Blood Test At Home in Dubai | Certified Technicians at Your Home

Health |

2026-06-19 12:27:25

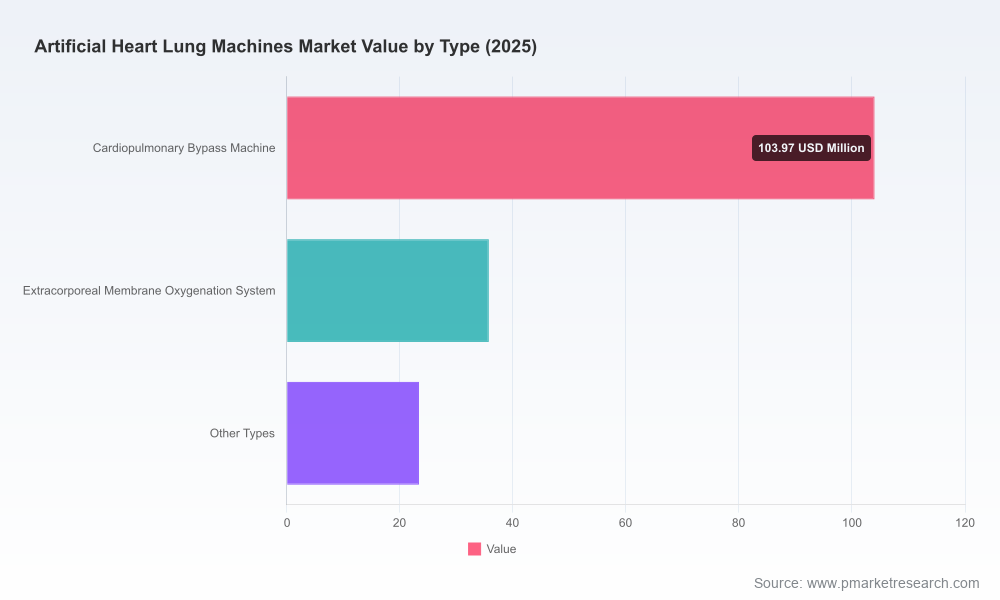

The artificial heart-lung machines market is entering a phase of steady expansion. With a 2025 base-year valuation of approximately USD 163.1 Million and a forecast trajectory that reaches roughly USD 260.6 Million by 2032, the market is expected to grow at a compound annual growth rate (CAGR) of 6.9% across the 2026–2032 forecast window. That macro momentum reflects a mix of clinical demand (longer and broader extracorporeal support), new product introductions, regulatory recertifications that extend device use, and evolving reimbursement frameworks that make extracorporeal therapies more accessible to payers and providers.

Artificial Heart Lung Machines Market

Capital allocation: The market’s mid-single-digit CAGR signals a durable, investable sector—but one where returns favor scale, product-service integration, and regulatory certainty. Decisions on manufacturing footprint, R&D investment, and commercial roll-out timing will materially affect ROI.

Artificial Heart Lung Machines Market

Portfolio strategy: High technical and clinical barriers favour incumbents, yet regulatory shifts and regional commercial openings create windows for focused innovators. Understanding when and where to prioritize ECMO vs. cardiopulmonary bypass bets is essential.

Artificial Heart Lung Machines Market

M&A and partnership timing: A concentrated vendor landscape (top-three and top-five concentration remain substantial) creates strategic pathways for bolt-on acquisitions, distribution partnerships, or defensive alliances—especially for companies seeking rapid entry into underserved geographies or clinical niches.

Market access and reimbursement: Recent payer guidance and device-specific reimbursement references are already changing hospital economics. Payers’ evolving positions on continuous and extended-duration extracorporeal support will alter procurement and utilization patterns in 2026.

Actionable market sizing and forward-looking scenarios: granular, model-driven forecasts with upside/downside scenarios and sensitivity analyses to test price, adoption, and reimbursement shocks.

Segment playbooks: end-to-end go-to-market canvases for cardiopulmonary bypass (CPB), extracorporeal membrane oxygenation (ECMO), and emerging hybrid devices—covering product positioning, clinical evidence needs, training programs, and service models.

Regulatory & reimbursement roadmaps: country-by-country timelines and milestone maps (including recent MS-DRG and payer guidance examples), enabling planning for CE/FDA/other approvals and price-setting strategies.

Competitive benchmarking: in-depth profiles and capability matrices for global OEMs and regional suppliers, highlighting product portfolios, clinical traction, regulatory statuses, and distribution models.

Commercial and pricing frameworks: templated negotiation strategies for purchasing groups and hospital systems, total cost of ownership calculators, and subscription/consumables revenue models.

M&A screening and diligence tools: prioritized target lists (by capability and geography), valuation sensitivities, and integration checklists focused on supply continuity, IP, and install-base synergies.

Operational risk register: supply chain, quality/regulatory, and clinician adoption risks with mitigation playbooks—useful for procurement, manufacturing, and R&D leaders.

The market is characterized by a mixture of global platform leaders, specialized innovators, and cost-focused regional OEMs. This mix produces a marketplace where clinical trust and service reliability are as decisive as device features.

Medtronic plc (Ireland) — A global leader with advanced ECMO and CPB offerings. Recent regulatory traction and payer engagement (including published reimbursement references) position Medtronic to influence clinical standards and pricing dynamics in 2026.

LivaNova PLC (United Kingdom) — Focused commercial roll-outs and analytics partnerships demonstrate a strategy of combining device refreshes with data-enabled perfusion optimization to win hospital share, notably in large emerging markets.

Getinge AB (Sweden) — The company’s shift away from certain surgical perfusion production toward ECMO systems signals portfolio reorientation. That strategic pivot creates redistribution of competitive focus and potential whitespace for others in surgical perfusion.

Terumo Corporation & Xenios AG (Japan & Germany) — Established device families and ECMO console strengths underpin durable clinical adoption; both are likely to remain core competitors where product reliability is non-negotiable.

Inspira Technologies & CBM Lifemotion (Israel & other innovators) — Recent clearances and CE marks, followed by commercial rollouts, mark these firms as fast-follow or disruptor candidates—capable of shifting clinical practice if evidence and support models scale.

Regional OEMs and service specialists — Companies in Brazil, Japan, China, India, and Southeast Asia continue to supply attractive cost-performance options and local maintenance capabilities. They are critical partners or acquisition targets for global players seeking local traction.

Service and distribution channels — Specialist resellers and service providers remain pivotal to adoption; their role in installation, training, and consumables management is a strategic asset.

Several firms achieved regulatory and market milestones in 2024–2025, including new CE marks and FDA clearances, followed by staggered commercial rollouts. These certifications enable longer-duration extracorporeal use in some jurisdictions and directly influence hospital procurement cycles.

Notable commercial actions—such as launches into major markets and analytics partnerships—signal a dual trend: vendors are bundling software and services with hardware, and analytics/data platforms are becoming differentiators.

Strategic product rationalizations (e.g., manufacturers refocusing portfolios) re-shape competitive geometry and open tactical opportunities for entrants and niche specialists.

For incumbents: prioritize service and consumables revenue streams to protect margins; accelerate software/analytics integration to lock in clinical workflows; use regulatory wins to negotiate better reimbursement and long-term contracts.

For challengers and innovators: adopt a regulatory-first commercialization plan, focus on a narrow clinical segment to build evidence and install base, and structure partnerships for distribution and aftercare rather than attempting immediate global scale alone.

For private investors: favor platform companies with recurring revenue, strong service networks, and demonstrable clinical outcomes. Consider roll-up strategies to consolidate regional OEMs where local procurement favors domestic suppliers.

For hospital systems and group purchasers: demand bundled outcomes-based contracts, insist on interoperability and clinician training commitments, and use procurement timing to capture newly certified extended-use devices at favorable terms.

Three plausible trajectories should guide contingency planning: a base case consistent with the current CAGR outlook; an upside where accelerated reimbursement and guideline endorsements drive faster adoption; and a downside where regulatory tightening and supply disruptions compress growth. Key triggers to watch include major payer coverage decisions, high-profile multi-center clinical outcome studies, large procurement agreements in emerging markets, and strategic withdrawals or launches by major OEMs.

Our Artificial Heart Lung Machines Market study combines rigorous market-sizing, scenario-driven forecasting, executable go-to-market playbooks, and competitive diligence to support practical decisions in 2026: from budgeting and R&D prioritization to M&A screening and commercial execution. The analysis surfaces where value will accrue in the coming three years and identifies the operational moves that materially change market position.

For executives preparing 2026 budgets, board briefs, or transaction memoranda, this research is designed as a practical toolkit: models you can adapt, checklists you can operationalize, and strategic pathways you can execute. Access the full dataset, segmented forecasts, and downloadable financial models on our report page to convert this preview into a decision-grade plan.

For detailed analysis of this topic, please visit the official page:Artificial Heart Lung Machines Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com