Mechanical Vapor Recompression (MVR) Evaporators — Strategic Outlook for 2026 Decision-Making

Executive summary

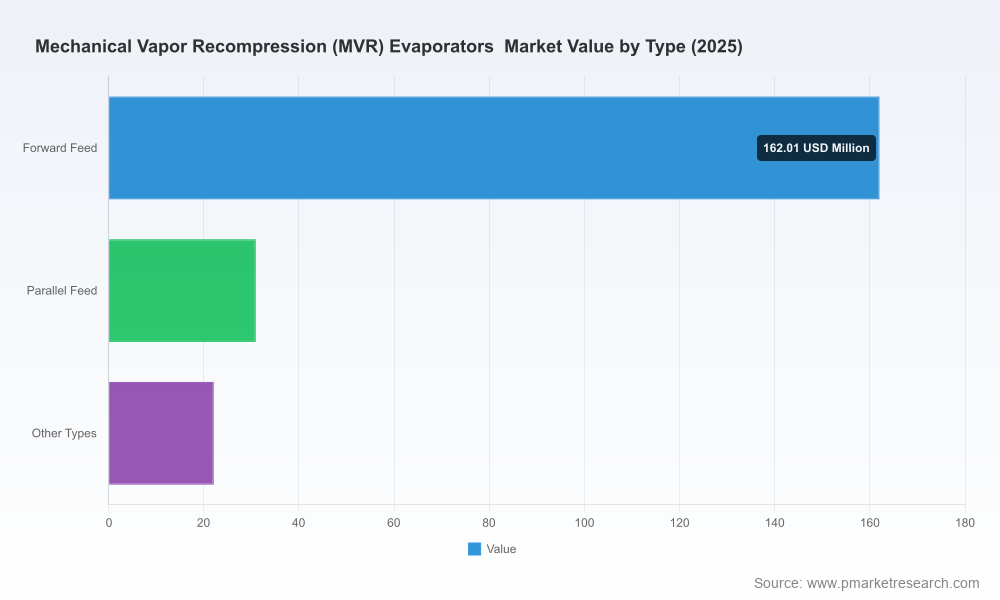

Mechanical Vapor Recompression (MVR) evaporators are moving from niche energy-saving equipment toward core infrastructure for water-sensitive and heat-integrated industrial processes. Our PW Consulting market model shows the global MVR evaporators market expanding from roughly USD 163 million in 2020 to USD 215 million in 2025, and continuing on a compound annual growth rate (CAGR) of 6.98% through the 2026–2032 forecast window. By 2032 the market reaches an estimated USD 345 million. Despite steady headline growth, concentration metrics (CR3 ~24.6%; CR5 ~26.2%) point to a fragmented competitive landscape where specialist engineering, regional service capabilities, and aftermarket economics determine winners and losers.

Mechanical Vapor Recompression (MVR) Evaporators Market

Why this study matters for 2026 corporate strategy

- CapEx prioritization: With continued growth and improving economics, 2026 is a pivotal year for companies to move pilot projects to capital deployment. The report’s financial models translate projected energy and water savings into payback windows under varying electricity and utility price scenarios.

- Technology selection: MVR offerings differ materially on compression technology, heat integration, crystallization capability, and automation. Selecting the right architecture now locks in 15–25 year operational profiles and maintenance regimes.

- Sustainability and compliance: Tightening energy and discharge regulations are shifting the calculus from OPEX-only reviews to lifecycle assessments. Our workbench enables rapid assessment of CO2-equivalent reductions and partial/full zero-liquid-discharge (ZLD) pathways.

- Supplier strategy and risk mitigation: The fragmented vendor base means buyers must evaluate not only unit pricing but spare-parts logistics, control-system roadmaps, local fabrication options, and financing structures.

Market trajectory: what the numbers tell us

The historical series in our base-year model (2020–2025) shows steady recovery and adoption post-2020, driven by higher utility costs and stronger environmental mandates. The 2025 baseline of approximately USD 215 million provides a pragmatic starting point for scenario planning. Under our base-case assumptions—moderate energy price inflation, gradual tightening of discharge regulations, and continued industrial efficiency investment—the market grows at 6.98% CAGR through 2032, reaching about USD 345 million.

Mechanical Vapor Recompression (MVR) Evaporators Market

This trajectory masks important non-linearities: pockets of accelerated adoption where ZLD and high-concentration brines intersect with strong energy-cost pull, and slower uptake in sectors with low thermal integration readiness. The bottom line for executives is clear: the addressable opportunity widens materially for companies willing to invest in tailored engineering and service delivery models.

Mechanical Vapor Recompression (MVR) Evaporators Market

Key dynamics shaping vendor and buyer decisions

- Energy-efficiency engineering: Recent vendor disclosures confirm MVR systems can achieve coefficients of performance north of 40 on narrow temperature lifts, materially reducing thermal input requirements. For capital projects, this translates into lower steam/thermal demand and improved lifecycle OPEX.

- Automation and labor substitution: Leading suppliers are embedding intelligent automation, self-diagnosis and self-cleaning features that cut routine maintenance and operator load—addressing a tightening labor market for skilled evaporator operators.

- Material and seal innovation: New low-carbon elastomers and seal materials with lower product carbon footprints are entering the supply chain, lowering life-cycle environmental impact and improving service intervals for seal-intensive installations.

- Service and aftermarket economics: Given the long service life of MVR units, aftermarket availability of compressors, controls, and replacement bundles drives total cost of ownership. Local fabrication and spare-part logistics are decisive selection criteria.

- Regulatory and procurement incentives: Energy-efficiency mandates and industrial wastewater discharge limits accelerate demand for full or hybrid ZLD architectures where MVR plays a central role.

Competitive landscape — what practitioners must know

The market is occupied by a mix of global engineering groups, specialized technology vendors, and regional manufacturers. Competitive differentiation is increasingly less about the evaporator shell and more about integrated solutions: compressor quality, control algorithms, crystallization know-how, and a services-led commercial model that includes financing, guaranteed performance, and spare-part support.

- Saltworks Technologies — A specialist in modular MVR crystallizers and evaporators with a focus on intelligent automation for ZLD. Recent product introductions emphasize capacity modularity and embedded self-diagnosis, reducing on-site labor and downtime risk. For buyers targeting ZLD on compressed project timelines, Saltworks’ modular approach reduces installation lead times and risk.

- GEA Group AG — A diversified engineering house offering integrated meVap® systems. GEA’s technical positioning highlights high coefficient-of-performance operations and packaged solutions that combine evaporation, crystallization, and distillation for complex processes. For industrials seeking tried-and-tested, heat-integrated solutions, GEA’s systems are compelling—especially where energy optimization is the design driver.

- Valmet — Known for pulp and chemical-recovery applications, Valmet’s MVR installations target low fan power operation and integration into existing recovery boilers and steam systems. Recent commissioning activities indicate a focus on major industrial clients with significant thermal integration complexity.

- ENCON Evaporators — A North American manufacturer emphasizing U.S.-made equipment and low operating-cost designs. ENCON’s value proposition centers on predictable OPEX and local support for industrial wastewater applications, making it attractive to buyers prioritizing domestic supply chains.

- LH Evaporator & Hanpu Mechanical Technology — Regional manufacturers from China with extensive installed bases. Their scale and cost-competitive manufacturing are attractive for projects where capital cost sensitivity and regional service networks outweigh premium control or automation features.

Strategic takeaway: procurement teams should segment procurement strategies between “performance-first” suppliers (high automation, guaranteed performance, integrated services) and “cost-first” suppliers (capex-efficient units with regional support). Blended sourcing strategies are viable where project risk is distributed across vendors.

What the full report delivers (practical, operational content)

Our full research package is designed to move decisions from “option” to “action.” Highlights include:

- Proprietary market model (2020–2032) with scenario toggles for energy price, regulatory intensity, and capital cost changes.

- Vendor benchmarking matrices covering technology features (compressor type, crystallization capability, automation level), warranty & service models, and aftermarket parts lead times.

- CapEx/Opex excel templates and payback calculators tailored to different industry use-cases (ZLD, concentration, pulp recovery, pharma).

- Case studies and reference installations with anonymized performance data and lessons learned on commissioning, scaling, and maintenance.

- Procurement playbooks and RFP templates that align technical KPIs with commercial terms (performance guarantees, uptime SLAs, spare-part stocking, and retrofit scopes).

- Regulatory and material inputs — a compact dossier on raw material and seal innovations, applicable efficiency mandates, and LCA considerations that impact procurement and TCO conversations.

Note: to preserve the strategic value of the study and encourage effective contracting, our public summary intentionally omits detailed regional and application split tables. These segment-level data, plus vendor scorecards and price benchmarking, are included in the full subscription report and associated deliverables.

How executives should use this intelligence in 2026

- Short-term (0–12 months): finalize pilot-to-scale gating criteria that tie energy and water targets to measurable payback thresholds and operational KPIs. Use our vendor benchmark to shortlist partners aligned with your service and automation requirements.

- Medium-term (12–36 months): integrate MVR-selected architectures into plant masterplans where thermal integration and ZLD ambitions exist. Prioritize procurement contracts that include performance guarantees, spare-part agreements, and remote-monitoring capabilities.

- Long-term (3–7 years): build supplier partnerships that deliver co-investment on retrofits and joint service hubs in priority regions. Consider M&A or JV activity to capture aftermarket value in high-growth corridors.

Closing: strategic posture and next steps

MVR evaporators are no longer adjunct efficiency devices; they are strategic levers for industrial water stewardship and energy-efficient production. For 2026, the most valuable decisions will be those that align technical selection with service economics and regulatory trajectories. Our modelling indicates a robust growth path and clear opportunities for companies that combine engineering excellence, automation, and aftermarket reach.

For decision-ready data — detailed segmentation, vendor scorecards, excel models, and procurement templates — access the full PW Consulting MVR Evaporators Market study and the accompanying implementation toolkit on our research portal. The public summary is designed to demonstrate methodology and strategic direction; the full intelligence package is required to execute with confidence.

For detailed analysis of this topic, please visit the official page:Mechanical Vapor Recompression (MVR) Evaporators Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com