Digital Calipers with LCD Display Market Overview: Key Drivers and Challenges

Other |

2026-04-20 06:53:09

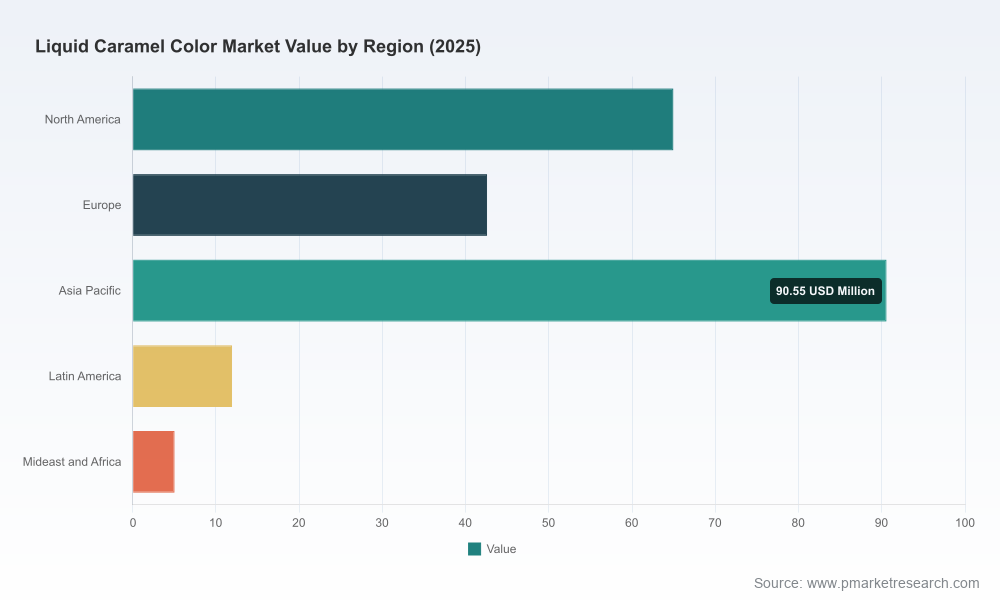

As PW Consulting’s Chief Industry Analyst, I present this executive preview of our Liquid Caramel Color Market study to help leaders prioritize choices in 2026. The market we modeled uses 2025 as its base year and traces historical performance from 2020–2025, with a forecast window covering 2026–2032. At a compound annual growth rate of 5.1% during the forecast horizon, the global liquid caramel color market shows steady expansion — a trajectory reflected in a rise from roughly USD 163 million in 2020 to about USD 215 million in 2025 and a projected climb toward the low‑hundreds of millions by 2032. This preview highlights the strategic implications of those dynamics without disclosing the granular segment tables reserved for the full report.

Liquid Caramel Color Market

Decisions in 2026 will be shaped by a mix of steady end‑market demand, regulatory scrutiny, supply chain pressure, and shifting customer expectations around naturalness and transparency. For commercial leaders — whether in ingredient supply, finished goods, private equity or procurement — the core questions are: where to allocate incremental capital, what formulations to prioritize, how to structure supply agreements, and which competitive threats require preemptive moves. The macro trajectory above signals opportunity, but the tactical levers differ by corporate role and risk appetite. This preview translates the headline growth into practical, prioritized action.

Liquid Caramel Color Market

Steady volumetric growth with compositional shifts. The market’s mid‑single‑digit CAGR masks structural change: traditional demand drivers remain — beverages and processed foods continue to account for a substantial share of usage — while reformulation for clean‑label and regulatory compliance is reshaping product portfolios. Companies that can offer differentiated, certified liquid formats (e.g., low‑4‑MeI variants, organic, Kosher/Halal) will capture premium placements.

Liquid Caramel Color Market

Moderate market concentration. The sector exhibits a moderate concentration profile (top three and top five supplier groups capture a meaningful share of supply), which creates bargaining room for dominant suppliers but also opens windows for agile niche providers to win formulation partnerships or regional contracts.

Price resilience, with margin pressure in commoditized channels. Pricing behavior is influenced by raw‑material cycles, regulatory testing costs, and specialty certification expenses. Suppliers that integrate formulation science with supply reliability will preserve margins; those exposed to spot raw‑material swings face compression.

Regulatory context remains a central determinant of product strategy. Key authorities continue to affirm caramel color’s regulatory status: U.S. and EU frameworks maintain established positions on acceptable daily intake and usage standards. Our review highlights two operational takeaways for 2026:

Compliance as a market differentiator. Acceptable daily intakes for certain caramel classes are codified, and industry practice has converged on formulation and documentation standards that demonstrate compliance for global supply chains. Suppliers that embed regulatory testing and transparent reporting into customer contracts gain access to global blue‑chip buyers with rigorous supplier qualification processes.

4‑MeI and Proposition 65 remain a live issue. Class III and Class IV caramel colors can contain trace 4‑methylimidazole (4‑MeI), and regulatory or labeling regimes in certain jurisdictions have prompted suppliers to develop low‑4‑MeI variants. This is both a compliance cost and a commercial opportunity: buyers seeking aggressive risk mitigation or a clean‑label stance are willing to accept premiums for documented low‑4‑MeI solutions.

The competitive map blends global ingredient houses, regional volumes suppliers, and formulation specialists. Our qualitative assessment of notable players shows the following patterns:

Sethness Roquette (Clinton, Iowa) — breadth plus certification leadership. The company’s multi‑class portfolio, organic and special production lines, and recent issuance of Kosher and Halal certificates reinforce its position with multinational CPGs that require certified global streams. For buyers, Sethness represents a low‑friction partner for scale and documentation demands.

D.D. Williamson (Louisville, Kentucky) — formulation depth and product stewardship. With updated product specifications for core Class IV liquid forms, the firm emphasizes application‑specific grades and regulatory transparency — traits attractive to beverage formulators and private‑label manufacturers focused on stability and label claims.

Ingredion, Sensient, Kerry, and GNT — integrated ingredient and color strategies. These players combine caramel color offerings with broader ingredient portfolios, enabling bundling of functional and color solutions. Their value proposition centers on formulation efficiency and supply chain simplification for large CPG accounts.

Regional Indian manufacturers (several established exporters) — cost‑competitive capacity and regional agility. These suppliers play a critical role in price‑sensitive segments and contracts where local approval and logistics are decisive. Their relevance grows where buyers prioritize cost and rapid lead times over premium certifications.

Overall, the landscape rewards two distinct supplier archetypes in 2026: (1) premium, compliance‑centric partners that support global, label‑sensitive accounts; and (2) scalable, cost‑effective producers that serve regional, price‑sensitive channels. Investors and acquirers should map acquisition targets against these archetypes.

Prioritize contractual clarity on specifications and testing. Embed low‑4‑MeI thresholds, test frequency, and certification obligations into supply contracts to reduce commercial risk and protect shelf space against quality scares.

Invest in certification where you sell globally. Kosher, Halal, and organic credentials translate to easier shelf entry in regulated markets and reduce the cost of qualification for multinational buyers. For suppliers, this is a capitalized route to premium pricing.

Adopt a tiered product architecture. Offer a base commodity liquid plus two premium variants (e.g., low‑4‑MeI and certified organic) to capture diverse buyer segments without proliferating SKUs.

Use scenario planning to price for volatility. Build price escalation clauses and hedging playbooks tied to key feedstock indices; this is especially important where raw‑material cycles were historically volatile.

Leverage co‑development with customers on clean‑label reformulation. Co‑sourcing pilot projects reduce time‑to‑shelf and can lock in offtake for specialty grades.

Screen M&A opportunities against concentration metrics. With top suppliers holding a meaningful share of the market, bolt‑on acquisitions that broaden certification, geographic reach, or technical capabilities can be high‑value for mid‑sized ingredient players seeking scale.

This preview demonstrates the strategic shape of the market and immediate implications for 2026 planning. The comprehensive study contains the proprietary granularity that commercial and investment decisions require: detailed regional and application segmentation, product‑class breakdowns, supplier scorecards and positioning matrices, price‑by‑region decks, formulation cost models, contract playbooks, and scenario forecasts across multiple risk vectors. To preserve the trailer effect of this preview, we have withheld the full segment tables and the granular regional/application percentages that underpin the financial models. Accessing the full report provides the exact datapoints, downloadable datasets, and an interactive forecast model that buyers and strategists can use to stress‑test decisions.

Liquid caramel color is a mature ingredient category with nuanced pockets of innovation. Growth is predictable but not uniform; regulatory shifts and label sensitivity will continue to create arbitrage between certified premium solutions and lower‑cost commodity supply. For executives planning capital allocation, go‑to‑market changes, or M&A this year, the priority is to align product portfolios to buyer requirements (regulatory proof points, certifications, and low‑4‑MeI claims) while preserving margin flexibility through a tiered offering and contract protection mechanisms.

If your team needs a tailored briefing that translates these insights into an operational roadmap — supplier scorecards, contract clause templates, or an M&A target short‑list — PW Consulting’s full Liquid Caramel Color Market report and advisory services deliver the numbers, model access, and implementation playbooks you will need to act confidently in 2026.

For detailed analysis of this topic, please visit the official page:Liquid Caramel Color Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com