Bakery Products Market Growth Through Export Opportunities

Food |

2026-02-20 07:11:42

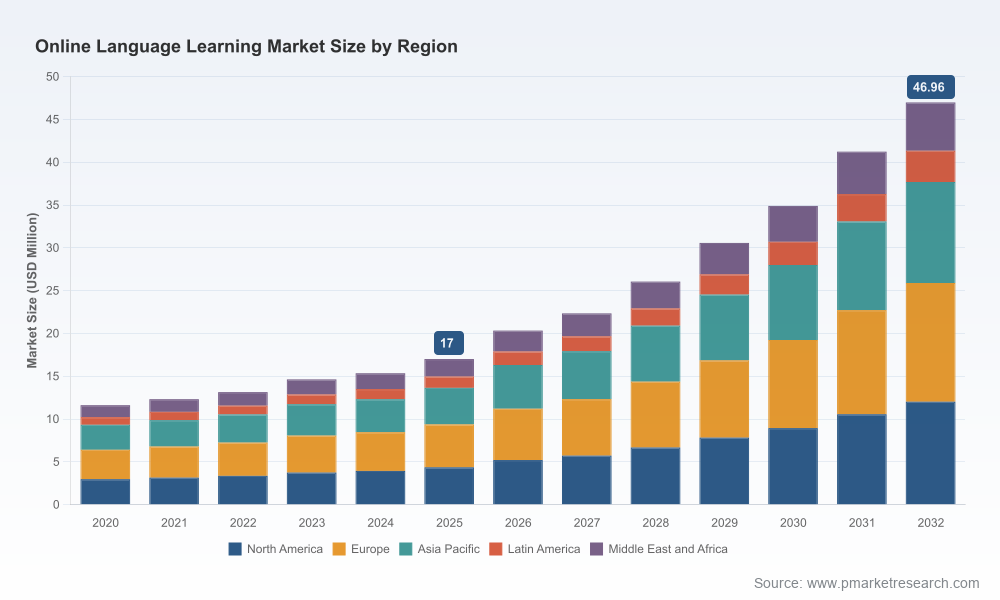

As digital learning matures from niche app experiences to embedded enterprise capability, the Online Language Learning market is entering a new growth inflection that will reshape product roadmaps, go‑to‑market models, and M&A agendas in 2026. Our PW Consulting analysis shows the market expanding at a compound annual growth rate (CAGR) of 15.83%, rising from an estimated USD 11.62 million in 2020 to USD 17.0 million in 2025, with projections pushing beyond USD 20 million in 2026 and approaching USD 47 million by 2032. This trajectory reflects sustained demand across consumer, corporate and cross-border mobility use cases — and it creates concrete opportunities and risks for vendors, buyers and investors this year.

Online Language Learning Market

Timing and allocation: The market growth rate implies that discretionary investment made in 2026 will either capture disproportionate share through early scaling or risk premium erosion as incumbents consolidate.

Online Language Learning Market

Portfolio prioritization: Executives must decide which capabilities—AI tutoring, live tutoring marketplaces, blended enterprise offerings, or content libraries—move from experimental to core investment in 2026.

Online Language Learning Market

Regulatory and cost headwinds: New data‑sovereignty rules and rising infrastructure electricity demand mean product design, vendor selection, and location strategy are now strategic choices with measurable cost and compliance implications.

The sector is no longer simply about user acquisition funnels and gamified retention. Our modelling of the 2020–2025 historical series and the 2026–2032 forecast period shows compounding forces that will determine winners: modular AI tutoring engines, scalable marketplace models for human tutors, and enterprise-grade compliance. The market concentration metrics indicate moderate top‑player dominance — the top three firms account for a significant share while the top five widen that footprint further — a structure that creates both partnership and competitive pressures for mid‑tier vendors and new entrants.

Practical implication: companies that can scale proprietary AI and secure reliable feedstock of human tutors while meeting enterprise controls will see unit economics improve sharply as the market expands.

Product leaders (consumer‑grade AI and gamification): Firms that combine bite‑sized mobile learning with AI enhancements continue to set expectations for engagement and freemium funnels. Recent product moves—such as enterprises making high‑value AI features broadly accessible—signal a shift in monetization strategy from strict premium gating to engagement‑driven lifetime value optimization.

Structured subscription providers: Companies with curated lesson pipelines and corporate training variants are doubling down on conversion pathways from consumer to enterprise accounts; promotional activity around lifetime or heavily discounted enterprise bundles illustrates willingness to compete on price to lock in long‑term revenue.

Marketplace platforms: Tutor marketplaces leverage network effects and long tail language demand by matching supply and demand globally. Their strategic questions in 2026 are platform monetization, quality assurance and AI augmentation to increase per‑learner spend without reducing tutor supply incentives.

Illustrative signals observed in early 2026 include a major platform broadening access to previously premium AI explanation tools, and another incumbent deploying aggressive lifetime offer promotions to stimulate adoption — both tactics reveal a market testing the elasticity of pricing and the interplay between feature access and user retention.

Two non‑product trends will materially alter strategic planning cycles in 2026:

Data sovereignty and privacy: The EU Data Privacy Framework requires localized, compliant processing for certain learning interactions — effectively pushing many platforms toward edge computing and regional data residency solutions. For companies targeting multinational enterprise clients, this is now a procurement and architectural requirement, not a compliance afterthought.

Energy and infrastructure cost pressure: Data center electricity demand in Europe is expected to surge through the next decade, creating higher operating costs and political pressure for greener compute. In some hubs, digital services have already become a non‑trivial fraction of municipal electricity consumption, which tightens timelines for negotiating sustainable cloud contracts and for engaging standards bodies around AI energy efficiency.

Strategic implication: product roadmaps must incorporate footprints and energy profiles of compute (inference vs. training), while commercial teams need to translate those operational choices into pricing and SLAs for enterprise customers.

Our report is designed as a playbook for boardrooms and product teams alike. It synthesizes market kinetics with executable deliverables aimed at reducing time to decision:

Market sizing and runway modelling: calibrated top‑line scenarios and breakpoints to test investment rounds, GTM timing and international expansion sequencing.

Product and tech playbooks: prioritized capability maps (AI tutoring stacks, live tutoring integration, speech recognition and prosody), architectural trade‑offs, and vendor selection criteria for edge vs. cloud deployments.

Commercial go‑to‑market templates: tailored pricing experiments, enterprise packaging, channel partner frameworks, and retention levers validated by demand signals.

M&A and partnership scorecards: target profiles, integration risks, valuation sensitivities and a short list of archetypal targets matched to strategic outcomes.

Regulatory & sustainability checklists: operational steps to achieve data residency, privacy compliance, and energy‑efficiency reporting required by major regional frameworks.

Operational stress tests: scenario analysis for energy price shocks, data‑localization costs, and competitive price promotions so executives can stress capital allocation and customer lifetime value assumptions.

Move from experimental to defensible: Allocate a measured share of innovation budget toward scalable AI tutoring modules that can be licensed or white‑labeled to other platforms. This preserves optionality while enabling incremental revenue capture as adoption grows at the forecasted CAGR.

Build a compliance‑first enterprise offering: For firms pursuing corporate accounts, embed data‑residency and privacy compliance into product architecture rather than retrofitting. Early investment here reduces bid friction with multinational buyers.

Hedge infrastructure risk: Negotiate multi‑region cloud contracts with energy‑performance SLAs and diversify between hyperscalers and regional data centers. Where feasible, pursue near‑term partnerships that provide preferential access to greener compute capacity.

Price dynamically and test rigorously: Competitive activity in early 2026 shows players are experimenting with feature gating and promotional pricing to accelerate scale. Run controlled experiments to understand the trade‑off between acquisition velocity and long‑run unit economics.

Consider marketplace hybridization: For companies relying on human tutors, use AI to augment tutor productivity and to create higher‑value product tiers rather than simply competing on cost per session.

Productization of AI features — the pace at which premium AI capabilities are democratized or re‑gated affects monetization strategies across the market.

Regulatory clarifications — implementation guidance on data residency and environmental rules will shape where platforms choose to host critical services.

Energy pricing and capacity announcements in major data center hubs — spikes or capacity constraints will materially affect operating margins for AI‑heavy vendors.

Competitive pricing moves — aggressive lifetime or discount promotions may signal market consolidation tactics or customer acquisition cost re‑optimization.

This article outlines the strategic contours and high‑impact levers that will matter for 2026. To preserve the commercial value of the underlying intelligence and to respect client research confidentiality, detailed regional splits, granular application penetration, and the full numerical breakdown of segmentation are available exclusively in the full PW Consulting report. Those datasets enable precise market entry models, granular competitor benchmarking, and valuation work for investment committees.

If your 2026 strategy hinges on where to invest, partner, or acquire in the Online Language Learning market, our full report delivers the complete dataset, company scorecards, and executable playbooks you need to operationalize the recommendations above. Contact PW Consulting for an executive briefing and access to the full report to convert these strategic signals into decisive action.

For detailed analysis of this topic, please visit the official page:Online Language Learning Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com