Rheumatology Drugs Market Trends Supporting 6% CAGR Expansion

Other |

2026-03-02 09:34:31

As PW Consulting’s lead industry analyst, I present a strategic preview that translates our full Nursery Planters and Pots Market study into the precise priorities executive teams must act on in 2026. The market has demonstrated steady expansion from an estimated USD 1.6 billion in 2020 to roughly USD 1.95 billion in 2025 (base year). Under current assumptions the sector is projected to continue growing modestly through the forecast window (2026–2032) at a compound annual growth rate of approximately 2.5%, reaching just over USD 2.3 billion by 2032. What follows is a synthesis of the report’s most consequential insights, the operational levers that matter to manufacturers, growers and investors, and a clear line of sight to the strategic moves that will shape competitive advantage next year.

Nursery Planters and Pots Market

Decision timing: 2026 is the inflection where sustainability commitments and practical economics collide. Buyers—from large commercial growers to retail garden centers—are demanding greener credentials while procurement remains highly cost-conscious.

Nursery Planters and Pots Market

Margin preservation: modest market growth and increasing input volatility mean suppliers must find margin uplift through product differentiation, operational efficiency, or integrated circular programs rather than relying on volume expansion alone.

Nursery Planters and Pots Market

Regulatory and reputational risk: recycling pilots and state-level scrutiny are moving from concept to implementation; companies that align early with verified circular pathways will avoid downstream compliance and brand risk.

Robust market sizing and scenario forecasts (2020–2032), including baseline, upside and downside scenarios shaped by material-cost shocks and regulatory outcomes.

Competitive landscaping with strategic profiles and capability maps for leading suppliers, plus a supplier-strength scorecard to prioritize partner selection and M&A targets.

Materials and manufacturing playbook comparing cost-to-serve, CAPEX needs and lifecycle trade-offs across plastic, recycled-resin, molded fiber and biodegradable solutions.

Channel and customer segmentation frameworks that translate buyer economics into SKU rationalization and go-to-market priorities.

Operational KPIs and a step-by-step guide to implementing closed‑loop collection pilots, including contractual models with nurseries and retail partners.

Financial sensitivity models—price elasticity, raw-material pass-through and breakeven analyses—that let executives test strategic choices on their own P&L.

Slow but steady growth: the market’s projected 2.5% CAGR indicates resilience rather than runaway expansion. Growth pockets will be driven by replacement cycles, premium indoor-plant products and specialty horticulture segments rather than broad-based volume lifts.

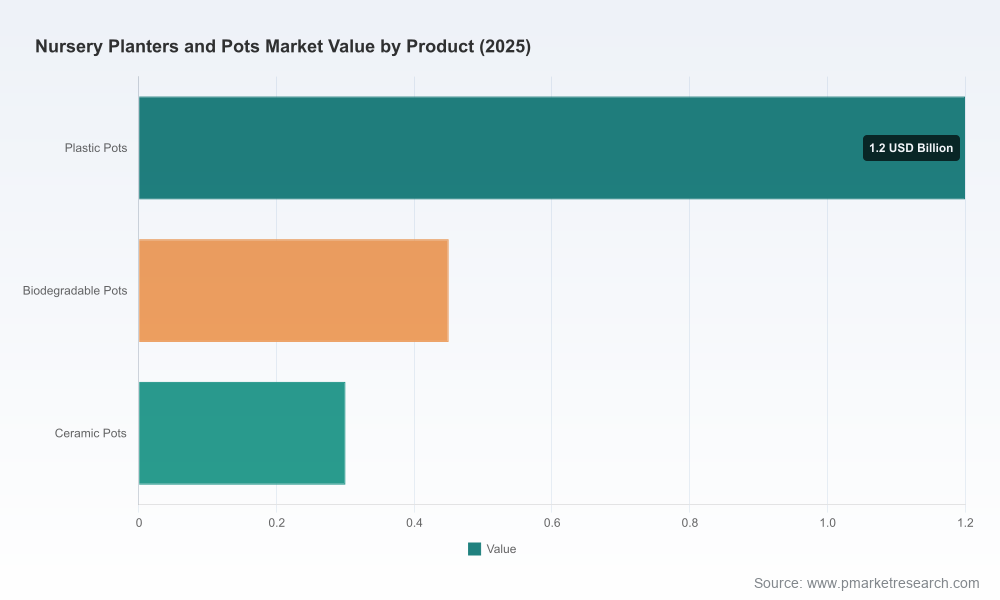

Material economics vs. sustainability expectations: producers continue to feel the tension between the low production cost of traditional plastic pots (measured in cents) and higher-cost biodegradable or molded-fiber alternatives. Buyers increasingly demand sustainability credentials, but willingness to pay premium varies across channels and end-users.

Waste and regulatory pressure: industry pilots—such as association-led pot collection programs—signal increasing externalities accountability. Current data indicate a very high disposal rate for conventional pots, which translates into policy risk and a mounting need for traceable recycling solutions.

Supply-side innovation is bifurcating: one track focuses on recycled and impact-modified plastics that preserve cost and durability; the other pursues biodegradable feedstocks and molded fiber for brand-differentiated sustainability. Both paths are viable but require distinct investments and channel propositions.

The market exhibits moderate concentration: top-three and top-five shares point to meaningful national players coexisting with a long tail of regional specialists. That structure creates strategic choices for both incumbents and entrants.

Scale manufacturers (capacity and breadth): firms with large-volume blow-molding, injection and thermoforming capabilities are advantaged on cost and lead time for commercial growers. These operators will compete on price, service and breadth of SKU availability.

Recycled-content innovators: companies that have invested in closed-loop processes to use high percentages of post-consumer recycled resin provide a compelling value proposition to buyers seeking verifiable circularity without the full cost premium of biodegradable alternatives.

Sustainability-first challengers: biodegradable and molded‑fiber producers are carving premium niches with customers willing to trade up for perceived environmental benefits, particularly in consumer-facing retail and higher-margin specialty segments.

Regional and specialty specialists: producers focusing on particular crop needs or unique horticultural formats retain defensible positions through specialized tooling, local logistics and deep grower relationships.

Major suppliers are refreshing catalogs and trade-show roadmaps to highlight recycled resins and sustainable portfolio extensions, signaling that circular claims are moving from marketing to product reality.

Association-driven pilots and trade shows are converting conversation into practice: collection and recycling pilots, industry trade events and state-level showcases are accelerating buyer exposure to alternative materials and supply-chain solutions.

Data on disposal and longevity of conventional pots is raising the cost of inaction—both from a public-policy standpoint and brand reputation perspective.

Operational: Build manufacturing flexibility. Prioritize modular tooling, multi-process capacity (blow, injection, thermoforming) and quick-change lines to switch between conventional and recycled/polymer blends. This reduces obsolescence risk and enables rapid response to customer trials.

Commercial: Create a two-track product strategy. Protect margin-sensitive, high-volume accounts with low-cost, durable plastics while rolling out premium, branded sustainable products to capture retailer and consumer willingness to pay. Use pilot recycling programs as a conversion tool for mid‑market customers.

Partnership and M&A: Pursue bolt-on acquisitions of regional producers or material-technology startups that provide either circular feedstock access or biodegradable manufacturing expertise. Smaller deals accelerate capability build with lower integration risk than greenfield investments.

Stress-test product portfolios: use the report’s SKU profitability models to identify which SKUs should be scaled, retired or relaunched with sustainable variants.

Design pilot KPIs: adopt our recommended metrics for closed-loop pilots—collection rates, contamination rates, net cost per unit recovered, and time-to-reuse—so pilots become repeatable commercial programs, not PR exercises.

Align procurement: map supplier scorecards against total-cost-of-ownership, not just unit price; include end-of-life logistics and brand risk as explicit cost inputs.

This preview purposefully highlights strategic conclusions while withholding the granular segment-by-segment revenue splits, regional share tables and confidential supplier-by-supplier revenue estimates. Those detailed data, plus downloadable model files, supplier scorecards, SKU-level forecasts and bespoke scenario outputs, are available in the full PW Consulting report and the accompanying data pack. We follow a “trailer” principle: this brief demonstrates our analytic depth to establish confidence, and the full dataset empowers executable decisions.

For executives allocating capital in 2026, the key choice is not whether the nursery planters and pots market will grow — it will, if modestly — but how to position for a market that prizes both cost discipline and credible sustainability. Firms that invest early in verified recycled-content supply chains, flexible production capability, and commercially realistic collection/recycling partnerships will secure disproportionate access to growth pockets and avoid the rising downstream costs of noncompliance. Conversely, players who treat sustainability as purely a marketing line risk margin erosion and escalating compliance exposure.

PW Consulting’s full report provides the granular evidence and financial templates to turn these strategic directions into an executable 12–36 month roadmap. For access to the complete study, detailed datasets, and tailored advisory support to operationalize the recommendations outlined above, visit our report page or contact PW Consulting’s industry team.

For detailed analysis of this topic, please visit the official page:Nursery Planters and Pots Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com