive grain markets have shown cyclical price behavior. Firms that lock in multi-year supplier agreements, pursue backward integration for key inputs, or adopt adaptive pricing algorithms will protect margins in 2026.

Regulatory and certification complexity: Markets in Europe have tightened labeling and conformity expectations, making pre-launch compliance planning non-negotiable. Certification leadership (EPDs, FEPA engagement, EN conformity) is already being used as a market access and differentiation strategy.

Automation and precision finishing demand: As automotive, aerospace, and industrial manufacturing automate higher-value finishing operations, demand shifts toward higher-spec discs with consistent, predictable performance. This creates a tiered market: commodity low-cost discs vs. premium engineered systems.

Channel and service orientation: Professional distributors and OEMs increasingly require integrated service offers (technical training, warranty, and performance guarantees). Suppliers who bundle products with technical support secure higher retention and better pricing.

Sustainability as procurement filter: Customers are beginning to require lifecycle information and lower-environmental-footprint products. Early movers publishing verifiable environmental data benefit from reduced procurement friction with sustainability-driven buyers.

Prioritize certification and transparency: Invest in recognized environmental and safety certifications for flagship product lines to open doors with corporate buyers and institutional accounts.

Hedge raw-material exposure: Use a combination of contract length, supplier diversification, and selective backward integration for critical grain or resin inputs to stabilize gross margins.

Product tiering and channel alignment: Segment SKUs into commodity, professional, and premium tiers with clear service and pricing models; align sales incentives and distribution contracts accordingly.

Targeted M&A and partnerships: Use the market’s mid-range concentration to pursue bolt-on acquisitions that fill product gaps (e.g., non-woven finishing, fiber-backed discs) or unlock distribution networks in priority geographies.

Commercialize performance-based selling: Shift commercial conversations from unit price to total cost of ownership by quantifying abrasion life, cycle-time gains, and scrap reduction for high-value customers.

Invest in digital trade and aftermarket services: E-commerce for professional buyers, technical content for training, and analytics-driven reorder systems reduce cost-to-serve and increase wallet share.

The market profile in 2026 favors disciplined operators that combine product performance, regulatory compliance, and supply resilience. Institutional investors and corporate boards should evaluate targets and strategic investments against three tests: can the asset protect margins under raw-material stress; does it have access to professional channels or OEM contracts; and can it demonstrate credible sustainability credentials? The market’s moderate consolidation — with the top-three and top-five shares indicating meaningful incumbent presence but room for new aggregation — supports both organic and acquisitive routes to scale.

Our full report contains the precise segmentation, region/type/application splits, and detailed company-level metrics that many strategic initiatives require. In keeping with our “preview” approach, this article intentionally omits the granular split data to preserve the analytical value of the complete study. For teams preparing budgets or M&A pipelines in 2026, the full dataset, models, and playbooks are designed to be plug-and-play for strategic planning sessions.

PW Consulting’s abrasive disc study is engineered to move decisions from insight to action. If your 2026 plans involve portfolio reshaping, procurement rationalization, or M&A in abrasives or adjacent finishing technologies, the research provides the evidence base and tactical templates to execute with confidence.

For detailed analysis of this topic, please visit the official page:Abrasive Disc Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com