Antibody-Drug Conjugate (ADC) Oncology Market: Insights, Key Players, and Growth Analysis

Other |

2026-04-27 08:59:48

As PW Consulting’s Senior Strategy Advisor and Lead Industry Analyst, I present a focused preview of our full Chandeliers Market study to inform executive choices in 2026. This briefing synthesizes the report’s strategic takeaways and illustrates how executives can convert market visibility into defensible action—while reserving the granular segment tables and precise regional breakdowns for the full report. Our base year is 2025 (reported in USD, revenue in Million units), and the market is modeled across a 2026–2032 forecast horizon at a compound annual growth rate (CAGR) of 4.8%.

Chandeliers Market

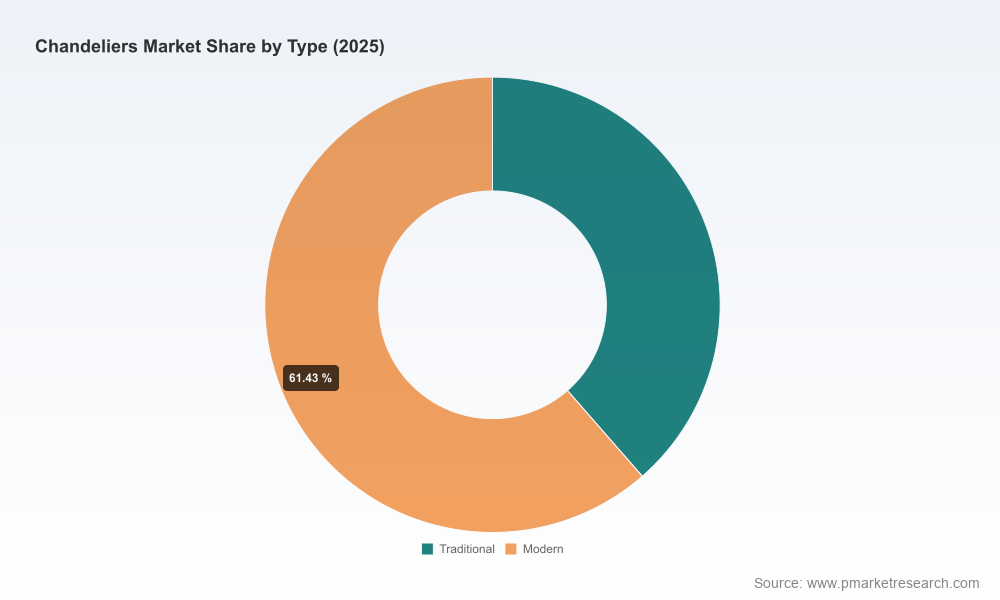

Chandeliers sit at the intersection of design, lighting technology, and built-environment decisioning. After several years of steady expansion through 2020–2025, the market entered 2026 from a position of modest scale and structural change. The total market size in 2025 provides the baseline against which near-term investments, channel strategies, and procurement decisions should be judged; our forecasts extend across 2026–2032 so that capital allocation and product roadmaps can be stress-tested against alternative demand and supply scenarios.

Chandeliers Market

Executives thinking in 2026 must contend with three converging forces: (1) an ongoing premiumization of fixture design driven by high-end residential and hospitality refurbishment cycles, (2) a technology shift as LED and integrated controls become baseline expectations, and (3) supply-side frictions that periodically re-price components and logistics. The result is a market that rewards nimble sourcing strategies, modular product platforms, and tight go-to-market execution.

Chandeliers Market

Our competitive concentration analysis shows a market that is moderately consolidated. The combined market share of the top three and top five suppliers indicates meaningful scale advantages for incumbents—but not so concentrated that innovators cannot carve differentiated positions. This concentration profile underscores two practical implications:

The report includes a focused vendor analysis of leading manufacturers and designers active in the chandeliers space. Profiles cover product positioning, distribution footprints, and recent strategic motions. Examples of firms reviewed include established U.S. players with broad lighting portfolios, family-owned makers with heritage brands, design-centric producers, and major fixtures manufacturers based in Asia. We track near-term product introductions and catalog updates through early 2026—evidence that incumbents are investing in refreshed collections and LED integrations to capture evolving buyer preferences.

We integrate several proximate supply-side developments into our baseline and scenario assumptions. Executives should treat these as decision triggers rather than static constraints:

For leadership teams updating their 2026 plans, the report identifies a prioritized checklist to convert insight into impact within 90–180 days:

Our methodology triangulates historical shipment and revenue trends (2020–2025) with input from primary interviews, proprietary dealer surveys, and bottom-up BOM modeling. Forecasts for 2026–2032 are stress-tested across demand and supply permutations and are presented in Million USD terms. We provide confidence bands and sensitivity matrices in the full report so that financial planners and product strategists can map revenue and margin outcomes to specific assumptions (price elasticity, lead-time shock, tariff scenarios, and technology adoption rates).

This preview provides the strategic context and decision frameworks but deliberately omits granular segment tables and region-by-application splits. Those discrete segment values and SKU-level benchmarking are core proprietary outputs of the full report and are required to support transactional-level decisions such as channel pricing, regional distributor selection, and product line P&L management. In short, this preview explains the how and why; the full study supplies the exact what.

In 2026, chandelier market winners will be those who combine three capabilities: cost-aware product modularity, accelerated time-to-market for differentiated collections, and supply-chain resilience for critical components. Whether you are a manufacturer optimizing a plant footprint, a brand rethinking distribution, or a private equity investor sizing a bolt-on, the strategic playbook in the full PW Consulting study converts market-level growth assumptions (anchored on a 4.8% CAGR across the forecast window) into executable options and financial thresholds.

For teams preparing capital allocation memos, product roadmaps, or procurement strategies this year, the report is designed to be actionable within the quarter. If you want the full segmentation, vendor scorecards, and downloadable financial models that underpin these recommendations, the complete market study contains them in downloadable form and is the logical next step for decision-makers who require transaction-grade detail.

For detailed analysis of this topic, please visit the official page:Chandeliers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com