Piezo Positioners Market — Strategic Outlook for 2026: A PW Consulting Brief

As piezo-driven positioning systems move from niche laboratory fixtures to mission-critical components across semiconductor fabs, optical instrumentation, and advanced manufacturing, executives need a concise, decision-grade perspective that translates market trends into concrete strategic options. Our new Piezo Positioners Market study (base year 2025; historical 2020–2025; forecast 2026–2032) delivers that perspective. The global market is projected to expand at a steady compound annual growth rate (CAGR) of 7.5% through the forecast window — a trajectory that creates distinct windows for product innovation, supply-chain repositioning, and targeted consolidation. This preview synthesizes the study’s strategic value for enterprise decisions in 2026 while intentionally withholding the report’s granular split tables to encourage direct engagement with the full dataset.

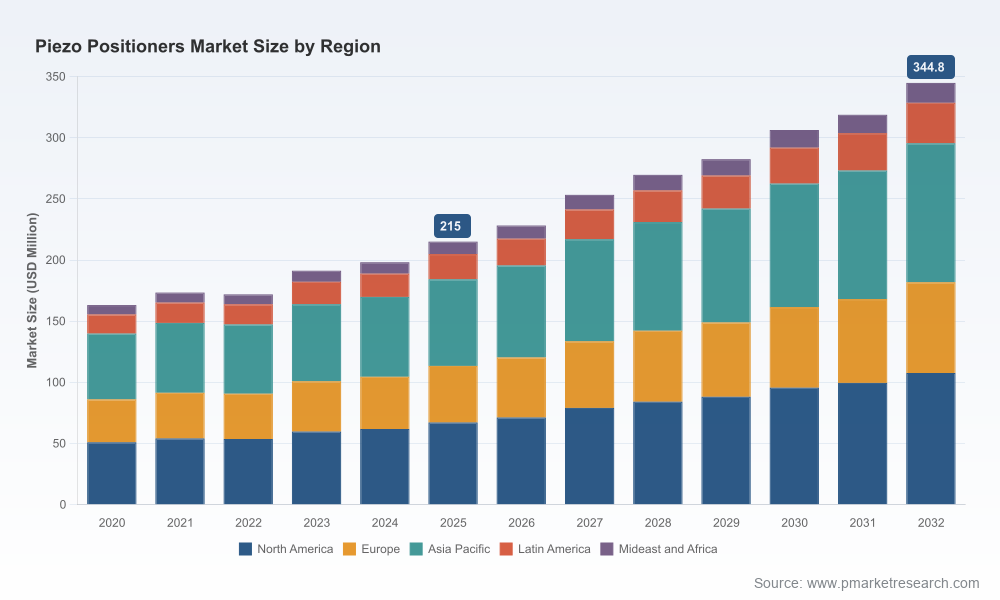

Piezo Positioners Market

High-level market view

By design, piezo positioners sit at the intersection of high-precision mechatronics and specialty materials. Our top-level sizing and trend analysis show the market in 2025 forming a clear inflection point: steady year-on-year recovery from early-decade volatility, followed by an accelerated demand pathway driven by semiconductor equipment upgrades and precision optics projects. The forecasted 7.5% CAGR reflects both the structural demand for higher-precision motion control and ongoing product diversification — from compact, limited-travel stages to multi-degree-of-freedom platforms for industrial applications.

Piezo Positioners Market

Two implications emerge immediately for 2026 corporate planning cycles: (1) near-term investment should prioritize modular, scalable platforms that can be configured for both R&D and industrial use cases; (2) supply-chain and regulatory risk management must be elevated given material sensitivities and tightening directives in key jurisdictions.

Piezo Positioners Market

Why this research matters for 2026 decision-making

- Capital allocation and R&D prioritization: With predictable top-line growth and identifiable inflection points, R&D roadmaps can be aligned to capture growth in higher-value segments while pruning legacy low-margin SKUs.

- M&A and partnership targeting: The market exhibits low-to-moderate concentration, creating attractive bolt-on targets and technology-acquisition opportunities. Our analysis surfaces the types of capabilities that move the needle in valuations (e.g., integrated control electronics, vacuum-compatible designs, multi-axis miniaturization).

- Supply-chain resilience: The industry’s reliance on piezoelectric ceramics (notably PZT) and evolving lead-free alternatives means sourcing strategies and supplier partnerships will materially impact cost curves and environmental compliance exposure.

- Regulatory readiness: New and revised directives across the EU, North America and health-care regulators introduce compliance margins that influence time-to-market. Companies that pre-emptively validate material substitutions and EMC/safety profiles will gain commercial advantage.

- Go-to-market and service models: The opportunity for aftermarket services, calibration contracts, and integration services is expanding alongside device adoption. Our study quantifies where a service-first approach drives better lifetime value.

What’s in the full report (practical, actionable components)

The full PW Consulting report is built for operators and strategists. Highlights include:

- Market sizing and validated forecast (2026–2032) with scenario analysis and sensitivity testing to price, material-cost and end-market demand shocks.

- Methodology appendix documenting data sources, primary interviews, and the bottom-up/top-down triangulation approach used to ensure reproducibility of results.

- Operational playbooks for product development, procurement, and quality assurance — including recommended certification roadmaps for medical and industrial deployments.

- Go-to-market blueprints tailored to OEMs, systems integrators and laboratory suppliers, with practical pricing and bundling strategies that reflect differential adoption curves across customer types.

- A searchable database of company profiles, transactional benchmarks, and an interactive financial model you can download to test your own strategic scenarios.

Note: This preview intentionally excludes the report’s granular regional, product-type and application-level splits; those detailed matrices and downloadable models are available with the complete publication.

Competitive landscape and strategic positioning

The industry’s competitive fabric combines established precision motion specialists with vertically-integrated optics and photonics suppliers. Market concentration metrics indicate a fragmented ecosystem, with the top three and five players accounting for a relatively small share of total revenues — a structure that favors niche differentiation and tactical consolidation.

- Physik Instrumente (PI) — Germany (https://www.physikinstrumente.com): A benchmark in high-precision motion systems, PI’s product depth spans modular piezo stages and turnkey positioning solutions. Their engineering excellence and broad catalog make them a default partner for high-end OEMs and research institutions.

- Aerotech Inc. — United States (https://www.aerotech.com): Aerotech’s strength is in motion control systems that combine precision stages with advanced controllers. They are often chosen where deterministic performance and systems integration are central to a customer’s value proposition.

- SmarAct GmbH — Germany (https://www.smaract.com): SmarAct focuses on compact, high-resolution stages optimized for laboratory and industrial metrology. Their product strategy emphasizes low drift and high repeatability for scientific instrumentation.

- attocube systems — Germany (https://www.attocube.com): Attocube’s portfolio is oriented toward cryogenic and vacuum-compatible nanopositioning, making them a preferred supplier in advanced physics and semiconductor inspection applications.

- Piezosystem Jena — Germany (https://www.piezosystem.com): Known for precision piezo mechanics and custom stage solutions, they maintain strong channels into academic research and bespoke industrial projects.

- Mad City Labs Inc. — United States (https://www.madcitylabs.com): With a history in nanopositioning for microscopy and life-science platforms, Mad City Labs competes on motion performance and microscopy-specific integrations.

- MICRONIX USA — United States (https://micronixusa.com): MICRONIX has been active with recent product introductions that emphasize multi-axis platforms and ultra-high-density controllers for industrial deployments, signaling an aggressive move into broader manufacturing markets.

- Thorlabs Inc. — United States (https://www.thorlabs.com): As a broad photonics supplier, Thorlabs adds scale and distribution reach, making piezo positioners accessible to a diverse base of end-users through strong channel relationships.

Strategically, incumbents are differentiating along three vectors: (1) systems integration and controller sophistication, (2) materials and environmental compatibility (vacuum/cryogenic/lead-free), and (3) go-to-market reach through distribution and OEM partnerships. For challengers, the fastest route to material growth is specialization — either by application vertical (e.g., semiconductor metrology) or by platform attribute (e.g., ultra-compact multi-axis systems).

Signals worth watching: material, regulatory and product cues

- Raw material dynamics: PZT remains the dominant piezoelectric ceramic, but price sensitivity and environmental pressure are accelerating R&D into lead-free alternatives. Companies that secure supply or master alternative-material performance will protect margins and access markets constrained by environmental directives.

- Regulatory tailwinds and constraints: The EU’s RoHS rules, updated EMC and safety standards in North America, and tightened FDA guidance for medical-stage applications all create certification and design constraints. Early compliance reduces time-to-market friction and becomes a competitive differentiator.

- Market catalyst events: Recent product announcements from industry providers — including multi-degree-of-freedom platforms and ultra-high-density controllers — are evidence of movement toward industrial-grade deployments. Corporate buyers should evaluate these new capabilities both for in-house adoption and for potential supplier consolidation.

- Cross-border harmonization: Regulatory alignment between Canada and the United States, as well as export-control considerations for high-precision equipment, are reshaping regional strategy for North American and global suppliers.

Strategic playbook for 2026 (what leading firms will do)

- Hedge material exposure: Negotiate multi-year contracts with ceramic suppliers, accelerate material substitution projects, and validate lead-free piezo prototypes under target use conditions.

- Modularize product platforms: Design product families where control electronics and mechanical modules are re-usable across applications to shorten development cycles and reduce inventory complexity.

- Certify early for regulated markets: Build EMC/safety and biocompatibility testing into the development loop to cut certification lead time — particularly for medical and industrial automation buyers.

- Expand service-led revenue: Create bundled calibration, remote diagnostics and lifecycle maintenance offerings to capture recurring revenue and improve customer stickiness.

- Pursue tactical M&A: Target firms with differentiated controller IP or access to specialty materials, rather than chasing scale alone; integration of these capabilities yields faster margin improvement.

Next steps — how PW Consulting unlocks the full value

This preview surfaces the strategic frames that matter in 2026, but the full study delivers the operating tools required to act: downloadable financial models, the granular segmentation matrices, company-level scorecards, and supply-chain heatmaps. For teams evaluating R&D roadmaps, M&A targets, or regional rollout strategies, those data products reduce execution risk and accelerate time to decision.

Engage with PW Consulting for: custom scenario runs on the forecast model, supplier due diligence packages, and an executive workshop that translates the study’s insights into a prioritized 90–180 day action plan tailored to your capabilities and market position.

To access the complete dataset, company profiles, and interactive models, please visit the report page linked in our release. The granular segmentation and downloadable tools are intentionally gated to ensure the integrity and practical benefit of the analysis for paying subscribers and direct advisory clients.

For detailed analysis of this topic, please visit the official page:Piezo Positioners Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com