Kids' Smartwatch Market — Strategic Preview for 2026 Decision-Makers

As PW Consulting’s lead industry analyst, I present a focused, strategy-oriented preview of our new Kids' Smartwatch Market study. This piece synthesizes the headline macro drivers, competitive dynamics, and near-term strategic imperatives that will shape executive decisions in 2026. It is intentionally concise and directional—designed to demonstrate the depth of our analysis while preserving the detailed segmentation and proprietary metrics that can only be accessed in the full report.

Kids' Smartwatch Market

Market at a Glance: trajectory and scale

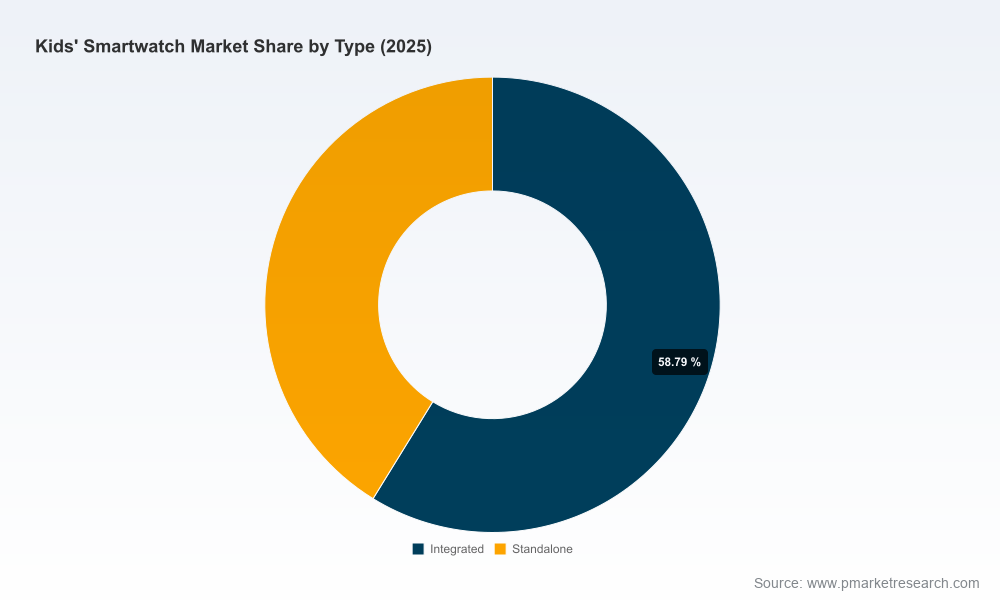

By our accounting, the global kids' smartwatch market has moved from a modest early-decade base into a stable growth phase. The market expanded from the low hundreds of millions in 2020 to a base-year (2025) market size of approximately USD 215 million (Million, USD base). Looking ahead, we forecast a steady compound annual growth rate of roughly 8.5% through our 2026–2032 horizon, taking the market toward the mid-three-hundreds by 2032.

Kids' Smartwatch Market

That growth profile reflects a market that is neither hyper-volatile nor saturated: enough room for new entrants and value migration, but also sufficient concentration among established players to warrant carefully targeted competitive strategies. Notably, the market exhibits a high degree of top-end concentration (our CR3 and CR5 metrics show that leading firms control a substantial majority of revenue), which has direct implications for distribution, pricing, and partnerships.

Kids' Smartwatch Market

Why 2026 matters: inflection points executive teams must watch

- Technology consolidation — The transition from single-band location services to dual-band GPS, more resilient cellular connections (including mainstream 4G support), and on-device low-power AI capabilities will separate premium offerings from commodity devices in 2026.

- Regulatory and privacy pressure — Increasing scrutiny around children’s data and communications will push device vendors to embed compliance and "privacy-by-design" as core product features rather than afterthoughts.

- Channel evolution — Direct-to-consumer, telco partnerships, and education/institutional channels will each demand different commercial models; product configuration and pricing must be tailored accordingly.

- Feature fragmentation — Safety-first devices (limited internet, approved contacts), education-first platforms (learning apps, gamified content), and entertainment-heavy wearables (cameras, media players) are diverging into clearer value propositions.

What’s driving growth (data-driven themes)

- Parental demand for safety and simplicity: A persistent desire for reliable location, curated communication, and easy-to-use interfaces continues to underpin purchases. Devices that reduce parental anxiety without exposing children to open internet access command premium positioning.

- Product feature maturation: Advances such as low-power AI, improved GPS accuracy, and richer on-device content expand use cases beyond rudimentary tracking, making watches more defensible as long-term household purchases.

- Affordability and lifecycle economics: While premium models push feature boundaries, mid-tier devices that balance price and capability sustain broader adoption—especially through carrier bundles and education programs.

- Concentration effects: High market concentration among a few vendors creates stable platforms and accessory ecosystems, but it also signals opportunity for niche entrants that can exploit unmet needs (e.g., ultra-secure, school-compliant devices).

Competitive landscape — who matters and why

Our competitive analysis covers established consumer electronics brands, specialist kids' tech vendors, telco-affiliated devices, and emerging OEMs. Each archetype competes on a mix of hardware design, software experience, channel reach, and trust signaling to parents.

- VTech (HK): Known for its educational play-to-learn pedigree, VTech’s KidiZoom Smartwatch lineup combines cameras and age-targeted educational content. Its brand credibility among parents of younger children gives it a durable position in the education/entertainment crossover.

- Gabb Wireless (Utah): Gabb’s platform-led approach emphasizes no-internet safety, curated contacts, and parental controls. Recent software refreshes reinforce usability and performance—key to defending parents who prize minimal exposure over bells-and-whistles.

- Starmax Technology (Shenzhen): Starmax competes on hardware variety, light-weight safety materials, and sport/activity tracking. Its manufacturing flexibility helps push feature sets at aggressive price points.

- Contixo (Chino, CA): Contixo’s offerings bridge educational content and rich media (HD screens, cameras), appealing to households seeking multifunction devices for ages spanning toddlers to preteens.

- TCL Mobile (HK): TCL has moved to a premium safety-and-connectivity play with devices that combine dual-band GPS, 4G calling, and AI-powered school modes—features that make it attractive to parents wanting advanced tracking and remote engagement tools.

- Verizon (New York): As a carrier-backed device option, Verizon’s offering integrates directly with telco services and parental billing, making it an important channel partner and a distinct route-to-market for device makers.

Recent vendor moves underscore these trends. For example, a late-2025 product launch from a major consumer electronics brand introduced dual-band positioning and AI-driven parental features—an explicit bet on accuracy and safety as differentiators. And a leading safety-first vendor issued a major OS refresh in early 2026 that streamlines the user experience and reduces friction for families upgrading from legacy devices.

Product and technology priorities for 2026

- Location fidelity: Dual-band GNSS and hybrid positioning (cell+WiFi fallback) will be minimum viable features for premium SKUs.

- Battery and power management: Improved endurance through hardware-software co-optimization will enable always-on safety features without daily charging trade-offs.

- Edge AI and privacy: Localized processing for activity recognition and school-mode enforcement reduces cloud dependency and regulatory exposure.

- Modular software stacks: A configurable OS that supports “safety-only,” “learning,” or “entertainment” profiles will broaden addressable markets without proliferating hardware SKUs.

Commercial implications: channels, pricing, and partnerships

Executives looking to expand in 2026 should weigh three parallel GTM plays:

- Carrier-first strategy: Leverage telco relationships for distribution and recurring service revenue. Ideal for devices with robust cellular features and parental billing integration.

- Retail + DTC hybrid: Combine the reach of big-box retailers for mass SKUs with direct channels for upsell services (extended warranties, premium content subscriptions).

- Institutional and education partnerships: Pursue contracts with schools and child-care organizations for bulk deployments and integrated management platforms—particularly for products emphasizing student safety and compliance.

Pricing will need to be elastic across these channels. Operators and retailers value low upfront cost with service attachment; parents increasingly accept subscription models for premium safety and content features. Strategic bundling—hardware plus layered subscription tiers—will be the dominant monetization model for mid-to-high tier devices.

M&A and alliance playbook

Given the market concentration and the technological pockets that matter (AI for safety, GNSS accuracy, secure comms stacks), acquisitive strategies in 2026 should prioritize:

- Small-to-mid acquisition targets with differentiated safety software or content IP

- Partnerships with carriers to fast-track scale and achieve better unit economics

- Licensing deals with education content providers to build stickier ecosystems

Non-dilutive collaborations—co-branded devices with trusted kid-focused consumer brands or telcos—offer lower-risk pathways to rapid distribution without the heavy CAPEX of organic expansion.

What the full PW Consulting report delivers (practical, actionable content)

- Market sizing and validated growth forecasts (2020–2025 historical base; 2026–2032 forecast), with scenario modeling that isolates downside regulatory impact and upside adoption shifts.

- Go-to-market playbooks tailored to each channel archetype, including suggested pricing ladders and subscription packaging strategies.

- Product roadmap templates prioritized by ROI—mapping hardware features to monetizable service tiers and expected payback periods.

- Competitive benchmarking of leading vendors across product, software, distribution, and brand trust metrics, with tactical recommendations for positioning and white-space targeting.

- M&A screening criteria and a short list of target profiles (technology, channel, and content assets) for bolt-on growth.

- Regulatory and privacy impact assessment, including compliance checklists and data governance templates to expedite market entry.

To preserve the integrity of our proprietary work, the report intentionally withholds the granular segmentation tables and some scenario-level revenue detail from this public preview. Those core breakdowns—critical for model-driven investment and competitive response—are available in the full report package.

Recommended 90-day action plan for 2026

- Product gap audit: Map current SKUs against the priority feature set (dual-band GNSS, on-device AI, battery endurance) and define a minimal viable upgrade path for each channel.

- Channel pilot: Launch a carrier pilot with a bundled safety-subscription tier to validate ARPU, churn, and take-rate assumptions in a controlled cohort.

- Compliance sprint: Harden data governance, build an auditable privacy-by-design checklist, and secure any third-party certifications parents value.

- Competitive maneuver: Initiate two strategic discussions—one with a content partner for education bundles, and one with a telco for distribution—to test co-marketing economics.

Conclusion: positioning for durable growth

The kids' smartwatch market in 2026 is a disciplined growth market: attractive for companies that can combine hardware reliability, software simplicity, and credible privacy safeguards. With a clear growth trajectory and concentrated incumbency, the prize is significant for firms that can align product development, channel strategy, and regulatory readiness within a coherent commercial model.

PW Consulting’s full study supplies the granular forecasting, segment economics, and tactical playbooks necessary to move from strategy to execution. For teams preparing 2026 budgets and strategic initiatives, the report is built to shorten the time from decision to deployment while reducing execution risk. Contact our research desk to review the full dataset, actionable forecasts, and custom advisory options.

For detailed analysis of this topic, please visit the official page:Kids' Smartwatch Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com