Как сегодня производится проверка AML криптовалютного кошелька

Other |

2026-02-13 10:20:57

As PW Consulting’s Senior Strategy Advisor and Head Industry Analyst, I present a concise but deep industry briefing designed to equip C-suite and operational leaders with the strategic context they need for capital allocation, supply-chain choices, and product-technology roadmaps in 2026. This briefing draws from our full market study (base year 2025) that models historical dynamics (2020–2025) and provides a 2026–2032 forecast under multiple scenarios. The market in 2025 is measured at USD 3,050 Million, and our modeled baseline grows at a compound annual growth rate (CAGR) of 8.9% through the forecasting horizon — a trajectory that nearly doubles nominal market value by the end of the period. High-level concentration metrics show that the top three and top five suppliers account for a material but not dominant share of market revenues, signaling both established leadership and available whitespace for differentiated entrants.

Coordinate Measuring Machine (CMM) Market

Timing: 2026 is the inflection window where productivity-driven equipment upgrades intersect with technology maturation in multisensor probing, software-led workflows, and shop-floor automation. Firms that align procurement and service models to this window will capture outsized operational returns.

Coordinate Measuring Machine (CMM) Market

Capital allocation: With measurable market expansion and demonstrable ROI thresholds for precision measurement systems, boards must re-evaluate CapEx cadence, financing structures, and trade-off analyses between in-house metrology versus outsourced inspection services.

Coordinate Measuring Machine (CMM) Market

Supply-chain risk: Tariff regimes, commodity cost volatility, and skills shortages have moved from episodic to structural considerations. The full report quantifies landed-cost sensitivity and supplier concentration effects to support sourcing decisions and hedging approaches.

The market base in 2025 is USD 3,050 Million. Our central forecast — reflecting macro demand, technology adoption, and regulatory pressures — projects steady, near-single-digit growth (CAGR 8.9%) through 2032. The result is a larger, more diverse market by 2032 driven by intensified quality control demands across high-precision industries and accelerated adoption of integrated, digital metrology solutions.

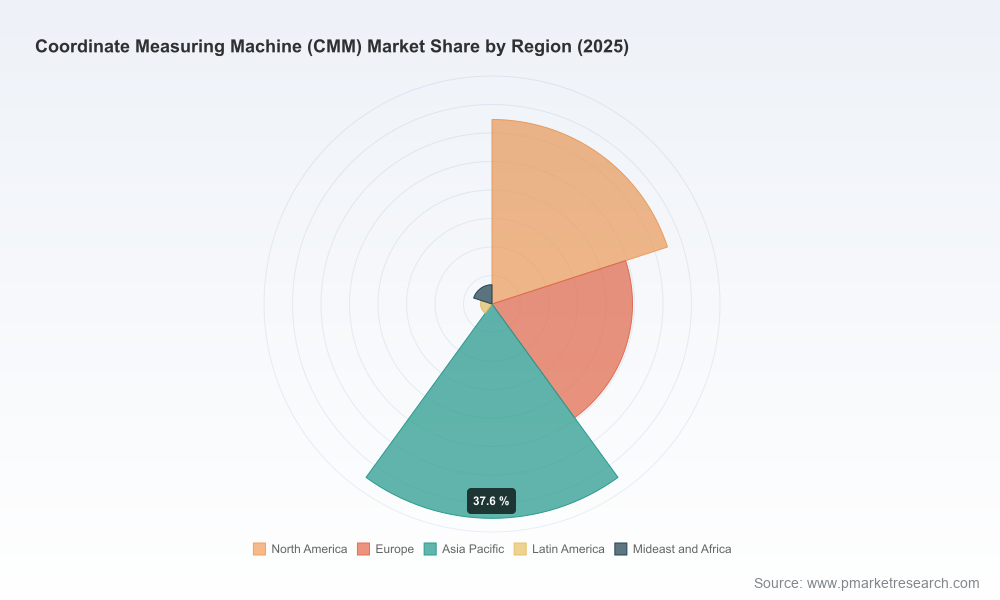

These top-line dynamics frame three strategic realities: first, buyers are increasingly evaluating CMM purchase decisions on total lifecycle cost and connectivity rather than unit price alone; second, software and services (including connectivity, analytics, and report automation) are becoming as strategic as hardware; third, regional demand drivers and application mixes differ in maturity and procurement behavior — granular detail on those splits is provided in the full study.

Executive Playbook — succinct guidance for boards and procurement committees on CapEx phasing, lease vs. buy analysis, and KPIs to track post-purchase value realization.

TAM and SAM Modeling — transparent methodology, scenario assumptions, and sensitivity analyses you can adapt to your business case; models are delivered in editable format for internal stress-testing.

Segmentation and Use-Case Insights — demand drivers by application category and production environment, with buyer personas, purchase triggers, and decision timelines. (Note: we preserve high-level segmentation in this preview; the full study contains the actionable granular splits.)

Cost-to-Serve & Supply-Chain Module — landed-cost modeling that incorporates 2025 tariff regimes, supplier lead-times, and component sourcing risk; pragmatic mitigation strategies and supplier scorecards help procurement teams translate analysis into contracting terms.

Technology and Product Roadmaps — comparative assessment of bridge, gantry, articulated, and portable form-factors; multisensor trends; software ecosystems; and five-axis probing capabilities, including integration maturity and upgrade paths.

Competitive Heatmaps and M&A Playbook — our examination of incumbent capabilities, emergent product launches, and potential acquisition targets to accelerate time-to-market for new feature sets or service portfolios.

Operational Implementation Guides — stepwise plans for piloting shop-floor CMMs, creating measurement automation loops, and embedding metrology data into QA/ERP systems.

The CMM ecosystem is characterized by a mix of long-standing precision instrument manufacturers, software innovators, and niche specialists. Our competitive analysis synthesizes public disclosures, product launches, and observable go-to-market motions to highlight where incumbents are investing and where gaps remain.

Mitutoyo Corporation (Kawasaki, Japan) — a full-spectrum hardware provider with deep installed base advantages. Their strength is comprehensive product breadth across bridge, gantry, and portable systems, and established service networks that lower customer switching costs.

Hexagon Manufacturing Intelligence (Stockholm, Sweden) — focused on connected, high-throughput measurement workflows. Recent product introductions position Hexagon to capture customers prioritizing speed and integration into digital quality ecosystems.

ZEISS Industrial Metrology (Oberkochen, Germany) — premium multisensor capability and a strong presence in applications demanding the absolute highest accuracy. ZEISS remains a go-to for industries where traceable precision and certification are mission-critical.

LK Metrology (Castle Donington, UK) — specialist in ceramic-structured bridge systems and shop-floor adaptations. Their recent launches demonstrate a clear push to occupy the “shop-floor high-accuracy” segment with real-time inspection solutions.

WENZEL Group (Germany) — scaled supplier for large-part inspection and portal systems, positioned to serve heavy industries where part size and throughput are primary constraints.

Renishaw plc (UK) — known for probing and multisensor innovations, including five-axis systems; they are a strategic partner for integrators looking to add tactile and surface-finish measurement capabilities.

KEYENCE Corporation (Osaka, Japan) — focused on compact, integrated CMMs with fast deployment and user-friendly interfaces; their approach targets manufacturers prioritizing minimal training and immediate productivity gains.

Recent product and software developments underscore the dynamic nature of the ecosystem: software releases from major metrology vendors and CAD/inspection ecosystem players are adding CT scanning, real-time handheld scanning, enhanced probing strategies, and richer report customization. Product launches through 2025–2026 indicate vendors are racing to solve two practical customer problems — faster measurement cycles and easier integration with factory IT stacks.

Regulatory & standards environment: ISO 10360 continues to be a gating factor for aerospace, automotive, and medical device procurement decisions. Certification and traceability matter; non-compliance introduces material commercial and liability risk.

Labor & productivity pressures: Global skill shortages and rising labor costs are increasing the premium on automation-ready CMMs and solutions that reduce operator dependency. Vendors are responding with shop-floor-capable, higher-automation offerings.

Raw material and tariff shocks: 2025 tariff policies lifted landed costs for precision components materially, with industry data indicating effective landed-cost increases in the 20–40% range for crucial metals. That change necessitates re-examining sourcing geographies, component design-for-cost, and supplier contractual protections.

Consolidation pressure but room for disruption: Market concentration shows leading vendors hold significant shares, yet almost half the market remains outside the top-five leaders — an invitation for focused entrants or platform plays that couple hardware and software differentiated offerings.

Re-base CapEx prioritization on lifecycle analytics, not acquisition price. Build scenarios that include upgrade-path options, software subscription economics, and end-of-life trade-in strategies.

Insist on interoperability: procurement specifications should require open APIs, standardized data formats, and compatibility with enterprise-quality systems to avoid vendor lock-in and to enable measurement data monetization.

Layer supplier risk assessments with landed-cost sensitivity. For critical components, negotiate clauses that share tariff risk, and consider dual-sourcing or regional partner development to shorten lead times.

Prioritize pilots that demonstrate shop-floor resilience. The fastest pathway to scale is a validated pilot that proves uptime, accuracy under shop-floor conditions, and IT integration in a single production cell.

Evaluate M&A or partnership opportunities for acquiring software capabilities if your strategy emphasizes platform-driven revenue (analytics, predictive maintenance, or measurement-as-a-service).

Contracting behavior: multi-year service contracts bundled with software subscriptions are a sign that vendors are shifting to SaaS-like economics.

Standard adoption: updates or new interpretations in ISO 10360 or similar standards that expand multisensor validation will materially affect procurement criteria.

Product launches and trade shows (e.g., industry conferences in 2026) that emphasize connectivity, five-axis scanning, or shop-floor automation are likely leading indicators of where the market is headed.

Supplier manufacturing footprints and tariff mitigation moves: onshoring, nearshoring, or advanced supplier financing schemes will signal durable shifts in lead-time and cost baselines.

This briefing outlines the strategic imperatives and market signals leaders must incorporate into 2026 planning. Our full report delivers the granular segmentation, buyer-behavior matrices, supplier scorecards, and editable financial models needed to translate strategy into executable procurement and technology roadmaps. If your 2026 decisions involve CapEx deployment, vendor selection, or a move toward measurement-as-a-service, the full study contains the evidence-based inputs and scenario tooling required to make those choices defensible to boards and investors.

For access to the complete dataset, scenario models, and implementation toolkits — including the detailed regional, type, and application splits that support targeted commercial execution — refer to the PW Consulting report portal. The full report preserves confidentiality-sensitive competitive detail while providing the precise inputs executives need to make high-confidence decisions in 2026.

For detailed analysis of this topic, please visit the official page:Coordinate Measuring Machine (CMM) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com