Is Mesotherapy Painful? What Patients Should Know

Health |

2026-06-23 13:03:31

As global manufacturers recalibrate supply chains, decarbonization plans, and product roadmaps, electrocoating (e-coat) has moved from a niche corrosion-protection technology to a strategic lever across automotive, industrial, appliance and emerging battery-related applications. PW Consulting’s new Electrocoating Market study (base year 2025) synthesizes five years of historical data (2020–2025) and an evidence-based forecast through 2032 to give leaders the decision-quality intelligence they need in 2026. The headline: the market—measured in USD Billion—has grown from a multi-year low point in 2020 to an estimated USD 4.47 Billion in 2025 and is forecast to reach approximately USD 7.08 Billion by 2032, implying a compound annual growth rate (CAGR) of roughly 6.8% across the forecast window.

Electrocoating Market

Convergence of structural drivers: Electrification of drivetrains, stricter corrosion and lifecycle requirements, and the proliferation of complex multi-material assemblies are increasing demand sophistication for e-coat chemistries and application systems. These trends amplify Total Addressable Market expansion even where unit growth is moderate.

Electrocoating Market

Supply-side reconfiguration: Tariff shocks and raw-material volatility in 2024–2025 have catalyzed nearshoring, capacity reallocation, and chemistry substitution—decisions that materially alter plant-level economics and sourcing strategies in 2026. The PW study embeds these adjustments in modelled supply curves and margin sensitivity analyses.

Electrocoating Market

Technology and sustainability pressures: Advances in binder design, low-temperature cure systems and functional electrodeposition (including conductive and battery-related coatings) are creating premium product tiers and new specification pathways between OEMs and tier suppliers.

Demand modelling calibrated to historical top-line performance (2020–2025) and forward-looking drivers—vehicle parc electrification, appliances replacement cycles, and industrial capex patterns—translated into scenario-ready forecasts through 2032.

Supply-side mapping and plant-level economics: a granular inventory of resin and coater capacity, proven versus brownfield expansion case studies, and an indexed capex calculator for greenfield versus retrofit investments. (Note: the public preview omits segmented capacity figures; these are in the full report.)

Cost-push and tariff stress tests: dynamic models that quantify input volatility (resins, pigments, pretreatment chemistries, steel/aluminum substrates) and the transmission mechanics of tariffs and reciprocal duties into customer pricing and margin recovery options.

Technology and chemistry scorecards: benchmarking of cathodic, anodic and functional electrodeposition systems across corrosion performance, process footprint, CO2 intensity and retrofit compatibility.

Commercial playbooks and procurement levers: tender templates, supplier segmentation approaches, and negotiation architectures tailored for OEMs, coil coaters, and captive paint shops.

M&A and partnership heatmaps: prioritized targets and capability gaps across coatings manufacturers, resin specialists and application-system integrators—scored on strategic fit, integration complexity and time-to-value.

Capacity planning: use the report’s plant-level build vs. buy economics to decide whether to expand resin production, add e-coat lines, or secure long-term offtakes with suppliers. Our models translate demand uncertainty into probabilistic utilization bands for each facility type.

Procurement and input-risk mitigation: the tariff and input-cost scenarios provide clear triggers for nearshore sourcing, dual-sourcing thresholds, and strategic inventory programs that preserve working capital while dampening price spikes.

Product development and specification strategy: the chemistry benchmarking helps R&D prioritize low-temperature cures, solids-in-binder tradeoffs, and functional coatings for battery enclosures—areas expected to influence bidding competitiveness in 2026.

M&A and partnerships: the heatmap identifies bolt-on targets that accelerate route-to-market or fill capability gaps (resin synthesis, pretreatment, application automation) with payback periods and integration risk profiles.

The electocoating landscape combines multinational coatings conglomerates, resin specialists, and regional formulators. The market remains fragmented: the top three players account for under one-third of the market, and the top five hold just over a quarter—signalling ample room for consolidation and differentiated growth strategies.

PPG Industries, Inc. — Pittsburgh-based PPG has been sharpening its e-coat portfolio, emphasizing cathodic and anodic resin technologies and system platforms marketed to automotive and appliances. Recent product introductions aim to move their revenue mix toward a higher proportion of sustainably advantaged solutions—an important factor for OEMs shifting supplier scorecards to include lifecycle emissions.

Axalta Coating Systems — Axalta’s strength in industrial liquid coatings extends into precision-driven e-coat solutions for automotive applications. Their go-to-market focus is on integration with OEM painting lines and performance repeatability—attributes that matter where warranty and reliability drive procurement decisions.

BASF SE — BASF’s CathoGuard® and related binder platforms underline the company’s strategy: secure raw-material supply chains, expand localized production and compete on high-performance resins. A notable 2026 development is the doubling of resin production capacity at a major Shanghai plant, accompanied by process enhancements targeting electrocoat binder output—an example of how geographic expansion can be timed to customer demand growth.

The Sherwin-Williams Company — Sherwin’s VECTROGARD™ suite targets corrosion protection and durability for industrial and appliance segments. Their competitive advantage is channel depth and an emphasis on end-to-end systems, from pretreatment through post-cure testing.

Nippon Paint Holdings — With a strong automotive coatings franchise, Nippon Paint is pushing E-coat binder innovations through its automotive coatings division, focused on OEM specifications across Asia and beyond.

AkzoNobel and Henkel — both remain relevant through niche competencies: AkzoNobel in coil and extrusion electrocoating solutions for industrial clients, and Henkel in functional coatings and conductive electrodeposition systems relevant to emerging battery and electrochemical applications.

BASF’s early-2026 capacity expansion in Shanghai (resin output) demonstrates how incremental increases in binder availability can tighten or loosen procurement leverage in local markets; companies structurally exposed to that geography should stress-test supply alternatives now.

PPG’s launch of next-generation electrocoating technologies (announced mid-2025) indicates a shift toward product differentiation on sustainability and performance—firms that delay specification updates may find themselves excluded from certain OEM panels.

Trade-policy volatility—US tariff adjustments on epoxy resins and pretreatment chemistries, and substantial increases in steel and aluminum duties (Section 232)—are not transitory. They have already triggered nearshoring and alternative-chemistry plays which materially affect sourcing costs and supply-chain lead times.

Two dynamics deserve explicit monitoring in 2026:

Trade and tariff volatility: recent changes to tariffs on key inputs (including epoxy resins, conductive pretreatment chemicals, and metal substrates) create a persistent risk of cost pass-throughs and procurement disruptions. Companies must model tariff scenarios into multi-year supplier contracts and price escalator clauses.

Transition risk from chemistry substitution: regulatory and OEM sustainability requirements are accelerating the move to lower-emission binders and higher solids. That transition creates winners and losers among resin suppliers and formulators depending on R&D lead times and scale-up capabilities.

Baseline (Central Case): Continued moderate demand expansion with embedded substitution. Recommended moves: prioritize retrofit investment options with flexible cure profiles; secure multi-year resin offtakes with price banding; upgrade specification checklists to include lifecycle metrics.

Supply-Shock (Tariff/Logistics Spike): Short-term input cost jumps and regional availability gaps. Recommended moves: activate contingency nearshoring plans, diversify supplier base by chemistry class, and convert fixed-cost elements to variable-throughput agreements where possible.

Green Acceleration (OEM Sustainability Push): Rapid adoption of low-carbon coatings and battery-related functional e-coats. Recommended moves: accelerate R&D partnerships, prioritize acquisitions that provide IP in low-temperature and conductive systems, and run pilot programs with key OEMs to lock in first-mover specification advantages.

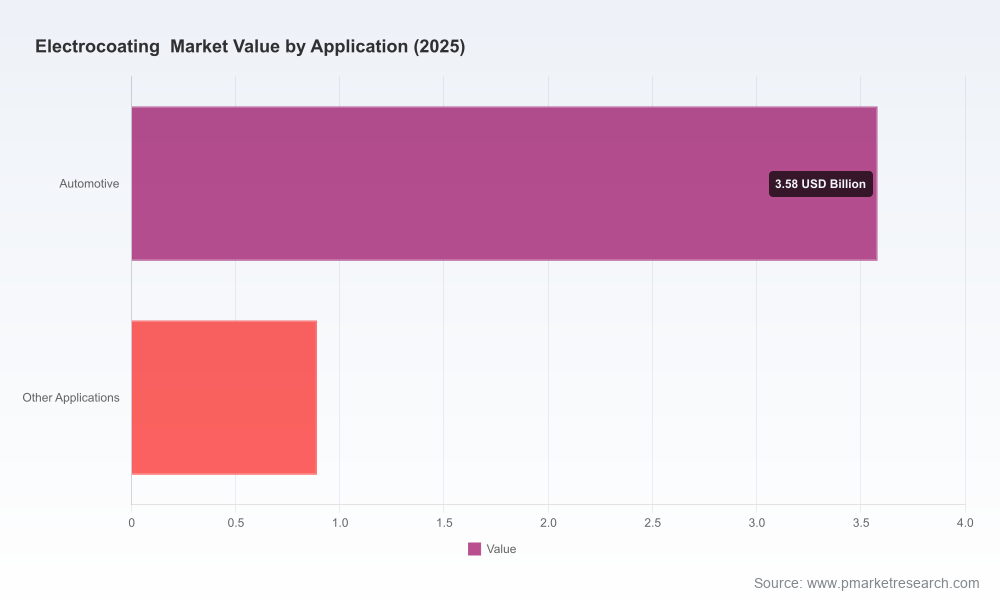

This preview demonstrates the type of strategic, executable insights PW Consulting delivers: integrated demand-supply modelling, supplier and plant-level economics, technology scorecards and commercial playbooks tied to real-world policy and commercial developments. We deliberately refrain from publishing granular regional and application-level splits in this executive preview to protect the integrity of the modelling and to ensure clients can act on exclusive, source-level intelligence. For procurement leaders, R&D heads, corporate development teams, and private-equity sponsors mapping next steps in 2026, the full report provides the calibrated levers, thresholds and negotiation-ready deliverables you will need.

Contact PW Consulting to access the full Electrocoating Market study and obtain the granular segment matrices, plant inventories and proprietary scenario outputs that underpin the 2026 playbook.

For detailed analysis of this topic, please visit the official page:Electrocoating Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com